Wind risk

Wind Uplift, Perimeter Edge Conditions, and Rooftop Equipment Risk on Commercial Roofs

Commercial roof wind risk is not only a field-membrane question. This guide shows how roofers, owners, lenders, brokers, insurers, and asset managers should document edges, corners, parapets, openings, and rooftop equipment.

Key takeaways

- Wind risk often concentrates at corners, perimeter edges, parapets, coping, terminations, rooftop equipment, and openings rather than the roof field alone.

- A wind record near a building should trigger perimeter and equipment questions, but it does not prove property-specific roof damage by itself.

- Rooftop equipment history, vendor control, access paths, and curbs can change roof confidence even when the membrane age is well documented.

- A useful wind-risk file separates exposure, vulnerability, observed condition, consequence, confidence, and next action.

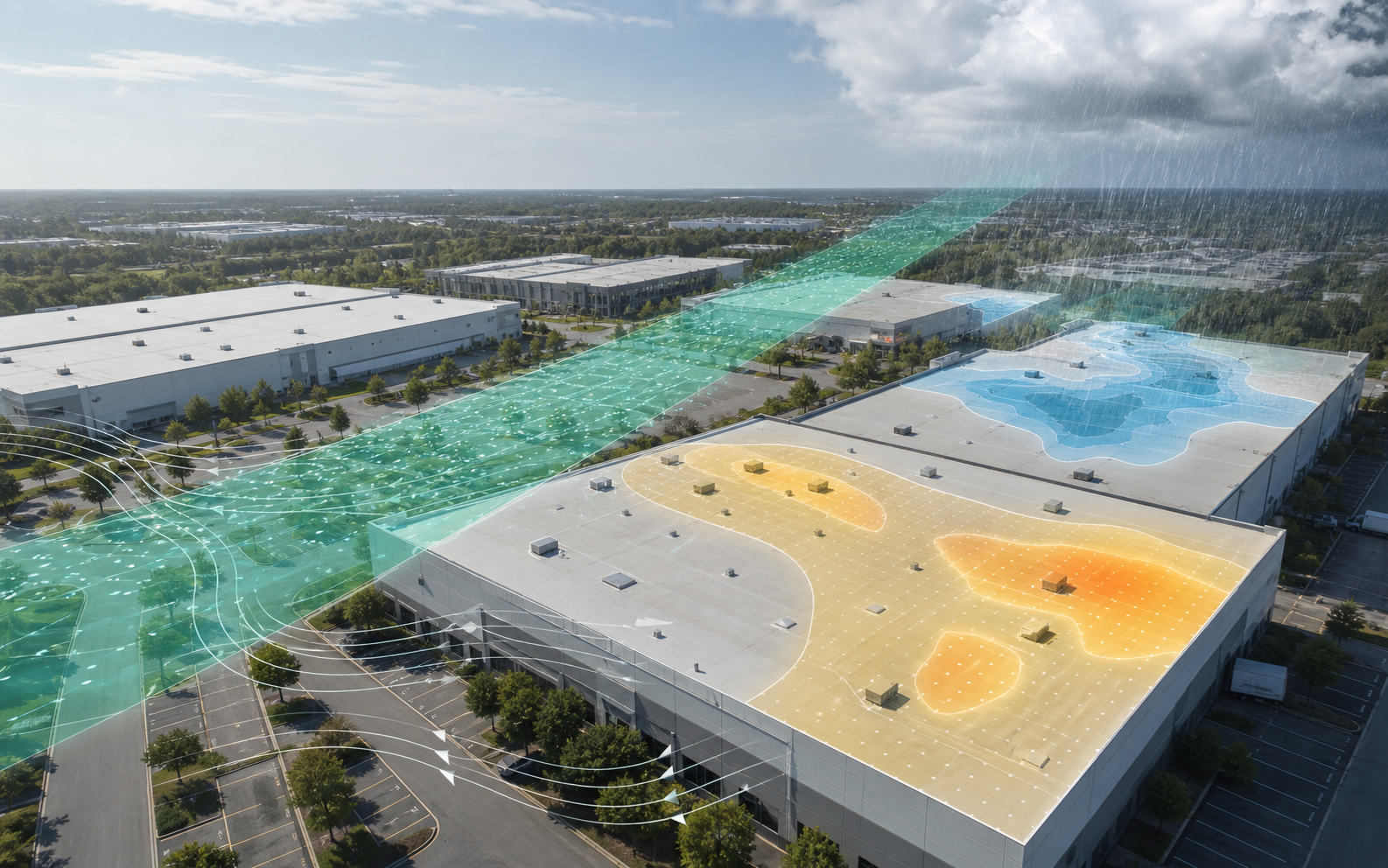

Wind roof risk often starts at the edge, not the middle

Commercial roof wind risk is easy to oversimplify. People often ask whether the roof "held up" after a wind event, as if the roof field were the whole story. In many commercial buildings, the most important wind evidence is not in the middle of the membrane. It is at the corners, edges, parapets, coping joints, flashing terminations, curbs, rooftop equipment, large openings, and transition details where pressure and attachment meet real construction.

That is why wind uplift belongs in physical underwriting. It connects the weather record to the roof assembly, the perimeter, the equipment platform, the openings, the inspection file, and the consequence of failure. A wind record near a building does not prove damage. It does create a reason to ask whether the vulnerable areas were documented before and after the event.

The practical question is not "Was it windy?" The practical question is: what roof areas could wind exploit, what evidence exists for those areas, and what decision changes because of the answer?

For Asset Optimix, this topic matters because commercial roof prediction should help roofers, owners, lenders, brokers, buyers, insurers, municipalities, and asset managers move from broad weather concern to specific evidence. Wind is not a generic roof hazard. It is a building-system hazard. The roof cover, edge metal, fasteners, deck, parapets, mechanical units, doors, vents, skylights, and openings can all affect what happens during a severe wind event.

Wind uplift is a building-system question

Wind uplift is not just wind pushing on a roof. Wind moving around a building creates pressure differences that can pull upward on roof components, stress perimeter conditions, and exploit weak attachment. Corners and edges often see higher localized effects than interior areas. Openings can change internal pressure. Rooftop equipment can move, vibrate, shed components, or stress curbs and penetrations. Loose edge metal or coping can become the first failure point.

That does not mean a business user should try to perform engineering calculations from a desk file. It means the desk file should point inspection and documentation toward the right areas.

A practical wind-risk file should separate:

- Wind exposure record.

- Roof age and system confidence.

- Perimeter and corner condition.

- Edge metal, coping, and flashing evidence.

- Rooftop equipment attachment and service history.

- Opening and door vulnerability.

- Prior repairs and maintenance.

- Post-event inspection evidence.

- Tenant or operational consequence.

This structure keeps the conversation grounded. A broker can avoid saying more than the file supports. A lender can understand whether reserve assumptions rely on stale roof evidence. A roofer can recommend a perimeter-focused inspection. An insurer can route follow-up based on vulnerability, not just wind speed. An owner can decide whether to refresh photos after a wind event.

Weather records should trigger questions, not conclusions

Public wind records are valuable. National Weather Service severe definitions, NOAA/NCEI storm records, local storm reports, and weather timelines can show that significant wind was reported near a property. Those records help identify date, event type, approximate location, and severity context.

But a wind record is not a roof inspection. It does not know whether edge metal was loose before the event. It does not know whether an HVAC contractor left a panel unsecured. It does not know whether a door failed and pressurized a warehouse. It does not know whether a parapet coping joint had been leaking for years. It does not know whether the roof cover was attached as designed.

The existing [hail exposure guide](/insights/commercial-roof-hail-exposure-damage-record/) makes the same distinction for hail. Exposure is context. Property-specific condition evidence is the bridge to roof-specific conclusions.

For wind, the same rule applies. A record of severe wind near a commercial building can justify inspection priority, photo updates, and record requests. It cannot by itself prove uplift damage, edge failure, equipment movement, or membrane detachment.

Good language sounds like this:

"Severe wind was reported near the property on the event date. The roof file has no post-event perimeter photos, and prior repair invoices mention edge metal. A perimeter and rooftop equipment inspection is recommended before reserve assumptions are finalized."

That is a decision note. It is not a technical verdict.

Perimeter and corner zones deserve their own evidence

Commercial roof files often include broad field photos and omit the perimeter. That is a problem. Edges and corners can be where the roof is most exposed and where small defects become large losses. A roof field that looks clean from the center can still have weak edge metal, open coping joints, deteriorated terminations, loose flashing, or prior repairs along the perimeter.

Perimeter documentation should include:

- Corners.

- Edge metal.

- Coping joints.

- Parapet walls.

- Termination bars.

- Counterflashing.

- Wall transitions.

- Gravel stops or fascia.

- Roof-to-wall interfaces.

- Perimeter drains and scuppers.

- Nearby rooftop equipment.

- Any prior repair locations.

The file should show both overview and detail. An overview photo helps locate the edge. A detail photo shows the condition. A repair invoice that says "edge repair" should be mapped to the actual roof area. If the same edge has repeated work orders, that repetition matters.

For roofers, perimeter evidence is a strong channel-partner wedge. A risk screen can identify buildings where the roof age is old, wind exposure is meaningful, and the perimeter file is weak. The next step is not an alarm. It is a disciplined inspection focused on the areas wind is most likely to exploit.

Edge metal is small, but it controls big outcomes

Edge metal, fascia, gravel stops, coping, and terminations may represent a small percentage of the roof area, but they can control the roof's behavior under wind. A loosened edge can allow wind to get under a roof cover. A missing or poorly attached section can expose the membrane edge. Failed coping can introduce water into parapet assemblies and weaken adjacent details. Corrosion or movement can turn an old maintenance issue into an event-driven failure.

An underwriting file should not treat edge metal as a cosmetic line item. It should ask:

- What type of edge condition exists?

- Are there parapets, coping, fascia, or gravel stops?

- Are fasteners visible, missing, backed out, or corroded?

- Are joints open or separated?

- Are there prior repairs or sealant-heavy patches?

- Is there staining below coping joints?

- Does the roof warranty or installation file mention edge details?

- Were edge areas photographed after high-wind exposure?

This does not require the business user to decide whether the edge system meets any standard. That is not the role of the file. The role of the file is to make weak or undocumented edge conditions visible enough that a qualified review can happen when the roof is material.

For buyers and lenders, edge evidence can change confidence. A building with an older roof but well-documented perimeter maintenance may be easier to underwrite than a newer roof with no edge photos and repeated wind exposure.

Parapets and coping connect roof risk to wall risk

Parapets can hide roof risk because they look like wall components from some vantage points. In reality, a parapet is part of the roof-edge system. Coping, cap flashing, counterflashing, termination points, wall membrane tie-ins, and drainage paths all matter.

A parapet problem can appear as:

- Open coping joints.

- Displaced coping.

- Cracked sealant.

- Loose counterflashing.

- Staining at interior wall lines.

- Moisture in parapet assemblies.

- Edge membrane movement.

- Repeated repairs at the same wall.

- Wind-driven rain entry near the roof-to-wall interface.

For physical underwriting, parapet evidence should be separated from the roof field. A roof field may be serviceable while a wall transition is weak. A PCA may mention roof condition but not show enough parapet detail. A broker may say the roof was replaced while the older parapet coping remained. A roofer may repair repeated leaks at a wall that never appear in the field membrane photos.

Wind can make these weaknesses more visible. It can stress coping, drive rain through openings, and exploit loosened terminations. The next action is not always replacement. It may be inspection, resealing, metal work, repair, monitoring, or a more detailed review. The point is to document the perimeter as a distinct risk area.

Rooftop equipment is part of the roof's wind profile

Commercial roofs carry equipment. HVAC units, exhaust fans, refrigeration units, hatches, screens, solar supports, telecom equipment, vents, ducts, pipe supports, and tenant-specific systems can all affect wind performance. Equipment adds penetrations, curbs, anchors, service traffic, condensate, repairs, and components that can move or detach.

Rooftop equipment risk has two sides:

- The equipment itself can be vulnerable to wind.

- The equipment can create roof vulnerabilities around curbs, supports, penetrations, service paths, and repairs.

The file should identify:

- What equipment exists.

- Who owns or maintains it.

- Whether it was present at roof installation.

- Whether equipment was added later.

- Whether curbs and penetrations were flashed by a roofer or another trade.

- Whether equipment service routes have walk pads.

- Whether panels, screens, hoods, or supports are secured.

- Whether repair invoices mention equipment areas.

- Whether photos show equipment after high-wind exposure.

This is especially important in industrial, retail, restaurant, cold-storage, medical, laboratory, and data-sensitive buildings. The roof is not only protecting space. It is carrying operational infrastructure. Wind damage to equipment can create water entry, business interruption, tenant disputes, or urgent repair needs even when the membrane field is not the primary issue.

Curbs and penetrations need a work history

Curbs and penetrations are common leak and wind-stress locations because they interrupt the roof field. They move differently. They are touched by more people. Mechanical vendors may remove panels, replace units, add lines, or change supports. A roof replacement may leave legacy penetrations. A tenant improvement may add new equipment after the roof warranty was issued.

A useful file should answer:

- Which curbs and penetrations existed at installation?

- Which were added later?

- Who performed the flashing work?

- Are there photos of completed details?

- Are there repair invoices at the same locations?

- Are pitch pans, pipe boots, or sealant-heavy details present?

- Are there signs of movement, cracking, open laps, or patched corners?

- Are service paths controlled?

Wind matters because it can move equipment, vibrate components, and stress weak details. Rain after wind can reveal failures at curbs and penetrations. The visible interior leak may appear after a storm, but the weak detail may have existed for years.

For roofers, a curb and penetration map is a practical advisory deliverable. It does not require overclaiming. It shows the owner where attention belongs and gives the next inspection a repeatable structure.

Openings and internal pressure change the roof conversation

Wind risk is not confined to the roof surface. Large doors, loading bays, roll-up doors, damaged windows, vents, and other openings can affect building pressure during a wind event. When an opening fails or is left unsecured, pressure inside the building can change and add stress to the roof system.

The roof file does not need to become a full building-envelope engineering study. It should, however, note opening-related vulnerabilities when they affect roof confidence.

Relevant evidence includes:

- Large loading doors.

- History of door or overhead-door damage.

- Broken windows or wall openings after a wind event.

- Vent or louver condition.

- Interior pressure-related observations after storms.

- Tenant operations that leave doors open.

- Wind-driven rain entry near openings.

- Roof damage that coincides with opening damage.

This matters for warehouses, industrial buildings, cold storage, hangars, municipal garages, and big-box retail. A roof may be judged unfairly if the file ignores building openings. Conversely, a roof may appear fine until a large opening changes the pressure conditions.

For insurers and lenders, opening evidence helps route the right review. For owners and asset managers, it can become a maintenance and operations issue, not just a roof issue.

Attachment history affects confidence

Commercial roof systems can be mechanically attached, adhered, ballasted, covered by pavers, recovered over existing assemblies, or installed in other system-specific ways. The business user does not need to calculate attachment. But the file should know what is documented and what is not.

Attachment-related evidence may include:

- Installation contract and specifications.

- Warranty and system documents.

- Fastener pattern or attachment notes.

- Deck type.

- Recover or tear-off scope.

- Prior uplift-related repairs.

- Ballast displacement history.

- Roof consultant observations.

- Manufacturer or contractor closeout documents.

- Photos during construction or repair.

If the roof has no installation records, the wind confidence level should be lower. If the roof was recovered, the file should not assume the hidden assembly behaves like a new full replacement. If a roof area has repeated edge repairs after wind, attachment or edge details may deserve review.

This is a confidence issue first. "Attachment undocumented" does not mean "roof will fail." It means the user should avoid pretending the system is understood.

Ballast, pavers, and loose materials create different questions

Some commercial roofs include ballast, pavers, walkway pads, loose equipment parts, temporary materials, or maintenance debris. Wind can move loose materials and create secondary damage. A ballasted or paver-covered roof may need different observation points than a smooth exposed membrane.

A file should ask:

- Is ballast present and evenly distributed?

- Are pavers used at walkways or equipment areas?

- Are pavers displaced or rocking?

- Are loose materials stored on the roof?

- Are screens, panels, or covers secured?

- Are temporary repairs or materials still on the roof?

- Are walkway pads attached and aligned?

- Are there signs of wind-scattered debris?

For underwriters, loose material evidence can change loss potential. For roofers, it is a maintenance opportunity. For owners, it may be a housekeeping and vendor-control issue. For buyers, it can signal whether the roof is actively managed or simply tolerated.

The goal is not to classify every roof system from an aerial image. The goal is to make sure inspection and photo requests cover the things wind can move.

Post-wind inspection should be perimeter-first

After a meaningful wind event, a roof inspection that only photographs the middle of the roof is incomplete. The post-wind photo set should begin with the areas wind is most likely to exploit.

A practical sequence:

- Exterior ground-level views of building sides and obvious damage.

- Corners and perimeter edges.

- Coping, parapets, fascia, and terminations.

- Roof-to-wall transitions.

- Rooftop equipment and curbs.

- Large openings and doors where relevant.

- Field membrane and seams.

- Drains, scuppers, and low areas.

- Prior repair locations.

- Interior leak or stain locations mapped back to roof areas.

Each photo should have a date and location note. A close-up without context is weak evidence. A broad roof view without detail can miss the issue. The best file shows where the condition is and why it matters.

For channel-partner roofers, this is a repeatable service workflow. It is not a promise that wind caused damage. It is a structured way to document current condition after an event.

Maintenance history can reveal wind vulnerability before the event

Wind failures often look sudden, but the record may show vulnerability before the storm. Maintenance history can reveal recurring edge repairs, loose coping, flashing reseals, repeated curb leaks, equipment panels coming loose, or service traffic that damaged details.

Useful keywords in invoices and work orders include:

- Edge metal.

- Coping.

- Counterflashing.

- Termination bar.

- Parapet.

- Curb.

- Pitch pan.

- Pipe boot.

- Roof hatch.

- HVAC curb.

- Wind damage.

- Loose panel.

- Reseal.

- Reset.

- Refasten.

- Replace flashing.

The pattern matters more than a single word. Three repairs at the same parapet over four years are different from one isolated reseal. A repeated equipment curb leak is different from a one-time puncture. A recurring edge repair after wind events should move that area into focused inspection.

For buyers and lenders, maintenance history helps distinguish known cost from uncertainty cost. For owners, it can justify preventive work before the next severe event. For roofers, it is a way to show value without exaggeration.

Underwriters should score confidence separately from severity

Wind-risk files should not collapse everything into one high, medium, or low label. Severity and confidence are different.

A roof may have high potential consequence but low confidence because records are missing. Another roof may have moderate vulnerability but high confidence because inspection and records are strong. A third may have known perimeter defects with high confidence, which is a different decision than a vague exposure record with no photos.

Useful dimensions:

| Dimension | Question |

|---|---|

| Exposure | Was severe wind reported near the property? |

| Vulnerability | Are edges, equipment, openings, or attachments likely weak or undocumented? |

| Condition | What was observed before and after the event? |

| Consequence | What happens if the roof opens or equipment fails? |

| Confidence | How strong are the records and photos? |

| Action | What should happen next? |

This structure is easier to defend than a single score. It also prevents overreaction. A strong exposure record with low vulnerability and current photos may not need the same action as a moderate wind event near an older roof with loose edge metal and no post-event inspection.

Brokers should prepare the wind file before marketing

When selling a commercial building, wind-related roof uncertainty can slow diligence. Buyers may ask whether a recent wind event affected the roof. Lenders may ask whether the PCA predates a storm. Insurers may ask about roof age, condition, and prior damage. The broker does not need to answer technical questions. The broker does need to organize the file.

Pre-listing wind diligence should include:

- Current roof photos covering edges and equipment.

- Known wind-event timeline since last inspection.

- Repair invoices tied to edge, coping, or equipment areas.

- Warranty and maintenance records.

- Roof age confidence by section.

- Tenant leak history after wind-driven rain.

- Notes on inaccessible areas.

- Any post-event inspection documents.

The offering package should not say "no wind damage" unless the evidence supports that statement and the limits are clear. Safer language names the source: "Seller provided post-event roof inspection photos dated..." or "No post-event roof inspection records provided."

This is not weaker. It is more professional. It reduces late disputes because the buyer sees the evidence boundary early.

Lenders should ask whether the roof file predates the wind event

Lenders may rely on a PCA, borrower records, photos, reserve schedule, and insurance evidence. If a severe wind event occurred after the roof observation, the roof file may be stale. The building may still be acceptable, but the confidence level should be updated.

Lender questions:

- Did severe wind occur after the most recent roof observation?

- Were perimeter and rooftop equipment areas photographed?

- Did the PCA include roof access limitations?

- Were repairs completed after the event?

- Is the reserve estimate tied to pre-event condition?

- Does the borrower have maintenance records?

- Are tenant complaints or leaks documented?

- Are high-consequence operations under vulnerable roof areas?

For bridge and hard-money lenders, speed makes this more important. A roof condition can be acceptable if it is known and priced. It can become a closing problem if it appears late and has no scope. Wind-risk confidence helps decide whether to request inspection, adjust reserve, or proceed with a documented caveat.

Owners and asset managers need a wind-event routine

Owners should not rebuild the roof file from scratch after every storm. The stronger approach is to create a routine.

A practical wind-event routine:

- Identify meaningful wind exposure near the property.

- Check whether the last roof photos predate the event.

- Review leak logs and tenant complaints.

- Inspect or photograph perimeter edges, corners, equipment, and openings.

- Note any loose or displaced materials.

- Record any emergency work.

- Map findings to roof areas.

- Update reserve or maintenance triggers if confidence changes.

This routine can be scaled across portfolios. The owner does not need every roof inspected at the same level after every wind event. The owner needs a way to prioritize buildings where exposure, vulnerability, consequence, and low confidence overlap.

For municipalities and public owners, this can support defensible triage. A building that houses emergency operations, has older roof age, and lacks post-event perimeter photos may move ahead of a storage building with a newer documented roof and current inspection.

Roofer channel partners can lead with perimeter education

Wind risk gives commercial roofers a useful advisory angle. Many owners understand leaks and replacement age. Fewer understand why perimeter edges, coping, equipment, and openings should be part of a post-wind inspection.

A roofer can educate without overclaiming:

- "Your roof field photos are current, but we do not see perimeter documentation after the wind event."

- "The repair history mentions edge metal twice. That area should be inspected before renewal."

- "The equipment curbs were added after the roof was installed. We should confirm flashing condition."

- "A post-wind photo set would improve your file even if no repairs are needed."

This kind of conversation supports trust. It does not promise damage, replacement, coverage, or an outcome. It creates a professional reason for inspection, maintenance, or documentation.

For Asset Optimix, this is exactly where prediction can support a channel strategy. The system can identify buildings where a roofer's expertise is likely to be useful before a crisis.

Insurers need to separate edge vulnerability from roof age

Insurance teams often receive roof age as a key field. Wind risk shows why age is not enough. A newer roof with poorly documented edge conditions and dense equipment can be a different risk than an older roof with well-maintained perimeter details and current photos.

Useful insurer-facing fields include:

- Roof age confidence.

- Perimeter condition confidence.

- Equipment density and attachment confidence.

- Opening vulnerability.

- Last wind-event review date.

- Prior edge or equipment repairs.

- Tenant consequence.

- Inspection recency.

This can improve routing. A policy file that says "2018 roof" may still deserve attention if edge evidence is missing after a wind event. A file that says "2009 roof" may be more understandable if inspection, maintenance, and perimeter records are strong.

The goal is better physical underwriting, not automatic rejection or automatic acceptance.

A wind-risk evidence matrix

A simple evidence matrix can keep teams aligned.

| Evidence area | Strong file | Weak file | Likely next action |

|---|---|---|---|

| Wind exposure | Event date, source, and location context recorded | Vague memory of high wind | Build event timeline |

| Perimeter | Dated photos of corners, edges, coping, and terminations | Field photos only | Perimeter inspection |

| Equipment | Equipment map and curb photos | Unknown equipment history | Equipment-focused roof review |

| Openings | Doors and openings reviewed after event | No building-envelope notes | Ask operations or maintenance team |

| Repairs | Invoices mapped to roof areas | Generic repair totals | Request detail or roofer notes |

| Consequence | Tenant and operation impact known | No consequence ranking | Rank building priority |

| Confidence | Limits and access noted | Broad roof condition statement | Add caveats and gather evidence |

The matrix should not decide technical issues. It should show where the file is strong, weak, or stale.

Transaction diligence should separate old wind history from current risk

Commercial property transactions often contain scattered weather references. A seller may mention that the property went through a wind event with no known issues. A buyer may see prior roof repairs in the ledger. A lender may receive a PCA that predates the most recent storm season. An insurance broker may ask for roof age and loss history. These facts can sit in different folders and never become one roof-risk view.

A transaction file should separate three things:

- Historical exposure: wind events that occurred near the building.

- Historical response: inspections, repairs, photos, or maintenance after those events.

- Current posture: what the roof file supports today.

The distinction matters. A 2021 wind event followed by documented perimeter repairs and current photos may be less concerning than a 2025 event with no inspection record. A building with old wind exposure and strong follow-up can be more transparent than a building with fewer records but no clear event timeline. The goal is not to punish buildings for having weather. The goal is to understand whether the owner kept the roof evidence current.

For buyers, this helps diligence stay focused. The buyer can ask for post-event inspection records instead of arguing abstractly about a storm. For sellers, it creates a way to show responsible ownership. For lenders, it clarifies whether reserves rely on current evidence or stale assumptions.

Lease and tenant operations can change wind consequence

The same roof condition can have different consequences depending on the tenant and use. A loose edge over a vacant storage bay is not the same business risk as a loose edge over a food-processing line, medical space, data room, cold-storage area, public-safety function, or high-value inventory. Wind risk should account for what sits below the vulnerable area.

Tenant and operations questions include:

- Which roof areas cover mission-critical operations?

- Are tenants responsible for any rooftop equipment?

- Do tenant vendors access the roof?

- Are large doors frequently open during operations?

- Would water entry shut down a production line?

- Would equipment displacement create immediate safety or operations issues?

- Are lease provisions clear about maintenance access and notification?

- Are tenant complaints mapped to roof areas?

This is not a legal review of the lease. It is a consequence review. The roof file should show when a vulnerable edge or equipment cluster sits above a high-consequence space. That building may deserve inspection sooner than a similar roof over low-consequence storage.

For brokers and asset managers, this can help explain why two roofs of similar age receive different attention. The roof with greater tenant consequence may be the higher priority even if the visible condition looks similar.

Vendor control is a roof-risk control

Rooftop equipment risk is partly a vendor-control problem. Mechanical, electrical, telecom, solar, refrigeration, signage, and tenant vendors may access the roof without the same roof-system knowledge as a commercial roofer. They may move panels, drag tools, add penetrations, reroute lines, remove fasteners, or leave temporary materials. Wind can then exploit conditions created by routine work.

Owner controls can include:

- Roof access logs.

- Required walk paths.

- Vendor rules for temporary materials.

- Photo documentation before and after equipment work.

- Roofer review when curbs or penetrations change.

- Closeout package for new rooftop equipment.

- Maintenance checks after major service events.

- Clear responsibility for tenant-owned equipment.

These controls are practical. They do not require a new software platform or a complicated policy. They require the owner to treat the roof as an operating surface, not empty space above the building.

For roofers, vendor control creates a recurring advisory service. A roofer can help the owner document equipment areas, inspect after major mechanical work, and identify where service traffic is creating wear. For underwriters, vendor control can improve confidence because the file shows that rooftop changes are managed.

Solar and newer rooftop systems deserve separate notes

More commercial roofs now carry solar arrays, screens, telecom equipment, security hardware, and other rooftop systems. These systems can change access paths, ballast or attachment questions, drainage behavior, and maintenance responsibilities. They can also make post-wind inspection harder because parts of the roof are covered or obstructed.

The roof file should identify:

- Whether solar or other rooftop systems are present.

- Whether they are ballasted, attached, or otherwise supported.

- Whether the roof warranty was reviewed when they were installed.

- Whether roof access under or around the system is possible.

- Whether drainage paths changed.

- Whether service routes are clear.

- Whether wind exposure creates inspection triggers for the system.

- Who owns and maintains the system.

This article does not tell the owner how to design or approve rooftop systems. It simply names the evidence that underwriting, acquisition, and maintenance teams need. A roof with solar may be a well-managed asset. It may also have hidden access and attachment uncertainties. The difference is the file.

For buyers, this matters before closing. A rooftop system can affect diligence, tenant operations, roof maintenance, warranty review, reserve planning, and insurance questions. It should not be discovered late as a few panels in an aerial photo.

Portfolio triage should combine event, vulnerability, and consequence

After a significant wind event, a large owner should not inspect every roof in the same order. The triage list should combine event strength, roof vulnerability, evidence confidence, and consequence.

A practical ranking might prioritize:

- Buildings near severe wind reports with no post-event roof photos.

- Older roofs with low age confidence and known edge repairs.

- Buildings with dense rooftop equipment over critical operations.

- Buildings with large doors or openings and prior wind-driven rain complaints.

- Roofs with known loose coping, fascia, or parapet repairs.

- Properties in sale, refinance, renewal, or major lease negotiation.

- Buildings with tenants reporting new leaks after the event.

The order will vary by portfolio, but the logic should be visible. A building moves up because several risk signals overlap, not because one map color looks concerning. This makes the triage defensible for owners, municipalities, lenders, and insurance teams.

It also gives commercial roofers a better outreach list. Instead of calling every property in a wind swath, a roofer can focus on buildings where the roof file already indicates a practical need for inspection or documentation.

Cost planning should include access and staging

Wind-related roof work can be more expensive than the visible defect suggests because access and staging matter. Replacing or repairing edge metal on a multi-story building may require lifts, safety planning, tenant coordination, traffic control, or after-hours work. Rooftop equipment work may require mechanical coordination. Parapet and coping repairs may involve wall conditions. Interior leaks may require tenant protection.

A reserve note should therefore separate:

- Visible roof condition.

- Likely repair area.

- Access complexity.

- Tenant consequence.

- Equipment coordination.

- Temporary protection needs.

- Urgency after exposure.

- Confidence in scope.

This keeps a buyer, lender, or owner from treating a perimeter issue as a simple material line item. A small edge condition in the wrong location can create a larger operational problem. A well-documented repair plan can make the same issue manageable.

The [commercial roof capex guide](/insights/commercial-roof-capex-reserve-planning/) uses the same principle: known cost, likely cost, and uncertainty cost should be separated. Wind risk often adds uncertainty cost when access, edge scope, or equipment history is unclear.

When to escalate

Escalation does not always mean emergency. It means the current file is not enough for the decision being made.

Escalate when:

- Edge metal appears loose, missing, displaced, corroded, or repeatedly repaired.

- Coping or parapet details are open or moving.

- Rooftop equipment appears shifted, unsecured, or surrounded by new distress.

- Wind-driven rain created leaks near transitions.

- Large openings were damaged during the event.

- The roof is high consequence and post-event evidence is missing.

- A sale, refinance, renewal, or reserve decision depends on roof condition.

- The PCA predates a meaningful wind event.

- Roof access was limited.

- Records conflict about prior repairs.

Escalation may mean a commercial roofer inspection, roof consultant review, maintenance repair, photo update, or owner decision meeting. The correct path depends on the building, the decision, and the evidence.

Limits keep the file credible

A wind-risk file should be explicit about what it does not do. It should not certify code compliance, calculate wind pressures, interpret insurance coverage, determine warranty rights, or replace engineering review. It should not say a roof is safe or unsafe based only on a weather record. It should not treat a lack of leaks as proof that no vulnerability exists.

Good limits sound like this:

"This review identifies exposure context, roof evidence gaps, and inspection priorities. It does not replace qualified roof inspection, engineering review, code review, warranty interpretation, insurance coverage review, or emergency response."

Clear limits make the output more useful. They tell the user what decision the file can support and what decision needs another professional.

Bottom line

Wind uplift risk is not only a roof-field question. It lives at corners, edges, parapets, coping, terminations, rooftop equipment, curbs, openings, attachment records, and maintenance history. A severe wind record can raise the right questions, but the roof file needs property-specific evidence before drawing property-specific conclusions.

The commercial value is practical. Roofers get a stronger advisory workflow. Owners and asset managers get better event routines. Brokers reduce late diligence friction. Buyers and lenders understand whether reserve decisions rest on current evidence. Insurers can separate age, vulnerability, condition, consequence, and confidence.

That is how wind becomes part of physical underwriting instead of another vague weather label.

Frequently asked questions

Does a severe wind report prove roof uplift damage?

No. A severe wind report can justify inspection priority, but roof-specific conclusions need property-specific evidence such as perimeter photos, equipment observations, repair history, and qualified review.

Why are perimeter edges important in commercial roof wind risk?

Edges, corners, coping, parapets, and terminations can be vulnerable areas where wind can exploit loosened or poorly documented details. A roof field can look stable while perimeter evidence is weak.

What should a post-wind commercial roof inspection document?

A useful post-wind file should document corners, edge metal, coping, parapets, terminations, rooftop equipment, curbs, openings, field membrane, drains, prior repairs, access limits, and interior leak locations when present.

Sources and limits

Research basis reviewed against WBDG roofing-system guidance, FEMA low-slope roof mitigation guidance, IBHS commercial wind vulnerability research, NWS severe wind definitions, NOAA/NCEI storm records, ASTM PCA framing, and Fannie Mae PCA guidance. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence, observed condition, and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, useful life, and repair needs.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings, including low-slope roof drainage principles.