Weather risk

Hail Exposure Versus Roof Damage: What Commercial Property Records Can and Cannot Prove

A hail record can justify attention, but it cannot prove property-specific roof damage by itself. This guide shows how to separate weather exposure, roof vulnerability, inspection evidence, and underwriting confidence.

Key takeaways

- A public hail record is exposure context, not proof that a specific commercial roof was damaged.

- The practical file should separate event records, roof vulnerability, property-specific inspection evidence, consequence, and confidence.

- Post-event roof photos, rooftop equipment observations, leak logs, and repair history matter more than a raw weather map.

- Roofers can build trust by using hail exposure as an inspection and documentation trigger instead of a guaranteed outcome claim.

Hail exposure is not the same as roof damage

Commercial roof hail conversations often start with a weather record. A storm passed near the building. A hail report appeared in a public database. A map shows a swath over the market. A tenant remembers a severe thunderstorm. A broker hears that the area had hail last spring. An owner wonders whether the roof should be inspected. An insurer asks about roof age and prior damage. A lender wants to know whether the property condition file is still current.

Those are legitimate questions. They are also easy to mishandle.

A hail exposure record can show that hail was reported near a location or that conditions supported hail in a region. It cannot, by itself, prove that a specific commercial roof was damaged. The roof might have been hit directly, missed by the core of the storm, shielded by size and trajectory, already vulnerable, recently replaced, previously damaged, or completely unaffected. The only responsible way to move from exposure to damage is to add property-specific evidence.

That distinction matters for every Asset Optimix audience. Roofers need to prioritize inspection without promising an outcome. Owners need to decide whether to document the roof after a storm. Brokers need to avoid overstating storm impact in a sale process. Buyers need to know whether exposure changes diligence. Lenders need to understand whether reserves or conditions should change. Insurers and insurtech teams need to separate hazard signals from observed condition.

The central rule is simple: weather records can justify attention, but roof-specific evidence must support roof-specific conclusions.

Why the distinction matters commercially

The gap between exposure and damage is not only a technical point. It changes money, timing, trust, and risk allocation.

If a hail exposure record is treated as proof of damage, a roofer may overpromise, an owner may expect a coverage result, a buyer may demand a credit without enough evidence, and a broker may create conflict in diligence. If a hail exposure record is ignored, a vulnerable roof may go uninspected after a meaningful event, a lender may rely on stale condition evidence, and an owner may miss the chance to document a roof before small problems become larger.

The disciplined middle path is better:

- Treat hail records as exposure context.

- Identify whether the roof assembly was vulnerable.

- Check whether there is current property-specific evidence.

- Record whether inspection occurred after the event.

- Separate observed roof condition from weather history.

- Decide what next action is proportionate.

This approach supports a better commercial conversation. A roofer can say, "A severe hail report occurred near this property, and your roof has older exposed accessories and no post-event photos. The next step is inspection." That is different from saying, "The storm damaged your roof." The first statement is useful and honest. The second requires evidence that the speaker may not have.

For owners and asset managers, the distinction supports governance. A portfolio may include hundreds of roofs across multiple markets. Not every building near hail deserves the same urgency. The buildings with older membranes, high tenant consequence, dense rooftop equipment, weak records, or no recent photos should move first.

What a public hail record can tell you

Public hail records are valuable, but they have limits. NOAA/NCEI Storm Events data, National Weather Service criteria, local storm reports, radar-derived products, and field observations can provide context about severe weather in an area. They help answer questions such as:

- Did severe weather occur near the property?

- What date and approximate time matter?

- Was hail reported, and what size was reported?

- Were damaging wind reports also present?

- Was the event part of a larger storm system?

- Was the reported hail size severe by public criteria?

- Did the event occur before or after the last roof inspection?

Those are powerful inputs. They can help triage inspection, organize owner records, and explain why a roof file should be updated.

They do not answer every question:

- They do not prove hail hit the roof surface.

- They do not prove the reported size occurred at the parcel.

- They do not prove damage to the roof membrane, flashing, insulation, deck, or rooftop equipment.

- They do not identify pre-existing conditions.

- They do not interpret warranty terms.

- They do not decide insurance coverage.

- They do not replace qualified roof inspection.

The record is the beginning of the chain, not the end. That is why the existing [roof weather risk and physical underwriting guide](/insights/roof-weather-risk-physical-underwriting/) separates hazard, vulnerability, observed condition, consequence, and evidence confidence.

Severe hail thresholds help frame attention

The National Weather Service commonly uses one inch diameter hail as a severe thunderstorm criterion. That threshold is useful because it gives teams a shared language for why a hail event deserves attention. A one-inch report near an older roof with exposed accessories is more meaningful than vague memory that "it hailed around here."

But threshold language still does not prove roof damage. It only helps classify the weather event. A commercial roof decision still needs more context:

- How close was the report to the property?

- Was the report measured, estimated, or relayed?

- Did the storm core pass directly over the building?

- What was the roof system and age confidence?

- Were rooftop accessories exposed?

- Was the roof inspected after the event?

- Are there new leaks, punctures, displaced components, or marked impact patterns?

- Are there photos from before and after the event?

The threshold should trigger a better evidence request, not a shortcut. It can also help prioritize. A portfolio owner may decide that buildings within a certain exposure window and with low condition confidence deserve roof photos within a defined period. That is not a damage conclusion. It is a disciplined maintenance and underwriting response.

Spatial uncertainty is part of the file

Hail is uneven. A report in a town, county, or ZIP code does not mean every building in that area received the same hail. Storm paths can be narrow. Hail size can change quickly. Wind direction, storm speed, building location, and observation quality all affect the record.

For commercial property underwriting, spatial uncertainty should be named. A roof file might say:

"NOAA/NCEI record shows severe hail reported in the area on May 8, 2026. The property-specific roof impact is not confirmed. No post-event roof inspection was provided. Current roof condition confidence is low."

That statement is much stronger than either extreme. It does not ignore the storm. It does not turn the storm into proof.

Spatial uncertainty also matters for multi-building campuses. One building may have rooftop equipment on the exposed west side. Another may have a newer membrane and fewer penetrations. A third may have an older canopy with poor records. Treating the campus as one hail outcome can mislead the reserve and inspection plan.

For roofers, this means outreach should be property-specific. A map can start the conversation, but the next step should be a roof-specific inspection, record request, or photo update. For lenders and buyers, spatial uncertainty means the diligence question should be framed as missing evidence rather than confirmed loss.

Time matters as much as location

A hail exposure record becomes more useful when it is tied to the roof timeline. The same storm record means different things depending on what happened before and after it.

Important timeline questions include:

- Was the roof installed before or after the hail event?

- Was a recover, coating, restoration, or repair completed after the event?

- Was there a post-event inspection?

- Were new leaks reported after the event?

- Were rooftop equipment repairs or replacements completed after the event?

- Was a PCA performed before or after the event?

- Did the insurance placement or lender review rely on pre-event roof evidence?

- Are current photos older than the hail event?

If a PCA was completed two months before a severe hail event, the PCA may no longer be enough for roof confidence. The building may still be fine, but the condition evidence is stale relative to the exposure. If a roof was inspected after the event and no relevant distress was observed, confidence may improve. If a roof was repaired after the event but the repair scope is vague, the file needs more detail.

This is why Asset Optimix treats weather exposure as a timeline input. A weather record does not stand alone. It interacts with roof age, condition, maintenance, inspection dates, and consequence.

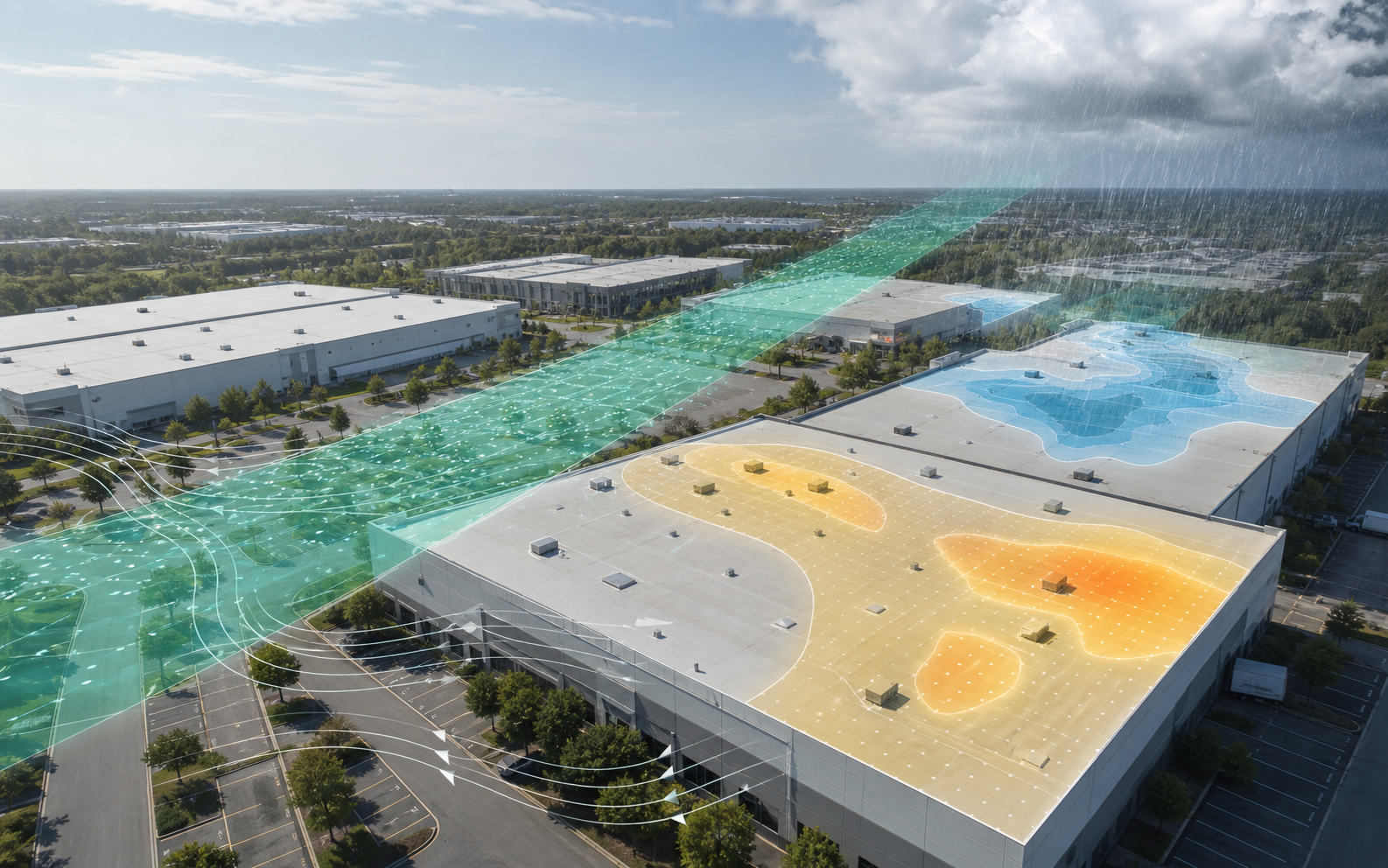

Roof vulnerability decides whether exposure is important

Not every exposed roof deserves the same urgency. Vulnerability changes the meaning of a hail record.

Vulnerability factors include:

- Roof age confidence.

- Membrane type and condition.

- Recover or coating history.

- Prior hail or wind exposure.

- Existing repairs and patch density.

- Exposed insulation or weakened surfacing.

- Brittle, aged, or poorly maintained components.

- Rooftop equipment density.

- Skylights, vents, hatches, and accessories.

- Edge, coping, and flashing condition.

- Drainage and ponding patterns.

- Tenant consequence if water intrusion occurs.

A newer documented roof with recent inspection photos may have lower immediate concern after a modest nearby hail report than an older unknown roof with repeated repairs, exposed accessories, and no access record. The weather record is the same type of input, but the building-level decision is different.

This is the heart of physical underwriting. The goal is not to label a storm as good or bad. The goal is to connect hazard, vulnerability, evidence quality, and consequence.

The [roof age confidence bands guide](/insights/commercial-roof-age-confidence-bands/) explains why age should be section-level and evidence-based. That same discipline applies to hail. A hail exposure near an unknown roof section is a different problem than a hail exposure near a documented, recently inspected section.

Rooftop equipment can carry the evidence

Commercial roofs are not only membranes. They are mechanical platforms. HVAC units, vents, hatches, skylights, satellite mounts, pipe supports, screens, exhaust fans, and other accessories can provide important condition evidence after hail exposure.

Accessory evidence can include:

- Dented metal housings.

- Damaged fins.

- Broken or cracked plastic components.

- Marks on vent caps.

- Damage to skylights or domes.

- Displaced covers.

- New sealant work.

- Damaged screens.

- Impact marks near curbs or penetrations.

Accessory evidence still needs careful interpretation. Dents can be old. Some components may have been damaged before the event. Maintenance traffic can create unrelated marks. A current photo without a pre-event baseline may show condition but not timing.

The value is that accessories help build a property-specific record. If a roof inspection after a documented hail exposure shows consistent impact marks on exposed metal components and related membrane distress, the file is stronger than a weather record alone. If the roof inspection shows no relevant evidence, that is also useful. It can improve confidence and prevent unnecessary speculation.

For roofers, accessory photos should be organized by location and date. For owners, they should be kept with the roof file. For buyers and lenders, they should be read as evidence that still requires professional context.

Interior leaks are not automatically hail damage

After a storm, interior leaks often drive urgency. A tenant calls. A ceiling tile stains. A maintenance team finds water. The owner naturally connects the leak to the storm. Sometimes that connection is correct. Sometimes the storm only revealed an older defect. Sometimes the water entered through a wall, drain, curb, flashing, HVAC unit, or plumbing issue rather than hail-created roof damage.

The file should separate:

- Date and time of the leak.

- Location of the leak inside the building.

- Weather conditions at the time.

- Roof area above or near the leak.

- Roof inspection findings.

- Existing repair history at that area.

- Photos of interior and exterior conditions.

- Whether the leak repeated after later rain.

- Repair scope and cause notes.

This matters because an interior leak can prove water entered the building, but it does not automatically prove why. If the roof has a known open seam, clogged drain, deteriorated curb, or old flashing issue, hail may not be the cause. If the roof has impact marks and new membrane fractures aligned with the event, the file may support a different conclusion.

For underwriting, a leak is a consequence signal and a condition trigger. It should move the building into follow-up. It should not skip the evidence chain.

Inspection evidence should be organized by confidence

Not all inspection evidence has the same weight. A useful post-hail roof file should organize evidence by confidence and scope.

| Evidence type | Strength | Limit |

|---|---|---|

| Dated roof inspection with mapped photos | Strong when performed by qualified personnel with access | May still exclude hidden moisture or inaccessible areas |

| Before-and-after roof photos | Strong when location and dates are clear | Needs consistent angles and roof-area mapping |

| Repair invoice tied to hail-related observations | Useful when scope and cause notes are specific | Invoice language may be narrow or ambiguous |

| Tenant leak log after event | Useful trigger | Does not prove hail cause |

| Aerial or remote imagery | Useful context | May miss membrane-level condition |

| Weather record | Important exposure input | Not property-specific damage proof |

| Owner memory | Starting point | Low confidence without supporting records |

The output should be honest. "Strong exposure record, weak property evidence" is a valid finding. So is "moderate exposure record, strong post-event inspection evidence." Those statements help the user decide what to do next.

This is especially valuable for insurance and insurtech teams. A confidence-labeled file can route follow-up without turning every weather record into a damage assumption.

Photos need location, date, and purpose

Roof photos are useful only when they are organized. A folder of unlabeled images is better than nothing, but it can still create confusion. The photo file should answer:

- When was the photo taken?

- Who took it?

- What roof area does it show?

- What direction or feature anchors the location?

- Was the photo before or after the hail exposure?

- Does the photo show overview context or detail evidence?

- Is the image tied to a finding, repair, or maintenance note?

For commercial roofs, context photos and close-up photos should work together. A close-up of a puncture without a location is weak. An overview photo without detail may be too broad. The best file shows the roof area, then the specific condition, then the surrounding features.

Photo discipline also protects against overclaiming. A roofer can show what was observed without making unsupported statements about cause. A broker can provide a dated condition file without certifying the roof. A buyer can ask targeted follow-up questions. A lender can see whether the evidence covers the roof areas that matter.

Hail exposure can make older records stale

A roof condition file is only useful relative to events that happened after it. If the last inspection predates a meaningful hail exposure, the file may be stale for underwriting. That does not mean the roof was damaged. It means the confidence level should be adjusted until current evidence is available.

Examples:

- A 2024 PCA describes the roof as serviceable, but a severe hail event occurred in 2025 and no post-event inspection is in the file.

- A seller provides 2023 roof photos, but the property was near multiple hail reports in 2024.

- A lender's reserve estimate was based on a pre-storm inspection.

- A buyer sees a warranty but no maintenance or post-event documentation.

- An insurer asks for roof condition evidence after a storm season, and the owner only has older photos.

The next action may be simple: collect new photos, schedule inspection, request repair history, or verify that no interior leak tickets followed the event. The important point is to record that the prior condition evidence predates the exposure.

Confidence should update when the roof file updates.

Brokers should avoid storm language that creates false certainty

When a building is marketed after hail in the area, brokers should be careful with storm language. The goal is not to hide exposure. The goal is to avoid turning exposure into a roof conclusion.

Weak language includes:

- "Roof not affected by hail" without post-event inspection evidence.

- "Hail damage present" without roof-specific findings.

- "No storm issues" when no records were reviewed.

- "Recent storm passed nearby, but roof is fine" without a dated source.

Stronger language is evidence-based:

- "Severe hail was reported in the market on April 12, 2026; seller has not provided post-event roof inspection records."

- "Seller provided post-event roof inspection photos dated April 20, 2026; buyer should review scope and limitations."

- "Tenant leak log requested; no storm-period leak tickets provided as of package date."

- "Roof condition statements are based on seller-provided documents and are not a roof certification."

This kind of language helps the deal. Buyers can underwrite more quickly when uncertainty is named early. Sellers avoid overclaiming. Roofers can be brought in for a practical inspection rather than a late-stage dispute.

The [broker flat-roof listing diligence guide](/insights/commercial-roof-broker-listing-diligence/) gives a broader pre-listing framework for roof records.

Buyers should price uncertainty, not just defects

A buyer may not know whether a hail exposure damaged the roof before closing. That uncertainty has value. The buyer should decide whether to inspect, ask for records, request a credit, adjust reserves, or proceed with a known caveat.

The key is to separate known defects from missing evidence.

Known defects might include observed membrane punctures, damaged flashing, cracked skylights, displaced components, or repeated leak locations. Missing evidence might include no post-event inspection, no current photos, no roof access, no repair history, or unclear roof age.

Those should not be priced the same way. A known defect is a scope and cost question. Missing evidence is a confidence question. Sometimes the confidence question is more important because it affects the buyer's ability to trust the rest of the file.

For 1031 exchange buyers, timing pressure can make this harder. A buyer may need to decide quickly whether a replacement property is acceptable. In that setting, a clean exposure and inspection file can be a competitive advantage. A vague hail history can slow diligence or push the buyer toward a larger uncertainty reserve.

Lenders need to know whether reserves rely on stale condition evidence

Lenders do not need every hail exposure to become a loan condition. They do need to know whether the roof reserve and condition file are current enough to support the decision.

A lender should ask:

- Did the property have meaningful hail exposure after the most recent roof observation?

- Were roof areas accessible during the PCA?

- Was remaining useful life estimated before or after the exposure?

- Are photos included and dated?

- Does the borrower have post-event maintenance or inspection records?

- Are there tenant leaks or repair invoices after the event?

- Does the roof age confidence change because records are weak?

If the roof has strong documentation and a recent post-event inspection, the lender may have enough information. If the roof has unknown age, high consequence, and only pre-event photos, the lender may need additional diligence or reserve conservatism.

This is not about turning a hail map into a financing problem. It is about making sure the physical evidence still matches the capital decision.

Insurers and insurtech teams need evidence routing

Insurance teams often have access to hail exposure data, roof age fields, policy history, inspections, photos, and loss-control notes. The challenge is routing attention without confusing exposure with damage.

A useful routing file might classify buildings like this:

| Exposure | Roof confidence | Condition evidence | Suggested routing |

|---|---|---|---|

| Severe hail near property | Unknown roof age, no photos | Low | Request inspection or owner documentation |

| Severe hail near property | Documented newer roof | Current post-event photos | Monitor, keep record current |

| Multiple hail exposures | Older roof, repair history | Medium | Prioritize loss-control review |

| Hail report in county only | Strong records, low consequence | Medium-high | Note exposure, no immediate action unless other signals appear |

This keeps the workflow proportionate. It also supports better conversations with producers, insureds, and risk engineers. Instead of saying "hail risk is high," the file can say "exposure is present, but property-specific condition evidence is missing." That is a more useful underwriting sentence.

Roofers should build an evidence-first storm workflow

Storm response can be a sensitive sales environment. A commercial roofer who leads with evidence will usually create more durable trust than one who leads with certainty.

An evidence-first workflow:

- Identify properties with relevant hail exposure.

- Check roof age confidence and prior condition evidence.

- Prioritize buildings with vulnerable roofs, high tenant consequence, or stale photos.

- Offer a property-specific inspection or documentation update.

- Photograph roof areas and accessories with location context.

- Separate observed condition from possible cause.

- Provide repair or maintenance recommendations only where supported.

- Encourage owners to keep records with warranties, maintenance logs, and leak history.

The roofer's advisory value is not limited to damage discovery. A post-hail inspection that finds no relevant condition can still be valuable because it improves confidence. It gives the owner a dated record. It gives a buyer, lender, or insurer a stronger file later. It can also identify unrelated maintenance issues that deserve attention.

What a post-hail roof file should include

A commercial post-hail roof file should be compact but complete enough to support future decisions.

| File item | Purpose |

|---|---|

| Event date and source | Connects weather record to timeline |

| Roof section map | Prevents one conclusion from covering all roof areas |

| Roof age confidence | Shows how well each roof area is documented |

| Inspection date and access notes | Explains what was observed and what was not |

| Overview photos | Shows roof areas and context |

| Detail photos | Shows observed conditions |

| Rooftop equipment photos | Records accessory condition |

| Leak and tenant log review | Captures consequence and timing |

| Repair history | Separates old issues from new observations |

| Next action | Turns evidence into maintenance, inspection, reserve, or monitoring |

The file should also include limits. If no moisture scan was performed, say so. If a roof area was inaccessible, say so. If the inspection was visual only, say so. If cause was not determined, say so.

Limits do not weaken the file. They make it credible.

Avoiding common hail record mistakes

The most common mistakes are predictable:

- Treating a nearby hail report as roof damage proof.

- Ignoring meaningful hail exposure because no leak was reported.

- Using pre-event photos as current condition evidence.

- Failing to separate roof sections.

- Ignoring rooftop equipment and accessories.

- Describing dents or marks without location or date.

- Treating owner memory as inspection evidence.

- Confusing warranty status with roof condition.

- Assuming a coating or repair reset hail vulnerability.

- Making coverage or claim conclusions from roof observations alone.

The fix is also predictable: build a file that separates weather exposure, roof vulnerability, observed condition, consequence, and confidence.

Hail exposure can support better capital planning

Hail exposure is not only an insurance question. It can affect capital planning even when there is no immediate claim, dispute, or emergency.

After a meaningful hail exposure, an owner may decide to:

- Move inspection sooner.

- Refresh roof photos.

- Update reserve timing.

- Review rooftop equipment condition.

- Reconcile leak logs.

- Confirm warranty maintenance duties.

- Budget for targeted repairs.

- Adjust replacement planning for older sections.

- Prioritize high-consequence tenant areas.

That is good asset management. It turns weather into a maintenance and documentation trigger rather than a panic event. The existing [commercial roof capex and reserve planning guide](/insights/commercial-roof-capex-reserve-planning/) explains why roof reserves should change when new evidence changes timing, confidence, or consequence.

The right output is a decision note, not a verdict

The most useful hail output is not "damaged" or "not damaged" unless the evidence supports that level of conclusion and the right professional has made it. For many business workflows, the better output is a decision note:

"Severe hail was reported near the property on May 8, 2026. Main roof age is supported by 2018 invoice, but no post-event roof photos are in the file. Rooftop equipment density is high over the production area. Tenant leak log shows no reported leaks after the event. Recommended next action: schedule roof and rooftop equipment inspection before renewal and reserve update."

That note is more useful than a raw weather map. It connects exposure, roof age confidence, evidence gaps, consequence, and next action. It also avoids pretending to decide matters that require inspection, professional judgment, warranty review, or insurance coverage review.

This is where commercial roof prediction can help. The value is not in turning every storm into an alarm. The value is in telling the user which buildings deserve attention, why they deserve it, what evidence is missing, and what action is proportionate.

Multiple hail events need a chronology

Many commercial roofs do not face one clean hail question. They sit through several storm seasons. A public record may show hail in 2022, another event in 2024, and a larger event in 2026. The roof may have been inspected after one event, repaired after another, and photographed only before the most recent exposure. If those events are not organized in order, the file becomes confusing quickly.

A chronology should include:

- Event date.

- Weather source.

- Approximate location relationship.

- Reported hail size or severity context.

- Roof age and work status at the time.

- Inspection or photo response.

- Leak or tenant response.

- Repair or maintenance response.

- Confidence after the response.

This helps answer a practical question: which event, if any, changed the roof evidence? A roof may have a meaningful 2024 hail exposure, but if a full roof inspection and repair package followed in 2025, the current evidence may be stronger than it looks from a weather map. Another roof may have modest hail exposure in several years and no inspection after any of them, which makes the confidence problem grow over time.

The chronology also protects against assigning all observed distress to the most recent event. A split, puncture, dent, leak, or patch may predate the last storm. Without prior photos or repair records, timing can be uncertain. The file should say when timing is uncertain.

For buyers and lenders, this matters because a single severe event may look alarming, but an uninspected sequence of smaller events can be just as important for confidence. For roofers, it creates a clearer inspection plan. For insurers, it helps separate exposure history from event-specific evidence.

Pre-existing condition should be documented, not ignored

Hail exposure should never erase the roof's prior condition. A roof with old open seams, brittle membrane, ponding, patched curbs, or deteriorated flashing may leak after a storm because the storm stressed weak points. That does not automatically mean hail created the underlying condition. It means the roof file needs to separate what existed before from what was observed after.

Pre-existing condition evidence may include:

- Prior inspection photos.

- Older repair invoices.

- Maintenance logs.

- Tenant leak history.

- PCA observations.

- Warranty service records.

- Roof consultant notes.

- Aerial history.

- Seller disclosures or owner records.

A strong post-hail workflow begins by reading the pre-event file. If the same leak area appeared in work orders for three years, the event may not be the only explanation. If the roof had no prior leak record but shows new, consistent exterior evidence after the event, the file points in a different direction. The goal is not to decide causation casually. The goal is to keep the evidence organized so the right professional can evaluate it.

This is important in sale and lending contexts. A seller may prefer to describe all post-storm roof issues as storm-related. A buyer may prefer to treat all roof uncertainty as a seller credit. A lender may only care that the roof condition and reserve are understood. A disciplined file helps everyone stay closer to the evidence.

Warranty questions should stay separate from damage questions

Warranty status often appears in hail conversations because commercial roofs may have manufacturer, contractor, material, workmanship, coating, or maintenance-related warranty documents. The existence of a warranty does not answer the hail question. A warranty may include exclusions, maintenance duties, notice procedures, transfer rules, and scope limits. It may cover some conditions and exclude others. It may require specific documentation or inspection steps.

The roof file should separate:

- Is there a warranty?

- What roof areas does it cover?

- Is it transferable?

- What maintenance duties apply?

- What exclusions or limits are visible in the document?

- Was notice required after a storm?

- Was any warranty inspection or service performed?

- Does the warranty relate to the observed condition?

This is not legal advice and not warranty interpretation. It is file discipline. A broker should avoid saying "hail is covered" or "hail is not covered" unless the proper party has reviewed the actual terms. A buyer should request the warranty and ask qualified advisors to review it. A roofer should describe observed roof condition and known document limits without becoming the owner's legal advisor.

Warranty evidence can still be useful. It may prove installation date, contractor identity, system type, covered areas, or maintenance expectations. That can improve roof age confidence and help decide what records should be gathered after hail exposure.

Municipal and public portfolios need defensible prioritization

Municipalities, school districts, counties, and other public owners often manage many roofs with limited capital. A hail event can create pressure to inspect everything at once. That may not be realistic. A defensible prioritization model helps public owners show why one building moved ahead of another.

Useful prioritization fields include:

- Hail exposure strength.

- Roof age confidence.

- Last inspection date.

- Known roof condition.

- Critical service housed in the building.

- Public occupancy and continuity needs.

- Existing leaks or complaints.

- Warranty or procurement constraints.

- Drainage and equipment vulnerability.

- Estimated consequence of delayed inspection.

The output should be transparent. "Building A moved first because it houses emergency operations, has unknown roof age, no post-event photos, and was near a severe hail report" is easier to defend than "Building A looked risky." Public owners need records that can survive internal review, board questions, budget debate, and procurement timing.

The same logic applies to private portfolios. A national owner with hundreds of retail, industrial, office, or multifamily assets needs a consistent triage method. Hail exposure is one input. Consequence, condition, and confidence decide the order.

When the next action should be inspection

Not every exposure record requires immediate roof inspection, but some combinations should move quickly.

Inspection should be strongly considered when:

- Severe hail was reported near the building and current roof photos are older than the event.

- Roof age is unknown or inferred.

- The roof is older or near a reserve decision.

- High-value tenant operations sit under the exposed roof area.

- Leak complaints appeared after the event.

- Rooftop equipment is dense or visibly affected.

- The roof has prior repairs in the same area.

- A sale, refinance, renewal, or reserve decision depends on current condition.

- The building has no recent roof inspection at all.

- A prior inspection excluded roof access.

Inspection may be less urgent when the exposure is weak, the roof has current post-event photos, no leak or repair signals emerged, roof age is documented, and consequence is low. Even then, the file should note why immediate action was not taken.

The point is proportionality. Hail exposure should create a reasoned action, not automatic alarm and not automatic dismissal.

Bottom line

Hail records matter. They can identify exposure, support inspection priority, refresh stale roof files, and help roofers, owners, brokers, buyers, lenders, and insurers ask better questions. But hail exposure is not roof damage. Property-specific roof condition evidence is the bridge between the two.

A disciplined commercial roof file should separate the event record, the roof's vulnerability, the inspection evidence, the tenant or operational consequence, and the confidence level. It should name limits. It should avoid coverage conclusions. It should move the building toward the next responsible action.

That is the difference between using weather as a blunt alarm and using weather as part of physical underwriting.

Frequently asked questions

Does a hail report prove commercial roof damage?

No. A hail report can show exposure near a property, but roof-specific damage conclusions require property-specific evidence such as inspection findings, photos, repair records, and professional judgment.

When should a commercial roof be inspected after hail exposure?

Inspection should be considered when severe hail was reported near the property and roof photos are stale, roof age is unknown, tenant consequence is high, leaks appeared after the event, or a sale, loan, renewal, or reserve decision depends on current condition.

Can hail exposure affect a roof reserve even without confirmed damage?

Yes. Exposure can lower confidence in stale condition evidence and justify updated photos, inspection, or reserve review. It should still be separated from confirmed property-specific roof damage.

Sources and limits

Research basis reviewed against NOAA/NCEI storm records, National Weather Service severe hail definitions, WBDG, FEMA, IBHS, ASTM PCA framing, Fannie Mae PCA guidance, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence, observed condition, and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, useful life, and repair needs.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.