Commercial roof intelligence

How Commercial Roofs Fail Before the Leak: A Field Guide for Owners, Roofers, Brokers, and Underwriters

Most commercial roof losses are not a mystery leak. They are a chain of drainage, membrane, flashing, traffic, equipment, weather, and record-quality signals that become expensive when nobody owns the timeline.

Key takeaways

- A commercial roof usually fails as a system: drainage, membrane, edge, penetrations, traffic, weather, and records interact.

- The most valuable early signals are often mundane: ponding locations, repeated patch zones, clogged drains, HVAC penetrations, tenant leak tickets, and repair chronology.

- Weather history should raise inspection priority when it aligns with vulnerability, but it does not prove damage by itself.

- Physical underwriting improves when roof evidence is separated into hazard, vulnerability, observed condition, consequence, and confidence.

The useful answer is not "flat roofs leak"

Commercial roof failure is usually discussed too late. The tenant has a stained ceiling tile, the property manager has an angry call, the roofer is looking at a patch that failed twice, the broker is waiting on diligence, or the underwriter has a roof-age note that does not match the building's apparent condition. By that point the roof is already being treated as a problem. The better question is what changed before the leak became visible.

Asset Optimix treats commercial roof risk as a chain of conditions. A low-slope roof can have one weak membrane area, but the expensive outcome usually needs several pieces to line up: water that does not leave fast enough, a membrane that has lost flexibility, a flashing detail that moves differently from the field, a penetration that was never resealed after equipment work, repeated foot traffic, heat cycling, wind uplift at an edge, or a record gap that keeps everyone from knowing which repair happened when.

That framing matters because different people enter the roof conversation with different incentives. A commercial roofer wants to find roofs that deserve attention before a competitor gets the emergency call. A property owner wants to avoid replacing too soon or waiting too long. A broker wants a credible story before a buyer turns uncertainty into a price reduction. An underwriter wants to know whether the roof is maintained, vulnerable, or unknown. A lender wants reserve logic that survives scrutiny. A tenant wants business interruption avoided. All of them need the same thing first: a more organized roof file.

The roof file does not have to be perfect. It needs to separate five categories:

- Hazard: weather, heat, wind, rainfall, hail, debris, freeze-thaw, rooftop work, and foot traffic.

- Vulnerability: age band, membrane type, drainage geometry, roof edges, flashings, penetrations, equipment, repairs, and workmanship clues.

- Observed condition: ponding, stains, splits, open seams, punctures, displaced ballast, clogged drains, soft insulation, corrosion, and recurring leak areas.

- Consequence: tenant sensitivity, inventory exposure, operating interruption, mold concern, electrical exposure, refrigerated space, critical process areas, and reputation.

- Confidence: records, inspection quality, photo coverage, roof access, source conflicts, and recency.

When those categories are mixed together, roof decisions become emotional. When they are separated, the next action becomes easier to defend.

Commercial roof failure is a system problem

Most commercial roofs are assemblies, not single products. A roof may include a structural deck, vapor control layer, insulation, cover board, membrane, attachment system, ballast or coating, flashing, coping, drains, scuppers, gutters, expansion joints, walk pads, curbs, skylights, hatches, pipes, and rooftop mechanical equipment. Each element can perform acceptably by itself and still create risk where it meets another element.

The Whole Building Design Guide describes roofs as part of the building enclosure, where moisture control depends on design, construction quality, commissioning, inspection, and maintenance. Its moisture-management discussion is useful because it does not treat water as one thing. Bulk water, capillary water, vapor diffusion, and air leakage move differently. A roof can shed rainwater and still have condensation risk. A roof can be watertight at the membrane field and still fail at an air-leakage or flashing condition. A roof can have no active interior leak and still hold wet insulation that changes thermal performance and future repair scope.

This is why single-factor roof scoring is weak. A roof is not simply "15 years old" or "TPO" or "had hail nearby." The decision-quality question is how the assembly is behaving under its actual exposure. Two roofs installed in the same year can diverge quickly if one has interior drains that clog, ponding along a parapet, heavy mechanical service traffic, grease discharge, unprotected walk routes, and repeated storm exposure while the other drains cleanly and has disciplined maintenance records.

Commercial roofs also fail across timescales. Some failure modes are sudden, such as wind-related perimeter damage or a puncture from equipment work. Others are slow, such as UV degradation, seam fatigue, corrosion, trapped moisture, or repeated minor ponding. Many losses combine both. A roof that has been weakened by years of heat, traffic, and small repairs may be the roof that opens during a severe wind event. The wind may be the trigger, but the vulnerability was already present.

That distinction matters for underwriting and for sales ethics. Weather history can justify inspection priority, but it should not be used as a shortcut around roof condition. A maintenance history can show care, but it should not erase a new hazard event. A good roof-intelligence workflow puts both on the table.

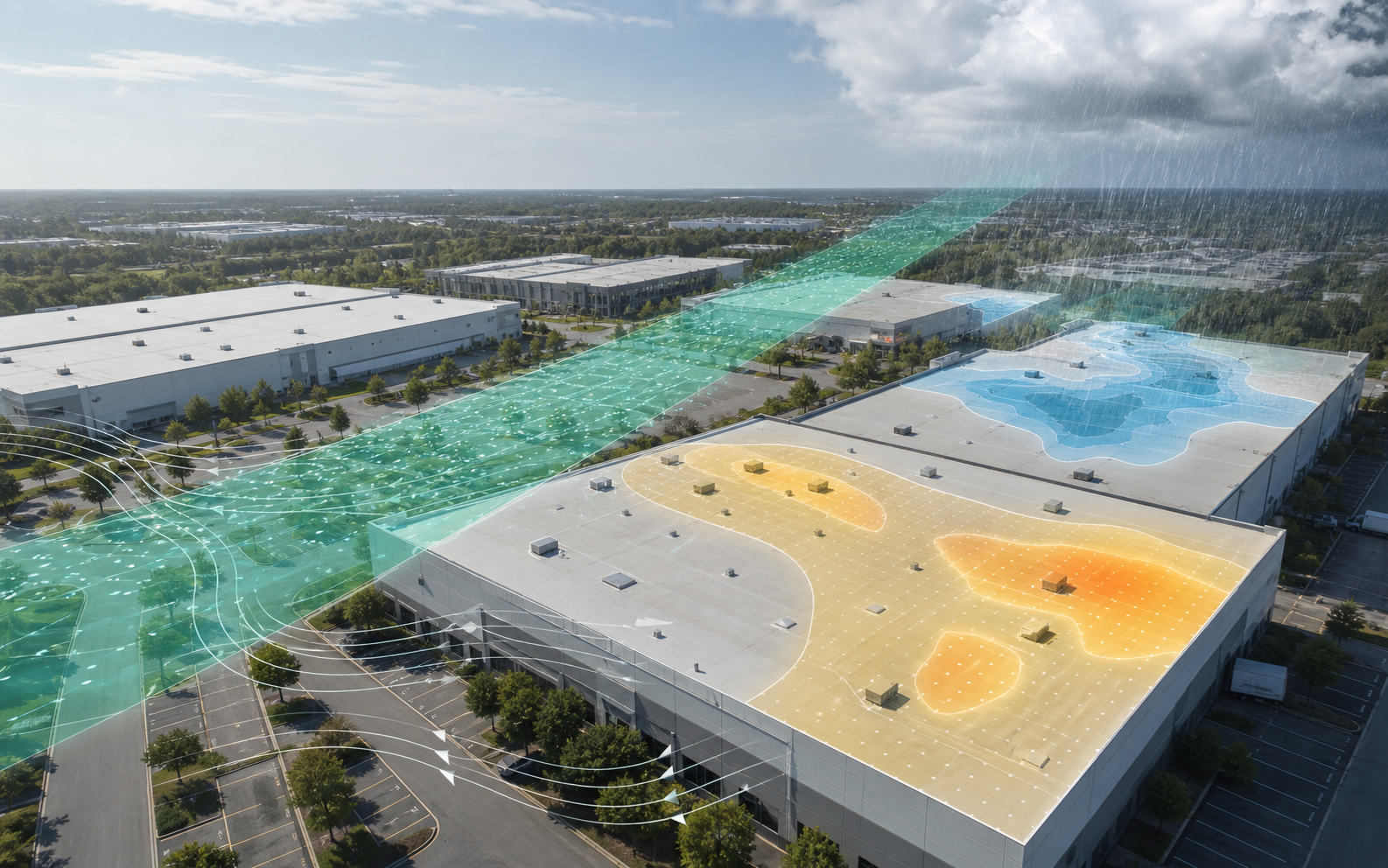

Drainage failure is often the first quiet signal

Commercial roof decisions should start with water movement. Even a roof called "flat" is supposed to move water to drains, scuppers, gutters, or other disposal points. The U.S. EPA moisture-control guidance notes that low-slope roof design should collect and dispose of rainwater, and it discusses slope to drain in the context of maintenance and moisture control. WBDG roofing guidance similarly emphasizes roof drains, valleys, gutters, downspouts, and ponding risk.

Ponding is not just a cosmetic observation. Standing water adds load, slows drying, carries contaminants, concentrates heat, masks membrane defects, encourages biological growth, and makes a small surface irregularity more important. If the same roof zone holds water after storms, that zone deserves its own history. When was the ponding first documented? Does it line up with a roof deck deflection, crushed insulation, a blocked drain, a bad taper layout, an added rooftop unit, or a repair that changed water flow?

The most useful drainage observations are boring and repeatable:

- Which drains or scuppers serve each roof zone.

- Whether strainers are present, damaged, or blocked.

- Whether water stains radiate from a drain bowl or parapet.

- Whether there are sediment rings that show recurring ponding.

- Whether previous patch areas sit inside ponding zones.

- Whether walk pads direct traffic through wet areas.

- Whether rooftop equipment condensate drains onto the roof surface.

- Whether gutters and downspouts discharge away from the building.

For a roofer, drainage patterns help prioritize inspection. For an owner, they help decide whether a repair is likely to hold. For a broker, they explain why a buyer's inspector keeps returning to the same roof zone. For an underwriter, they separate a general "older roof" concern from a specific condition that increases loss probability.

The dangerous habit is treating every ponding mention as the same. A shallow area that dries quickly after normal rain is different from persistent water near a seam, drain, penetration, or parapet. A one-time blocked drain after a storm is different from recurring ponding visible in multiple photo sets. A good file should record location, duration, recurrence, and relationship to defects.

Membranes rarely fail in isolation

The membrane field gets attention because it is visible. Cracks, splits, punctures, open laps, blisters, fishmouths, wrinkles, loose seams, exposed reinforcement, coating loss, and brittle areas all deserve documentation. But membrane observations become more valuable when they are tied to cause and context.

A puncture near an equipment path is different from widespread weathering. A split at a transition may be movement-related. A blister can be a moisture, adhesion, vapor, or installation clue. A repair patch can be good evidence of maintenance or evidence of recurring distress, depending on age, workmanship, location, and whether the same area has been patched before. A roof that looks clean from satellite imagery can still have seam issues, punctures, or flashing defects that only close inspection will find.

Membrane vulnerability also changes with climate and use. Heat and ultraviolet exposure affect material aging. Hail and wind exposure can create impact or uplift concerns. Grease, chemicals, standing water, and mechanical discharge can accelerate deterioration in specific locations. Foot traffic can damage areas far from the original defect. The roof's material label is not enough; the relevant question is how that material is performing under this building's actual service conditions.

This is where prediction can add value without pretending to be inspection. Remote and records-based signals can identify where membrane risk is more likely:

- Older age band with high heat exposure.

- Repeated severe weather near a vulnerable material or edge condition.

- Large low-slope areas with many penetrations.

- Roof zones around heavily serviced equipment.

- Deterioration seen across dated imagery or inspection photo sets.

- Recurring repair invoices that name the same roof area.

- Tenant work orders that map to the same bay, suite, or roof drain.

The model should not say "the membrane is failed" without inspection support. It can say "this membrane should be treated as higher-priority for inspection because vulnerability and consequence are both elevated." That is a more defensible statement and a more useful one.

Flashing and transitions deserve more attention than the field

Many commercial roof leaks start where the roof has to change direction, attach to something, or pass around something. Parapets, curbs, walls, expansion joints, edge metal, skylights, hatches, pipe penetrations, drains, and equipment supports are all transition details. They move differently, age differently, and are touched more often than the open roof field.

WBDG roofing-system guidance calls out flashing at transitions, penetrations, and termination points as a factor in reducing moisture intrusion. That is consistent with field reality. A membrane field can be serviceable while a poorly maintained curb or wall flashing lets water in. A roof can have a recent repair in the field while the real issue is counterflashing, coping, sealant, or a mechanical curb that moves under service loads.

Transition failures often have a record trail. Look for invoices that mention "reseal," "counterflashing," "curb," "pitch pan," "pipe boot," "drain bowl," "parapet," "coping," "termination bar," or "edge metal." A repeated vocabulary pattern can be more useful than a generic roof age estimate. If three invoices over four years mention the same set of curbs, that is not random maintenance. It is a location-specific roof story.

For underwriters and buyers, transition risk should be treated as an evidence-quality issue. A property file that says "roof replaced in 2018" may still be weak if it does not show how rooftop equipment, curbs, drains, and edge metal were handled. A roof replacement can leave legacy penetrations, unusual transitions, or poorly documented tie-ins. The question is not just when the membrane was installed. The question is whether the roof system's weak points were addressed, photographed, and maintained.

Perimeter edges are small areas with large consequences

Wind-related roof failures often begin at edges, corners, and transitions where uplift pressure and attachment details matter. The Insurance Institute for Business & Home Safety has emphasized commercial-building wind vulnerabilities that include roof membrane, perimeter edge flashing, roof-mounted equipment, load path, openings, and over-pressurization. That list is useful because it connects roof performance to the rest of the building.

Perimeter conditions can turn a local defect into a larger loss. Edge metal that is loose, poorly attached, corroded, or damaged can expose membrane edges. Coping problems can introduce water into parapet assemblies. Wind can exploit small openings. Once a roof cover begins to peel or lift, water intrusion and business interruption can follow quickly. The owner experiences the event as sudden. The evidence file may show that vulnerability existed long before the wind.

A practical roof-risk review should separate field condition from perimeter condition. A roof can look stable in the middle and still have poor edge details. The inspection or photo request should cover corners, parapets, coping joints, edge metal, terminations, and any place where the roof connects to a wall or vertical surface.

Perimeter evidence also matters in channel partnerships with roofers. A roofer can use a risk screen to prioritize which buildings merit a perimeter-focused inspection after high winds, especially where the roof has older age, large open exposure, prior repairs, or rooftop equipment that complicates airflow. The workflow should be framed as inspection priority, not a promised claim or a scare tactic.

Rooftop equipment can be the roof's busiest risk zone

Commercial roofs are work platforms. HVAC units, exhaust fans, refrigeration equipment, grease ducts, solar arrays, satellite equipment, conduit, security hardware, and tenant improvements bring people and penetrations onto the roof. Every new curb, conduit, support, drain line, or service path can change roof risk. The roof may be designed as a weather barrier, but it is often used as mechanical real estate.

Rooftop equipment creates several kinds of risk:

- Penetration risk where pipes, curbs, supports, or fasteners pass through the roof assembly.

- Service traffic risk from technicians walking the same routes.

- Chemical or grease risk near exhaust and food-service equipment.

- Condensate risk when discharge is not piped correctly to drains.

- Wind risk for equipment supports, panels, and attachments.

- Documentation risk when tenant or vendor work is not added to the roof file.

WBDG roofing guidance notes the need to inspect and reseal roof-mounted equipment penetrations over time and points to condensate discharge as a membrane damage concern. That is exactly the kind of maintenance detail that disappears in asset-level summaries. The roof may have a replacement date, but does the file show who cut in the last curb? Does the warranty include the later rooftop work? Did anyone photograph the completed flashing? Did a mechanical vendor use proper walk paths?

For owners and asset managers, rooftop equipment should be mapped. A simple roof plan with equipment IDs, service routes, known penetrations, and past repair locations can outperform a vague annual roof note. For roofers, equipment density is a strong prospecting signal because dense equipment creates recurring inspection needs. For underwriters, equipment changes can explain why a roof's risk changed after the original installation.

Foot traffic turns maintenance into exposure

Roof access is necessary. It is also a source of damage. A commercial roof that supports frequent HVAC service, sign work, telecom access, kitchen exhaust maintenance, solar inspections, or tenant vendors needs a traffic plan. Without one, the roof experiences repeated concentrated loads, abrasion, dropped tools, crushed insulation, punctures, and damage near ladders, hatches, and equipment.

Traffic risk is easy to under-document because nobody thinks of a service walk as a roof event. But the pattern shows up over time. Patches cluster between the hatch and the equipment. Walk pads end before the final turn. A technician takes a shortcut across a wet area. A heavy panel is staged on unsupported membrane. Debris sits near a curb. These are not dramatic events, but they can move a roof from normal aging to recurring repair.

The inspection request should include access points and service routes, not only defect photos. A portfolio owner can ask for:

- Photos from each roof access point.

- Walk pad layout and missing walk pad gaps.

- Repeated traffic routes to major equipment.

- Evidence of crushed insulation or low spots along paths.

- Debris, abandoned materials, and loose fasteners.

- Vendor work areas and recent penetrations.

- Interior leak tickets below frequent service zones.

For a roofer-led sales workflow, foot traffic is a useful educational angle because it does not require fear. The message is simple: the roof is also a platform, and platforms need routing, inspection, and housekeeping.

Weather exposure is a priority signal, not a verdict

Weather belongs in every commercial roof-risk file, but it has to be used carefully. The NOAA/NCEI Storm Events Database contains records used for official Storm Data publication and includes significant events such as hail, thunderstorm wind, tornadoes, and other hazards. The National Weather Service defines a severe thunderstorm using criteria that include hail at least one inch in diameter, wind of at least 58 mph, and/or a tornado.

Those records are valuable. They are not parcel-level roof inspections. A severe storm report near a building can raise the inspection priority, especially when the roof has known vulnerability. It does not prove a specific membrane was damaged, that a claim is covered, or that a roof replacement is required. The same weather exposure may have different consequences for different roof systems, ages, edges, attachment methods, drainage conditions, and maintenance histories.

The right workflow is:

- Identify the event type, date, and proximity.

- Compare the event to roof vulnerability.

- Check whether observed condition changed after the event.

- Review tenant complaints, leak tickets, and repair invoices around the event window.

- Document the inspection decision and remaining uncertainty.

This protects everyone. Roofers can explain why a building deserves inspection without overpromising. Owners can decide whether to document before the next rain. Underwriters can distinguish exposure from condition. Brokers can avoid presenting storm history as either irrelevant or conclusive. The model can surface high-priority roof zones without pretending it saw damage that only field review can verify.

Weather is most powerful when combined with chronology. A hail event, then a roof inspection, then photos, then a repair invoice, then no further leak tickets is a different story than a hail event, no inspection, a tenant complaint three weeks later, and two patch invoices in the same area. The point is not to force causation. The point is to organize time.

Roof age is useful, but age without records is weak

Commercial roof age is a common underwriting and diligence field because it is easy to ask for. It is not always easy to prove. A building may have a partial replacement, overlay, recover, coating, localized restoration, tenant-driven rooftop work, or repairs that sound like replacement in a spreadsheet. One section may be newer than another. A roof may have been installed before the current owner acquired the building. Permit databases can be incomplete or ambiguous. Warranty documents can exist but not transfer. Invoices can be missing.

The useful answer is an age confidence band:

| Evidence | What it can support | What it cannot support by itself |

|---|---|---|

| Permit record | Work date, jurisdiction record, possible scope | Exact assembly condition or whether all roof areas were included |

| Contractor invoice | Scope, date, materials, contractor, payment trail | Current condition without later inspection |

| Warranty | Product or workmanship evidence if address and scope match | Transfer status, coverage outcome, or later vendor work |

| Aerial imagery | Visible change between image dates | Exact installation date or membrane condition |

| PCA or inspection | Accessible condition at visit date | Hidden moisture, inaccessible roofs, or future useful life certainty |

| Leak log | Tenant-facing symptom chronology | Roof-wide condition without mapping and inspection |

Age should influence inspection and reserve planning, but it should not be treated as the whole roof. A well-maintained older roof with strong documentation may be more understandable than a newer roof with poor records, dense equipment, and recurring drainage issues. The confidence score is as important as the age band.

A roof file should map symptoms to locations

One of the biggest mistakes in commercial roof management is keeping roof information as loose text. "Leak in Suite 212" is useful only if someone can relate Suite 212 to roof zones, drains, equipment, and prior repairs. A stronger file maps symptoms to locations.

The minimum viable map is simple:

- Roof zones or sections.

- Drain and scupper locations.

- Major equipment and curbs.

- Known penetrations and access points.

- Repeated ponding areas.

- Prior repair locations.

- Interior symptoms by suite, room, bay, or gridline.

- Photo dates and viewpoints.

- Weather events and inspection dates.

This does not require a perfect BIM model. A marked-up aerial image, roof plan, or inspection sketch can be enough. The value comes from repeatability. If three unrelated people can locate the same roof area from the file, the file is working.

Location mapping turns vague patterns into specific decisions. If all symptoms point to one equipment curb, the next step may be a targeted repair and documentation. If symptoms appear across multiple roof zones after wind, the next step may be broader inspection. If ponding aligns with deck deflection and wet insulation, the planning problem changes from patching to assembly evaluation. If leak tickets cluster below a drain line, the roof may not be the only suspect.

For Asset Optimix, this is where prediction and workflow meet. A model can score the likelihood that a roof zone deserves attention, but the operator still needs a file that routes the next human action.

How different audiences should read the same roof evidence

The same roof file serves different decisions. That is why a good commercial roof intelligence surface should not be written only for roofers or only for underwriters. The evidence is shared, but the action changes.

| Audience | Primary question | Useful roof evidence | Bad shortcut |

|---|---|---|---|

| Commercial roofer | Which buildings deserve outreach or inspection? | Age band, weather exposure, equipment density, drain layout, visible distress, repair history | Treating weather exposure as proof of damage |

| Owner or asset manager | When should we inspect, repair, reserve, or replace? | Leak log, repair chronology, inspection photos, reserve schedule, tenant consequence | Waiting until leak tickets force action |

| Broker | What roof story will survive diligence? | Replacement records, warranties, recent inspections, known issues, capex plan | Hiding uncertainty until buyer inspection |

| Buyer or 1031 investor | What roof risk affects price, insurance, lending, and reserves? | PCA, roof consultant notes, age confidence, weather history, repair budget | Assuming a broad PCA answered roof-specific questions |

| Insurer or MGA | Is this risk maintained, vulnerable, or unknown? | Roof age confidence, maintenance evidence, hazard exposure, condition notes | Using a single roof age field as the whole view |

| Lender | What reserve or repair condition is reasonable? | Remaining useful life evidence, deferred maintenance, inspection quality, cost trend context | Treating replacement timing as a simple year count |

This table is not a substitute for professional review. It is a way to keep the conversation honest. A roofer should not write like an insurance adjuster. A broker should not turn a roof concern into a hidden disclosure problem. A lender should not pretend a roof reserve is exact. But all of them can use the same organized evidence.

The best early interventions are often documentation interventions

Not every high-risk signal means immediate replacement. Sometimes the highest-return intervention is documentation. This is especially true before a sale, refinance, insurance renewal, tenant expansion, or storm season.

Documentation interventions include:

- Ordering a roof inspection before marketing a property.

- Photographing each roof zone after a major storm and before the next repair.

- Collecting invoices, permits, warranties, and repair scopes into one folder.

- Mapping leak tickets to roof zones and repair dates.

- Asking mechanical vendors to document roof penetrations and service routes.

- Recording drain cleaning and debris removal.

- Getting a roofer to separate temporary repairs from recommended permanent work.

- Updating the reserve schedule after inspection instead of once per year by habit.

These moves do not replace physical work. They make physical work easier to prioritize. They also reduce friction between parties. A buyer who receives a clear roof file may still negotiate, but the negotiation is less likely to be driven by mystery. An underwriter may still ask for inspection, but the request is more targeted. A roofer may still recommend repair or replacement, but the recommendation can point to evidence rather than pressure.

Documentation also protects against false confidence. A file can reveal that the roof is less understood than expected. That is not failure. It is the start of better triage.

A practical roof failure signal hierarchy

Every building deserves its own review, but the following hierarchy is a useful starting point for commercial roof prediction and triage.

| Signal level | Examples | Typical action |

|---|---|---|

| Records gap | Unknown age, no warranty, missing invoices, vague PCA, inaccessible roof | Request records, schedule baseline inspection, assign low confidence |

| Maintenance signal | Clogged drains, debris, missing walk pads, minor open sealant, isolated patch | Clean, repair, document, monitor recurrence |

| Recurring location signal | Same suite leak, same drain area, repeated curb repairs, persistent ponding | Map location, inspect assembly, review repair strategy |

| Weather-vulnerability alignment | Severe hail/wind near older or vulnerable roof, edge concerns, known defects | Prioritize inspection and photo documentation |

| Consequence escalation | Critical tenant, inventory, electrical, refrigerated space, public facility, active leak | Accelerate professional review and mitigation |

| Systemic distress | Multiple zones, widespread wet insulation suspicion, major uplift, large membrane failure | Engage qualified roof consultant, engineer, insurer/lender as appropriate |

The key is not to let one signal dominate. A records gap can be manageable if the roof is recently inspected and maintained. A moderate defect can become urgent if the consequence is high. A weather event can be lower priority if the roof is newer, well documented, and inspected after the event. The system should support judgment, not replace it.

Which predictions matter first

The first useful prediction is not "replacement date." Replacement timing is important, but it is downstream of more basic questions:

- Which roofs deserve inspection priority?

- Which roof zones appear most vulnerable?

- Which buildings have weak roof evidence?

- Which properties need a roof record request before diligence?

- Which weather events should trigger post-event documentation?

- Which owners or roofers should intervene before a leak becomes a tenant problem?

- Which underwriting files need a confidence caveat?

That is a better first operating signal because it respects uncertainty. It also creates value for channel partners. Commercial roofers can use the signal to identify educational outreach and inspection opportunities. Owners can use it to plan. Insurers and lenders can use it to ask better questions. Brokers and buyers can use it to reduce surprise.

Over time, the system can add more specific outputs: roof age confidence, material vulnerability, drainage risk, hail and wind exposure history, repair chronology, replacement reserve recommendations, and intervention timing. Later it can expand into paving, drainage, exterior envelope, and municipal asset triage. The same principle applies: combine hazard, vulnerability, observed condition, records, consequence, and confidence.

Portfolio owners need trends, not only snapshots

Single-building roof decisions are hard enough. Portfolio decisions add another layer because the owner has to choose where attention goes first. A portfolio with twenty, two hundred, or two thousand commercial roofs cannot treat every roof concern as equal. The useful question becomes which roofs are moving toward expensive decisions faster than expected.

That requires trend evidence. A one-time inspection photo shows a condition on a date. A trend shows direction. Leak tickets rising in one region after a storm season tell a different story from stable leak tickets across older roofs. Repeated patching around the same equipment class may point to a vendor or design pattern. Drainage problems clustered across buildings of the same vintage may point to a capital program rather than isolated maintenance. Roofs with similar age can deserve different intervention timing because climate, tenant use, equipment density, and inspection history are different.

Portfolio roof intelligence should therefore rank roofs in several ways:

- Highest probability of near-term intervention.

- Highest consequence if the roof fails.

- Lowest evidence confidence.

- Highest weather-vulnerability alignment.

- Highest transaction or refinancing exposure.

- Highest likelihood that a modest maintenance action prevents a larger cost.

The last category is important. Owners do not only need to know which roof is worst. They need to know which action changes the trajectory. A roof with a moderate risk score and a clear drainage fix may be more actionable than a roof with a high risk score and no available access until a tenant window opens. Prediction becomes valuable when it routes scarce attention.

Claims-grade wording without claim conclusions

Commercial roof data often touches insurance without being an insurance claim. That creates a wording problem. Roofers, owners, brokers, and insurtech teams need precise language that does not overstate what the evidence proves. The safest language separates exposure, observation, and conclusion.

Exposure language says what was recorded nearby: hail, wind, rainfall, heat, freeze, or other weather context. Observation language says what was seen at the property: open seam, damaged flashing, ponding, interior stain, repair patch, displaced ballast, or tenant complaint. Conclusion language should be reserved for qualified reviewers who have enough property-specific evidence and authority for the decision being made.

That distinction is not legal decoration. It changes the workflow. If the file says "hail exposure near property, no post-event roof inspection located," the next action is inspection or record request. If it says "mapped impact damage observed on roof membrane and rooftop accessories after documented event," the next action may be repair scope, professional review, or insurance communication. Those are different levels of confidence.

Asset Optimix should make that separation obvious because it helps every audience stay in the correct lane. Roofers can sell inspection and maintenance without promising outcomes. Insurers can use exposure and vulnerability as triage features without treating them as damage proof. Brokers can disclose known information without inventing conclusions. Owners can plan intervention without pretending every storm creates an immediate capital event.

Boundaries that make the content more credible

Commercial roof content often loses credibility by overreaching. The topic touches roofing, engineering, insurance, code, warranties, lending, real estate transactions, tenant operations, and safety. No article or model should pretend to own all of that.

Good boundaries are simple:

- Do not advise untrained people to climb on roofs.

- Do not promise insurance coverage.

- Do not say weather data proves damage.

- Do not interpret warranty coverage without the warranty and facts.

- Do not turn a broad property condition assessment into a roof consultant report.

- Do not treat visible imagery as a hidden-moisture scan.

- Do not use a single roof age field as a condition report.

- Do not ignore tenant consequence when choosing the next action.

These boundaries are not defensive writing. They improve the product. A user who sees clear limits is more likely to trust the parts that are actually supported.

Bottom line

Commercial roof failure is rarely one thing. It is usually a chain that starts with ordinary evidence: water that lingers, a drain that clogs, a curb that moves, a patch that repeats, a service route that wears, an edge that loosens, a storm that exposes vulnerability, or a file that never recorded what happened.

The goal of Asset Optimix is to make that chain visible earlier. For commercial roofers, that means better outreach and better inspection priority. For owners and asset managers, it means fewer surprise roof decisions. For brokers and buyers, it means cleaner diligence. For insurers and lenders, it means physical underwriting that distinguishes maintained risk from unknown risk.

The best roof prediction does not pretend to see everything. It tells the user what is known, what is inferred, what is missing, what could be expensive, and what should happen next.

Frequently asked questions

Can a remote roof prediction replace a commercial roof inspection?

No. Remote prediction can triage risk, organize evidence, and prioritize inspection, but it does not replace qualified roof inspection, engineering review, code review, insurance advice, or emergency repair.

What is the earliest sign that a commercial roof is becoming expensive?

The earliest useful sign is often repeated evidence in the same area: standing water, recurring patching, tenant complaints, stained deck underside, damaged walk paths, or penetrations that keep needing attention.

Why do underwriters care about roof records?

Records turn vague roof age and condition statements into an evidence file. They help separate maintained risk from deferred maintenance and help show what remains uncertain.

Sources and limits

Research basis reviewed against NOAA/NCEI, NWS, WBDG, FEMA, EPA, IBHS, BLS, and Fannie Mae public guidance. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.