Physical underwriting

Roof Weather Risk and Physical Underwriting: How to Use Hail, Wind, Heat, and Rain Without Overclaiming the Evidence

Weather data is most useful when it is tied to roof vulnerability and evidence quality. This guide gives insurers, brokers, owners, and roofers a practical framework for using exposure records without pretending they prove roof damage.

Key takeaways

- Weather records are exposure signals, not automatic proof of property-specific roof damage.

- Underwriting decisions need a link between hazard intensity, roof vulnerability, observed condition, and consequence.

- A roof with thin records should receive a lower confidence score even when the hazard signal is strong.

- The best commercial workflow turns weather history into inspection priority, documentation requests, and intervention timing.

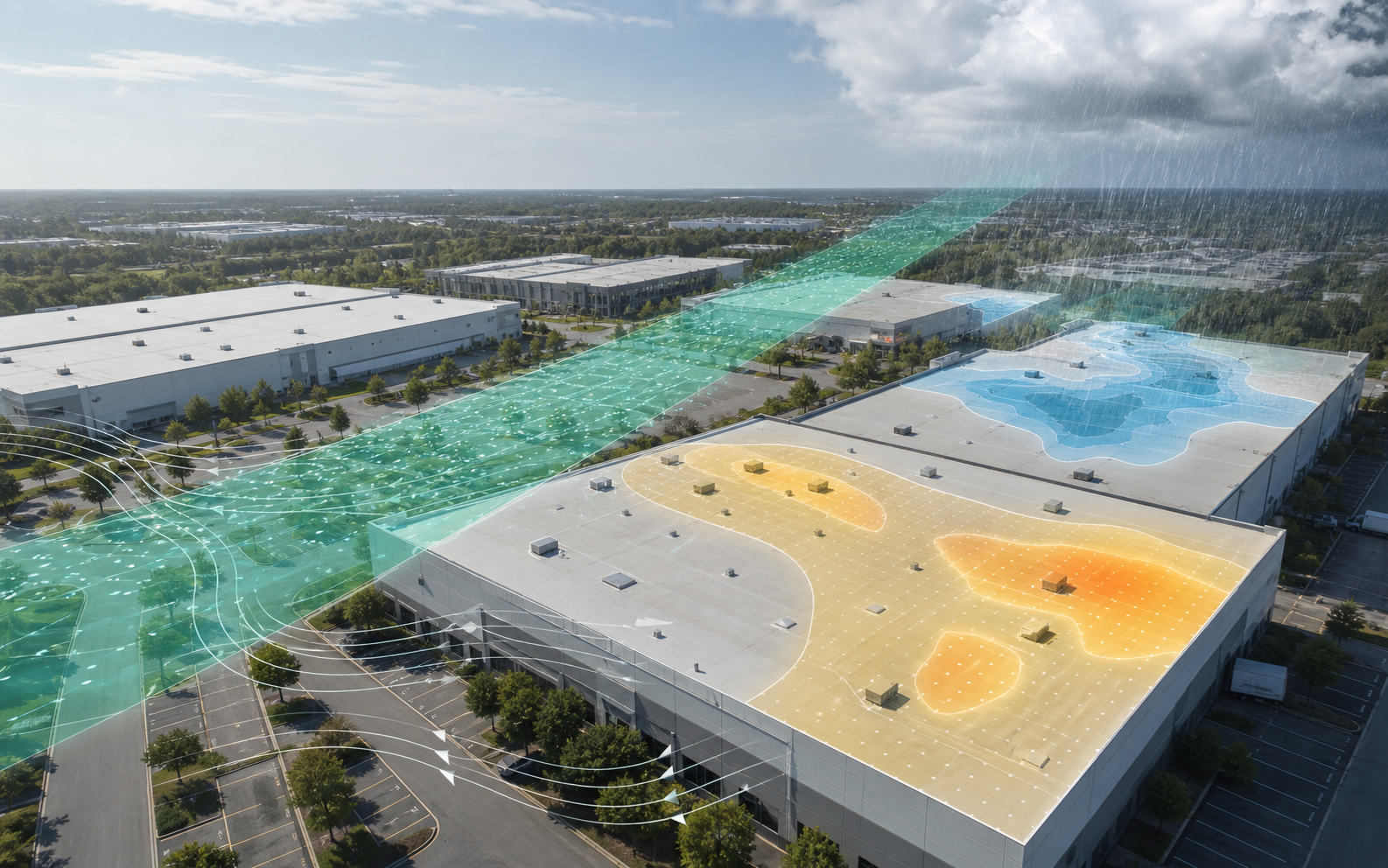

Weather data becomes useful when it is attached to vulnerability

Commercial roof weather risk is easy to misunderstand. A hail report near a building sounds concrete. A wind gust threshold sounds technical. A heat map looks objective. A rainfall total feels decisive. None of those signals, by itself, answers the physical underwriting question. The question is not only what happened in the sky. The question is whether the roof system below it was vulnerable, whether property-specific evidence changed, and whether the consequence of failure justifies action.

This distinction is where many roof conversations become noisy. Roofers may see weather as a reason to start outreach. Owners may see it as a maintenance trigger. Brokers may see it as a diligence concern. Insurers may see it as an exposure indicator. Lenders may see it as a reserve or repair question. Everyone is partly right, but the signal becomes dangerous when weather history is treated as roof damage proof.

Asset Optimix uses a four-part frame:

- Hazard: the weather or climate stressor that may affect the roof.

- Vulnerability: the roof characteristics that make the hazard matter.

- Evidence: the records, photos, inspection notes, work orders, and observations that support or weaken concern.

- Consequence: the business, financial, tenant, safety, or lending effect if the roof fails.

Weather data sits in the first category. It becomes underwriting value only when it is connected to the other three.

What official storm records can and cannot do

The NOAA/NCEI Storm Events Database contains records used for the official NOAA Storm Data publication. It documents significant weather phenomena, including events with enough intensity to cause loss of life, injuries, significant property damage, disruption to commerce, rare or unusual weather, and other significant meteorological events. The page also notes that the database includes records from January 1950 to February 2026 as entered by NOAA's National Weather Service, with important differences in available periods of record by event type.

That is valuable context for commercial roofs. It can establish that severe weather was reported in a region, help build a weather timeline, and identify which buildings deserve attention after an event. It also has limits. A storm-event record is not a parcel inspection. It is not a roof core. It is not a membrane test. It does not know whether an HVAC technician opened a curb flashing two months later. It does not know whether the roof was already wet before the event.

The National Weather Service definition of severe thunderstorm is also useful. NWS public guidance defines a severe thunderstorm as a thunderstorm producing a tornado, wind of at least 58 mph, and/or hail at least one inch in diameter. That threshold tells us why hail and wind should not be treated casually. It does not tell us whether a specific low-slope roof was damaged.

A responsible roof-weather interpretation should therefore use language like:

- "Severe weather was reported near the property during the review period."

- "This exposure increases inspection priority because the roof has edge, age, drainage, or membrane vulnerability."

- "No parcel-level damage conclusion is made without property-specific evidence."

- "The next action is inspection, documentation, or record request, not an automatic claim or replacement conclusion."

This is not timid. It is how the analysis stays useful across roofing, underwriting, and real estate use cases.

Hazard, vulnerability, evidence, consequence

Physical underwriting is not a weather lookup. It is a decision process that asks how a building may perform under stress and what it would cost if performance fails. For roofs, the best simple model is:

| Category | Roof-weather meaning | Example question |

|---|---|---|

| Hazard | Weather or climate stress | Was there reported hail, severe wind, extreme heat, heavy rain, snow, freeze-thaw, or debris exposure? |

| Vulnerability | Roof system susceptibility | Is the roof older, low-slope, poorly drained, heavily penetrated, edge-exposed, poorly documented, or frequently trafficked? |

| Evidence | Property-specific support | Are there dated photos, inspection notes, leak tickets, repair invoices, moisture scans, or roof consultant observations? |

| Consequence | Business impact | Would a leak interrupt tenants, inventory, public services, insurance placement, loan closing, or property sale? |

The highest-risk cases are not simply the strongest weather events. A severe event over a newer, well-documented, inspected roof with low consequence may call for routine documentation. A moderate event over an older, poorly drained roof above critical tenant operations may call for immediate inspection. Underwriting needs the combination.

This is why Asset Optimix should avoid a single "storm score" as the public language. A single score can be useful internally, but the user needs to know which part of the chain is driving the recommendation. Is the roof high priority because the hazard was strong? Because the roof is vulnerable? Because the records are weak? Because the consequence is high? Those are different conversations.

Hail exposure needs roof context

Hail is highly visible in marketing, but hail underwriting is often too blunt. The size, density, speed, storm direction, duration, roof slope, membrane type, surface temperature, cover board, insulation, age, prior moisture, and attachment all affect outcome. A large hail report near a building should matter. It should not be presented as a damage conclusion without roof-specific evidence.

Commercial roofs also differ from steep-slope residential roofs in ways that change the inspection question. Low-slope membranes may show punctures, fractures, bruising, displaced ballast, damaged coatings, or impact effects around equipment and exposed areas. Metal roofs can have different denting and coating concerns. Aggregate-surfaced roofs, smooth membranes, coated systems, recover assemblies, skylights, rooftop equipment, and parapets all create different evidence patterns. A hail event may damage rooftop equipment or accessories even when the membrane field does not show obvious distress from a distance.

The first pass should ask:

- What hail sizes were reported near the property?

- How close and how reliable are the reports?

- Was there a post-event inspection?

- What roof material and age band are known?

- Are there skylights, rooftop units, solar panels, soft metals, or exposed accessories?

- Did leak tickets, tenant complaints, or repair invoices increase after the event?

- Are photo sets available from before and after the event?

The strongest evidence is temporal and physical. A weather event followed by dated inspection photos, mapped impact areas, and professional notes is stronger than a weather event alone. A pre-event condition report is especially valuable because it lets the reviewer distinguish old distress from new distress.

For commercial roofers, the ethical sales workflow is inspection priority. "A hail event was reported nearby, and this roof has conditions that make inspection reasonable" is a defensible statement. "Your roof was damaged" is not defensible without inspection evidence.

Wind exposure is often the more structural conversation

Wind can be less obvious than hail and more consequential. Wind affects perimeter edges, corners, roof-mounted equipment, membrane attachment, doors, openings, parapets, loose materials, and over-pressurization. The Insurance Institute for Business & Home Safety has described commercial-building wind research focused on roof membrane and perimeter edge flashing, load path, rooftop equipment, large openings, and over-pressurization. That is a useful underwriting frame because it recognizes that the roof is part of a larger building system.

For commercial roofs, wind review should not be limited to "did the roof blow off?" Many meaningful wind issues are partial:

- Edge metal loosening.

- Membrane billowing or displaced ballast.

- Open laps or lifted corners.

- Damage around rooftop equipment.

- Loose panels, curbs, or accessories.

- Scattered debris impacts.

- Water entry after wind-driven rain.

- Interior symptoms after an event with no obvious field failure.

Wind history becomes more important when the building has large open exposure, older roof attachment, edge concerns, prior patching near perimeter zones, rooftop equipment, or weak documentation. It also becomes important when a building's operations cannot tolerate even short interruption. A warehouse storing noncritical goods may have different consequence than a medical, food, cold-storage, data, municipal, or high-value inventory facility.

Wind underwriting should include a perimeter evidence request. A roof inspection that only photographs the field can miss the highest-consequence details. The file should include corners, edge metal, parapets, coping, terminations, drains near perimeter areas, rooftop equipment anchorage, large openings, and any signs of prior edge repair.

The conclusion should stay in the correct lane: wind exposure plus vulnerability justifies review. It does not replace field assessment, engineering judgment, or insurance coverage analysis.

Heat and ultraviolet exposure change the background rate of aging

Heat is not as dramatic as hail, but it can be more persistent. Roof surfaces experience solar radiation, temperature cycling, thermal movement, material aging, sealant aging, and changes in reflectivity. The U.S. Department of Energy cool-roof guidance and EPA heat-island cool-roof guidance discuss how reflective roof surfaces can reduce heat transfer and broader heat-island effects. For roof prediction, the practical point is that heat changes both building energy context and roof material exposure.

Heat risk should not be reduced to "hot climate equals bad roof." The roof assembly, reflectivity, maintenance, dirt accumulation, slope, drainage, insulation, membrane color, rooftop equipment, and local microclimate all matter. Soiling can reduce reflectivity. Ponding can concentrate degradation. Rooftop equipment can create hot discharge zones. Dark surfaces can run hotter. Light surfaces can still fail at seams, edges, or penetrations.

Heat is best used as a background modifier:

- Older membrane plus high heat exposure means inspection priority increases.

- Repeated heat cycling near transitions can make flashings and sealants more important.

- Soiled or discolored reflective surfaces may reduce expected performance.

- Cooling-sensitive buildings may have both roof-condition and energy-cost exposure.

- Roof replacement decisions should consider energy, moisture, and durability, not only first cost.

For underwriters, heat is usually not a single event trigger. It is part of vulnerability and useful-life confidence. For roofers, it is a maintenance education topic. For owners and lenders, it is a reserve-timing input.

Rainfall, drainage, and water duration

Rain is common, but water duration is the roof-risk variable. A roof that drains quickly after heavy rain behaves differently from a roof that holds water at drains, seams, parapets, equipment curbs, or depressed insulation. WBDG roofing guidance calls attention to well-functioning drains, valleys, gutters, and downspouts, and notes that failed components can create ponding and additional load stress. EPA moisture-control guidance similarly treats roof water collection and disposal as a design and maintenance concern.

Rainfall history should be used with drainage evidence:

- Was rainfall unusually heavy or repeated across days?

- Did leak tickets increase after rain events?

- Are stains located below drains, parapets, equipment, or field areas?

- Do inspection photos show sediment rings or recurring ponding?

- Are drains cleaned and documented?

- Did rooftop equipment condensate add water outside storm events?

- Has insulation or deck deflection changed roof slope over time?

Rain is often the event that reveals a roof problem rather than the root cause. A leak after rain may be caused by a clogged drain, an open flashing, a deteriorated seam, a failed repair, condensation, plumbing, facade issues, or a roof defect. The underwriting workflow should avoid assuming that every interior water symptom is membrane failure.

Location mapping is the practical tool. If a rain-related leak appears under a specific drain line, the roof membrane may not be the only suspect. If it appears under a curb after wind-driven rain, flashing may be the priority. If it appears after prolonged ponding, drainage and assembly saturation may need review. Weather history helps order the questions.

Snow, freeze-thaw, and cold-region roof files

Cold-region commercial roof risk can be under-modeled if the system only tracks hail and wind. Snow load, ice, freeze-thaw cycling, drainage blockage, thermal bridging, interior humidity, vapor movement, and rooftop equipment all matter. A roof that performs acceptably in warm rain can have different problems when drains freeze, snow blocks scuppers, or interior moisture condenses in the assembly.

WBDG moisture-management material is useful here because it treats moisture as multiple mechanisms, not just rain leakage. Vapor and air movement can matter in roof assemblies. Condensation risk is not always visible from the exterior. A building with high interior humidity, process loads, food operations, pools, manufacturing, or unusual HVAC conditions may need more careful roof-envelope review than a generic low-slope roof.

For prediction, cold-region inputs can include:

- Snow and freeze-thaw climate exposure.

- Roof drainage layout and overflow provisions.

- Interior humidity or process use.

- Evidence of ice around drains or scuppers.

- Past winter leak patterns.

- Insulation and vapor-control documentation.

- Roof access and snow-removal practices.

- Structural and load-sensitive building use.

The best output may not be "high roof failure risk." It may be "low confidence without assembly records" or "winter inspection trigger needed." Underwriting value often comes from naming the missing evidence.

The evidence ladder for roof-weather underwriting

Weather exposure should be graded alongside evidence quality. A strong weather signal with weak property evidence is not the same as a strong weather signal with detailed inspection evidence. The following ladder helps keep claims proportional.

| Evidence tier | Example | Underwriting use |

|---|---|---|

| Tier 1: Regional exposure | NOAA/NCEI storm event, NWS warning, radar-derived context, climate history | Prioritize buildings or markets for review |

| Tier 2: Property vulnerability | Roof age band, material, drainage, equipment density, edge exposure, prior repairs | Decide which exposed buildings need inspection first |

| Tier 3: Property symptoms | Leak tickets, tenant complaints, stains, repair calls after event | Connect exposure to possible condition change |

| Tier 4: Field observations | Dated inspection photos, roof consultant notes, mapped defects | Support repair planning, underwriting questions, or reserve changes |

| Tier 5: Diagnostic evidence | Moisture survey, core cuts, engineering review, manufacturer or consultant assessment | Support high-consequence decisions and professional conclusions |

Many early commercial conversations live in tiers 1 through 3. Many binding business decisions require tier 4 or 5. The system should tell users which tier they have and which tier they need.

This ladder also prevents a common mistake: treating lack of evidence as evidence of lack. If a property had severe weather exposure but no post-event inspection, the correct conclusion is not "no damage." It is "unverified." If a property has no reported storm record but repeated leaks after rain, the correct conclusion is not "weather irrelevant." It is "condition evidence deserves review even without a severe-weather record."

How to turn weather history into an inspection trigger

A practical trigger should be clear enough for operations teams and careful enough for underwriters. The trigger should not be "any storm equals inspection." That creates noise. It should combine exposure and vulnerability.

Example trigger logic:

| Trigger | Why it matters | Next action |

|---|---|---|

| Hail one inch or larger reported near roof with older age band or exposed accessories | NWS severe hail threshold plus vulnerable roof context | Request roof and accessory inspection photos |

| Wind 58 mph or higher reported near roof with edge or rooftop-equipment concerns | Severe wind threshold plus perimeter/equipment vulnerability | Inspect edges, corners, equipment, and openings |

| Heavy rain after known ponding or drain problems | Rainfall stress plus drainage vulnerability | Check drains, ponding zones, interior symptoms, and repair history |

| Heat season after older dark or soiled membrane | Background aging modifier | Schedule maintenance review and reflectivity/condition notes |

| Winter leaks near drains or parapets | Freeze, snow, and drainage interaction | Review drainage, insulation, vapor, and interior humidity context |

For a commercial roofer, these triggers can guide outreach and service scheduling. For an owner, they can guide maintenance budgets. For an insurer, they can guide risk-control questions. For a broker, they can guide what to collect before renewal or transaction due diligence.

The trigger should always produce a next action, not just a risk label. A label that says "high weather risk" is less useful than "inspect perimeter edge and rooftop equipment after the April wind event; roof age records are missing; tenant consequence is high."

Physical underwriting needs confidence scoring

Confidence scoring is not the same as risk scoring. A roof can be high risk with high confidence if defects are well documented. A roof can be moderate risk with low confidence if records are missing. A roof can be low apparent risk but low confidence if access was blocked and no photos exist. For underwriting, confidence is crucial because it tells the user how much weight to put on the conclusion.

Confidence inputs include:

- Recency of inspection.

- Roof access quality.

- Photo coverage.

- Roof plan availability.

- Age and warranty records.

- Repair invoice clarity.

- Leak log mapping.

- Weather event chronology.

- Consistency between records and visible evidence.

- Professional review level.

Fannie Mae's multifamily PCA underwriting guidance is useful outside its direct lending context because it emphasizes actual property condition, deferred maintenance, components past useful life, alignment among inspection, PCA report, loan documents, photos, captions, component ratings, and reserves based on property needs and remaining useful life. The broader lesson is that physical evidence, documents, photos, and reserve decisions should align.

Asset Optimix should make confidence visible. A model output that says "medium roof intervention priority, low evidence confidence" is more honest than one that hides the data gap. For a sales workflow, low confidence can become a reason to inspect. For underwriting, low confidence can become a condition, exclusion question, or follow-up request. For a buyer, low confidence can become a diligence item.

What brokers and buyers should ask before weather becomes a price fight

Weather history often enters a transaction late. A buyer sees storm reports, asks whether the roof was inspected, and the seller responds with a general statement. That is when uncertainty turns into leverage. The better workflow is to collect roof-weather evidence before the buyer has to ask.

Pre-market roof-weather file:

- Roof age evidence by section.

- Most recent roof inspection report.

- Photos of each roof zone, drain, edge, parapet, and major equipment area.

- Repair invoices from the last five years.

- Leak ticket summary mapped to locations.

- Major hail, wind, and rainfall events during the ownership period.

- Notes showing whether post-event inspections occurred.

- Current warranty and transfer information if applicable.

- Known open issues and planned maintenance.

This file does not need to claim the roof is perfect. It needs to show that the owner knows what is known. A buyer can price known risk. Unknown risk tends to become a discount.

For 1031 exchange buyers, timing makes this even more important. Compressed diligence windows reward organized evidence. If the roof file is weak, the buyer may have to either accept uncertainty, push for reserves, demand concessions, or walk. A roof-weather intelligence layer can identify those risks earlier.

How insurers and insurtech teams can use roof-weather intelligence

For insurance and insurtech readers, the temptation is to turn roof-weather history into a direct rating variable. It may be part of risk selection or pricing, but the more defensible use is a structured physical-underwriting feature set.

Potential features:

- Roof age confidence band.

- Roof material or assembly indicator.

- Low-slope versus steep-slope class.

- Drainage and ponding indicators.

- Equipment and penetration density.

- Prior repair and leak chronology.

- Hail exposure frequency and recency.

- Severe wind exposure frequency and recency.

- Heat and rainfall climate modifiers.

- Post-event inspection evidence.

- Property consequence class.

- Evidence confidence score.

The model should avoid unsupported causation. A property with repeated hail exposure and poor roof records may deserve closer underwriting review. That does not mean hail damaged the roof. A property with no recorded severe hail but extensive recurring leak tickets may deserve review. That does not mean weather is the cause. The output should support triage, not pretend to be a claim determination.

This framing is especially important for automated systems. Automated roof intelligence will be trusted only if it shows evidence quality, confidence, and the difference between exposure and observed condition. Black-box certainty is not a virtue in physical underwriting.

How commercial roofers can use weather without damaging trust

Weather-triggered roofing outreach can be useful or abusive. The difference is evidence and wording. Commercial roofers have a legitimate reason to contact owners after severe weather, especially where roof vulnerability is visible or known. They lose trust when they imply a database record proves damage or an insurance outcome.

Better outreach:

- "A severe hail or wind event was reported near this area."

- "Your building appears to have a low-slope roof with multiple rooftop units."

- "If there has not been a post-event inspection, it would be reasonable to document the roof before the next storm season."

- "We can separate maintenance issues, event concerns, and records gaps."

Poor outreach:

- "Your roof is damaged."

- "Insurance will pay."

- "Every building in this area needs replacement."

- "The storm report proves your claim."

The first set educates. The second set creates legal, insurance, and reputation risk. Asset Optimix should support the first set.

For channel partnerships, this matters commercially. A roofer using Asset Optimix should be able to show prospects why an inspection is reasonable without overstating the model. That creates a higher-quality lead and a better long-term brand.

Intervention timing: inspect, monitor, repair, reserve, replace

Weather-risk intelligence should end in an action category. The most common categories are:

- Inspect: Field review is needed because exposure, vulnerability, symptoms, or consequence justify it.

- Monitor: Risk is present but no immediate action is supported; schedule follow-up and document changes.

- Repair: A specific defect or maintenance item should be addressed.

- Reserve: The roof may not need immediate work, but useful-life uncertainty or exposure justifies capital planning.

- Replace or restore: Professional review supports major intervention, or repeated repair is no longer rational.

The same roof can move between categories as evidence changes. A roof may move from monitor to inspect after a severe wind event. It may move from inspect to repair after a localized flashing defect is found. It may move from repair to reserve after multiple zones show wet insulation. It may move from reserve to monitor after a qualified inspection confirms better condition than expected.

This dynamic view is more useful than a static roof score. Commercial roofs are managed assets. Their risk changes as weather, maintenance, tenants, equipment, and records change.

What not to automate

Some tasks should remain outside a public prediction system unless qualified professionals are involved:

- Code compliance conclusions.

- Structural capacity conclusions.

- Warranty coverage interpretations.

- Insurance coverage or claim payment predictions.

- Hidden moisture conclusions without diagnostic evidence.

- Safety instructions for roof access.

- Engineering opinions.

- Contractor scope approval.

The model can organize evidence for these conversations. It should not pretend to be the professional who owns them. The boundary is good product design because it keeps users from overusing the output.

The executive decision needs a roof-weather thesis

The useful output for an owner, broker, lender, or underwriter is not a raw list of storm events. It is a roof-weather thesis that explains why the next action is proportionate. The thesis should connect the weather record to roof vulnerability, consequence, and evidence confidence.

Examples:

- "Recent severe wind near an older roof with known edge repairs makes a perimeter-focused inspection reasonable before renewal."

- "Hail exposure is present, but no post-event symptoms or inspection findings are available; the correct posture is verification, not a damage conclusion."

- "Repeated rain-related tenant complaints below one roof zone are more actionable than regional storm history because the symptom pattern is mapped and recurring."

- "Heat exposure is a long-term aging modifier, not an emergency trigger, but it should change maintenance priority for older reflective membranes with poor cleaning history."

That kind of thesis helps a commercial roofer explain value without overstating weather. It helps an owner decide whether to spend now or monitor. It helps a lender understand whether the reserve issue is known cost or uncertainty cost. It helps an insurer distinguish a maintained roof from a vulnerable or unknown one.

The thesis should also state what would change the conclusion. A post-event inspection, moisture survey, updated leak log, warranty review, roof consultant memo, or clear repair closeout can materially change the risk posture. Good physical underwriting is not a one-time label. It is a living view of the roof as new evidence arrives.

Regional risk should become building-level prioritization

Insurance teams, commercial roofers, and portfolio owners often begin with regional weather. A storm path crosses a market. A heat wave covers a metro area. A hail corridor appears across a state. A wind event affects multiple counties. Regional risk is useful for awareness, but it becomes operational only when it is translated into building-level prioritization.

That translation should ask:

- Which buildings in the region have the most vulnerable roof assemblies?

- Which roofs have weak age or repair records?

- Which roofs have recent leak or maintenance signals?

- Which roofs have high tenant or operational consequence?

- Which roofs have had no post-event inspection?

- Which buildings are close to renewal, refinancing, acquisition, sale, or lease events?

This is where roof prediction can outperform a weather map. A weather map can show where a storm happened. It cannot decide which roof should be inspected first. Building-level prioritization can combine storm context with physical vulnerability, consequence, and evidence confidence.

For commercial roofers, this creates a better territory strategy. The best opportunities may not be every building under a storm cell. They may be the older low-slope roofs with dense equipment, weak records, and owners facing budget or insurance decisions. For insurers, the same logic can support risk-control outreach. For brokers, it can identify which listings need roof files tightened before diligence. For owners, it can turn a regional event into a practical work order.

Climate exposure should influence maintenance rhythm

Weather is not only discrete events. Climate exposure changes the maintenance rhythm of a roof. Heat, ultraviolet radiation, rainfall patterns, freeze-thaw cycles, wind environment, nearby debris sources, and local storm season all shape how often a roof should be reviewed and what the inspection should emphasize.

A building in a hail-prone region may need stronger post-storm documentation habits. A building in a high-heat region may need closer attention to membrane aging, reflectivity, sealants, and rooftop equipment discharge. A building in a heavy-rain region may need more disciplined drain and scupper maintenance. A building in a cold region may need winter drainage, ice, and interior humidity questions. A coastal or high-wind region may need perimeter, rooftop equipment, and opening protection to receive more attention.

This does not mean every climate signal should trigger expensive work. It means maintenance cadence should match exposure. The owner who cleans drains and documents roof zones before the wet season is not doing paperwork for its own sake. The owner is reducing the chance that a preventable drainage issue becomes a roof assembly problem. The roofer who knows the regional exposure can recommend the right inspection emphasis. The underwriter who sees the maintenance rhythm can better distinguish a watched roof from an ignored roof.

Physical underwriting becomes more accurate when climate is treated as a background pressure on roof vulnerability, not only as a history of dramatic events.

Market timing matters for roof-weather action

The same weather event can mean different things depending on where the building sits in its business cycle. A roof exposed to severe wind two weeks before insurance renewal is not only a maintenance issue. It is a documentation and underwriting issue. A hail event during acquisition diligence is not only a roofing issue. It can affect price, escrow, inspection scope, lender questions, and closing certainty. Heavy rain during a tenant buildout can change operational priority even if the roof was previously considered manageable.

Useful roof-weather intelligence should therefore include timing context:

- Insurance renewal, new placement, or loss-control review.

- Loan maturity, refinance, or acquisition financing.

- Sale process or 1031 exchange deadline.

- Tenant move-in, expansion, or high-value inventory period.

- Capital budgeting cycle.

- Storm season start or post-event response window.

- Warranty expiration or transfer event.

This turns weather from a static record into a decision trigger. If nothing important is happening and no symptoms appear, monitoring may be enough. If a building is entering sale, renewal, or refinancing, the same exposure may justify immediate inspection because uncertainty itself has value.

For commercial roofers, this is one of the best ways to prioritize serious prospects. The strongest outreach is not merely "a storm happened." It is "a storm happened, this roof has vulnerability, and the owner appears to be entering a decision window where roof uncertainty becomes expensive." That is a business reason to talk.

For insurers, brokers, lenders, and owners, timing context also prevents overreaction. A roof with exposure but no symptoms and no near-term business event can be handled differently from a roof with exposure, weak records, and a transaction deadline. The weather may be the same. The decision is not.

That difference is where disciplined underwriting becomes practical.

The strongest files preserve disagreement instead of hiding it

Roof-weather decisions often involve disagreement. A roofer may see a vulnerability that the owner considers routine. A broker may consider a roof issue manageable while a buyer treats it as a major reserve item. An insurer may focus on edge and equipment vulnerability while an asset manager focuses on leak history. A lender may care less about technical nuance and more about whether the capital plan is funded.

A weak file tries to flatten those disagreements into one vague statement. A strong file preserves them and ties each one to evidence. It can say the roof has documented weather exposure, no confirmed event damage, recurring rain-related symptoms in one zone, weak age records, and high tenant consequence. That is not indecision. It is a more accurate view of the building.

This matters because commercial roof action is often collaborative. The owner may authorize inspection. The roofer may define scope. The insurer may request risk-control evidence. The broker may communicate diligence status. The lender may size reserves. Each party can act better when the file shows what is known, what is disputed, and what would resolve the dispute.

The goal is not to remove judgment. It is to make judgment visible enough that the next action is proportionate.

Bottom line

Roof weather risk is not a claim that a storm damaged a building. It is a disciplined way to connect weather exposure to roof vulnerability, property-specific evidence, consequence, and confidence. Used well, it helps roofers prioritize outreach, owners schedule inspection, brokers prepare diligence, lenders think about reserves, and insurers ask better physical-underwriting questions.

The best output is not "hail happened" or "wind happened." The best output is a clear recommendation: this roof deserves inspection, monitoring, repair, reserve planning, or professional review because these evidence categories line up, and these are the limits of the data.

That is the kind of roof-weather intelligence commercial roof decisions need.

Frequently asked questions

Does a NOAA storm event prove that a commercial roof was damaged?

No. NOAA storm-event records can document nearby significant weather, but parcel-level roof damage still requires property-specific evidence.

What makes roof weather underwriting different from weather lookup?

Weather lookup asks what happened nearby. Physical underwriting asks whether the roof assembly was vulnerable, whether condition evidence supports concern, and what the consequence would be if the roof fails.

Where should a roofer use weather history in a sales workflow?

Use it to prioritize education, inspection, and documentation. Avoid presenting exposure records as a guaranteed claim, coverage outcome, or proof of damage.

Sources and limits

Research basis reviewed against NOAA/NCEI, NWS, WBDG, FEMA, EPA, IBHS, and Fannie Mae public guidance. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.