Acquisition diligence

Commercial Roof Records Before a 1031 Exchange Acquisition: What Buyers, Brokers, Lenders, and Roofers Need to Know

A 1031 exchange buyer does not have much room for late roof uncertainty. This guide explains how roof records, weather exposure, PCA scope, leak history, warranties, and reserve confidence should shape the replacement-property decision.

Key takeaways

- A 1031 exchange timeline makes roof uncertainty more expensive because late diligence issues can affect price, debt, insurance, reserves, and closing certainty.

- Roof evidence should be organized by section, confidence, known cost, uncertainty cost, weather exposure, leak mapping, warranty status, and tenant consequence.

- A PCA is a starting point for roof diligence, not a substitute for roof-specific inspection when the roof is financially material.

- Commercial roofers can become valuable acquisition partners by documenting roof condition and intervention timing without stepping into tax, legal, lending, or insurance advice.

Roof uncertainty is expensive inside a compressed acquisition window

A 1031 exchange buyer does not have the luxury of slow uncertainty. The exchange may be driven by tax timing, replacement-property availability, debt markets, seller deadlines, tenant stability, and a limited diligence period. The buyer may be moving from one asset class to another, trading into a larger building, diversifying across markets, or trying to preserve equity for the next investment. In that setting, a commercial roof problem is not just a maintenance issue. It can become a price issue, a reserve issue, a lending issue, an insurance issue, and a closing-certainty issue at the same time.

The roof is unusually good at creating late surprises because it touches multiple diligence streams. A property condition assessment may mention remaining useful life. A seller may provide a warranty. A broker may say the roof was replaced. A lender may require a reserve. An insurer may ask about age or condition. A roofer may identify ponding, edge, flashing, or membrane concerns. A tenant may have a history of leak complaints. Those facts often arrive in different folders, from different people, and at different levels of confidence.

Asset Optimix treats the 1031 roof file as a decision asset. The buyer does not need every possible roof fact before making an offer. The buyer does need to know which roof facts are strong enough to price, which are weak enough to reserve against, and which require professional inspection before the exchange timeline runs out.

This article is not tax, legal, insurance, engineering, or lending advice. A 1031 exchange should be structured with qualified tax and legal professionals. The roof question is narrower: how should a commercial real estate buyer, broker, lender, roofer, or owner organize roof evidence so physical uncertainty does not become a late acquisition surprise?

The 1031 clock makes roof diligence a sequencing problem

The IRS describes like-kind exchanges as exchanges of real property held for business or investment for other business or investment real property of like kind. The tax rules, identification deadlines, qualified intermediary structure, and exchange mechanics are outside the scope of a roof-intelligence article. But the roof impact is practical: the buyer may have less room to pause, renegotiate, or start over if physical diligence creates a late problem.

That pressure changes the roof workflow. In an ordinary acquisition, a buyer might discover roof uncertainty, extend diligence, bring in a specialist, ask for additional records, negotiate a credit, or move on. In an exchange-driven acquisition, the buyer may still do those things, but the timing can be tighter and the cost of delay can be higher. A roof issue that would be manageable on day five can become a deal problem on day thirty-five.

The practical sequence should be:

- Ask for the roof file before the property looks like the winning replacement candidate.

- Separate roof records by strength, not by folder name.

- Map roof evidence to roof areas, tenant areas, and business consequence.

- Identify what a PCA can answer and what it cannot.

- Decide early whether a roof specialist, roofer, moisture survey, or engineering review is justified.

- Translate uncertainty into price, reserve, inspection condition, or walk-away logic.

- Preserve source limits so nobody mistakes weather exposure, age statements, or broad observations for a roof-specific conclusion.

This sequence helps the buyer avoid two bad outcomes: overreacting to a roof that is manageable, or accepting a roof that is under-documented because the exchange deadline is uncomfortable.

The roof file should be requested before the buyer falls in love with the deal

Many buyers wait too long to ask for roof evidence. They tour the property, underwrite rent, review leases, think about financing, and only then push for roof details. By that time the buyer may already have emotional and transaction momentum. Roof uncertainty becomes harder to evaluate neutrally.

The stronger move is to ask early for a roof file, even if the first file is incomplete. The first request should not sound like a fight. It should sound like a normal physical diligence request for a capital component.

Useful early request:

- Roof installation date by section.

- Replacement, recover, coating, restoration, or repair scopes.

- Permits where available.

- Current warranties and transfer requirements.

- Roof inspection reports.

- Property condition assessment excerpts and roof photos.

- Leak logs and tenant work orders.

- Repair invoices from the last five years.

- Drain cleaning and maintenance records.

- Rooftop equipment work that affected penetrations, curbs, or access paths.

- Recent severe-weather history and any post-event inspections.

- Known open roof issues and bids.

If the seller cannot provide much, that is not an automatic deal killer. It is a confidence signal. A roof with weak records may still be serviceable, but the buyer should not underwrite it as though the records are strong. Weak records can justify earlier inspection, a larger uncertainty reserve, a lender discussion, or a more cautious price.

For brokers, this is also a listing-preparation issue. A seller who wants to attract exchange buyers should not wait for the buyer to ask. A ready roof file can reduce friction, especially when the building is older, low-slope, heavily penetrated, recently storm-exposed, or important to tenant operations.

Roof age is not one fact when the building has multiple roof areas

Commercial buyers often ask, "How old is the roof?" The answer may be misleading if the building has multiple roof sections. One section may have been replaced, another recovered, another patched, and another coated. Additions, tenant improvements, rooftop equipment changes, and partial storm repairs can create a roof history that does not fit one date.

For acquisition diligence, roof age should be organized by roof area:

| Roof evidence | Buyer use | Common problem |

|---|---|---|

| Full replacement invoice | Strong age and scope evidence if address and roof area are clear | May not cover all roof sections |

| Recover or overlay record | Useful capital history | May hide older assembly risks or warranty limits |

| Coating/restoration invoice | Useful maintenance and life-extension evidence | Should not be treated as full replacement without support |

| Permit record | Date and jurisdiction trail | Scope may be vague or incomplete |

| Warranty | Material/workmanship context | Transfer, exclusions, and later penetrations need review |

| Seller statement | Useful lead | Needs corroborating records |

| Aerial imagery change | Timeline clue | Does not prove assembly, condition, or exact date |

The buyer should avoid converting all of that into a single average roof age. A weighted average can hide the part of the roof that creates the next capital event. If 80 percent of the roof is newer and 20 percent sits over a critical tenant with poor drainage and unknown age, the smaller section may drive the reserve.

Roof age also needs confidence. "Roof believed to be 10 years old" is not the same as "Roof section A replaced in 2016 by invoice and warranty; roof section B coating installed in 2021; roof section C age unknown." The second statement is longer, but it is more useful.

A PCA is a starting point, not the whole roof answer

Property condition assessments are important in commercial real estate diligence. ASTM's E2018 guide is widely cited for baseline property condition assessment work in acquisitions, financing, investments, and capital expenditure planning. Fannie Mae's multifamily PCA guidance emphasizes physical condition, deferred maintenance, current and future needs, useful life, photos, component ratings, and replacement reserves. Those are exactly the categories buyers and lenders care about.

The limitation is that a PCA is often broad. The assessor may have limited roof access, limited time, weather constraints, safety constraints, or limited records. A PCA may identify apparent condition and reserve items without performing roof-consultant-level diagnostics. It may not include moisture survey, core cuts, manufacturer review, warranty analysis, or full roof-zone mapping.

That does not make the PCA weak. It means the buyer should read it with scope awareness.

Questions to ask while reading the PCA roof section:

- Did the assessor access the roof directly?

- Were all roof areas observed?

- Are photos sufficient to understand drains, edges, penetrations, equipment, and repairs?

- Does the report separate roof sections?

- Does the remaining useful life estimate explain its basis?

- Are immediate repairs separated from replacement reserves?

- Are roof access limits clearly stated?

- Are leak history and tenant complaints included?

- Are warranties or repair records reviewed?

- Are weather events after the PCA date relevant?

If the PCA roof section is thin and the roof is financially material, the buyer should decide early whether supplemental roof diligence is needed. The supplemental review may be a commercial roofer inspection, roof consultant review, moisture survey, targeted photo request, warranty review, or engineering input depending on the building.

The replacement reserve should separate known cost from uncertainty cost

Exchange buyers often need quick reserve thinking. The danger is turning incomplete roof evidence into an overconfident number. A better acquisition reserve separates known cost, likely cost, and uncertainty cost.

Known cost is supported by specific evidence. Examples include a repair bid for flashing, a PCA immediate repair item, a drain correction, a documented warranty transfer fee, or a known maintenance issue. Likely cost is supported by condition patterns but still needs scope confirmation. Examples include recurring ponding that may require tapered insulation work, repeated repairs around rooftop units, or an older roof section approaching planned replacement. Uncertainty cost is the premium for missing or weak evidence: unknown age, no access, no leak log, missing warranty, conflicting seller statements, or no post-storm inspection.

The distinction matters because known and uncertain costs are negotiated differently. A buyer can ask the seller to complete a known repair. A buyer can price a likely capital item. A buyer can demand more inspection access when uncertainty is too large. If all three categories are merged into one number, the conversation becomes less precise and more adversarial.

Example reserve framing:

| Evidence state | Reserve posture |

|---|---|

| Recent roof replacement, strong records, no leak history | Low near-term reserve, maintain documentation |

| Older roof, good inspection report, manageable defects | Maintenance and medium-term reserve |

| Multiple roof areas, partial records, no recent inspection | Baseline inspection and uncertainty reserve |

| Recurring leaks below same roof zone | Targeted investigation and repair/replacement scenario |

| Severe weather after last inspection | Post-event inspection trigger before final reserve |

| Unknown age, weak records, high tenant consequence | Larger uncertainty reserve or deal condition |

For lenders, this structure is easier to understand than a vague roof allowance. For brokers, it gives the deal team a way to explain why a roof concern is real, manageable, or still unresolved. For roofers, it creates a path from inspection to scope rather than jumping straight to replacement.

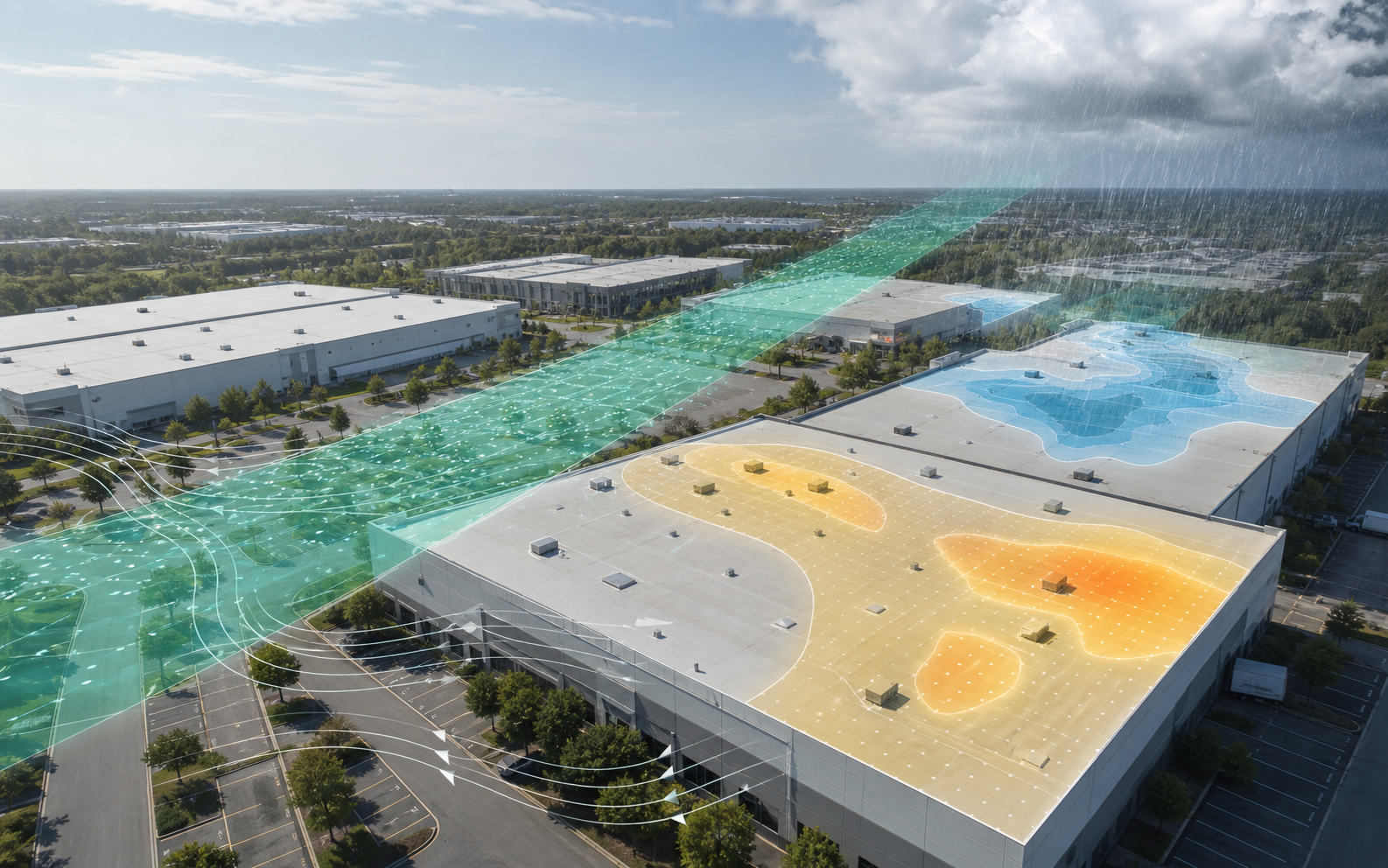

Weather history should change inspection priority, not create a damage conclusion

Weather is especially sensitive in acquisition diligence. A buyer may discover hail or wind history near the property and worry that the roof has hidden damage. A seller may dismiss the concern because no claim was filed. A roofer may see an inspection opportunity. An insurer may care about age and condition. All of those reactions can be reasonable, but they need evidence boundaries.

The NOAA/NCEI Storm Events Database can help establish significant weather events by date, geography, and event type. The National Weather Service severe weather definitions help explain why hail of at least one inch or wind of at least 58 mph is operationally relevant. But those records are exposure context, not property-specific roof damage proof.

For a 1031 buyer, the useful question is not "Did a storm happen somewhere nearby?" The useful question is: "Does the weather timeline change what we need to verify before closing?"

Weather should trigger follow-up when it aligns with vulnerability:

- Older roof with severe hail or wind exposure after the last inspection.

- Low-slope roof with known edge repairs after a high-wind event.

- Roof with skylights, rooftop equipment, solar, or soft-metal accessories after hail.

- Recurring leak tickets after heavy rainfall.

- No post-event inspection despite significant weather exposure.

- High-consequence tenant areas below vulnerable roof zones.

The buyer should ask for dated post-event photos, inspection notes, repair invoices, and tenant complaint chronology. If those do not exist, the file should say so. "Unverified after severe weather" is more honest than either "storm damage" or "no issue."

This language also protects brokers and roofers. The right position is not to weaponize weather history. It is to use weather history to decide whether inspection, documentation, or reserve adjustment is warranted.

Rooftop equipment can change the deal more than the membrane age

In many commercial buildings, rooftop equipment is the roof's most active risk zone. HVAC units, exhaust fans, refrigeration equipment, telecom hardware, conduit, solar equipment, grease ducts, and tenant improvements add penetrations, service traffic, supports, discharge, and vendor work. A roof can have a respectable age and still be vulnerable because the equipment history is messy.

Acquisition diligence should ask:

- What rooftop equipment exists and who owns or maintains it?

- Which equipment was added after the last roof replacement?

- Were new curbs, penetrations, or supports installed?

- Are service routes protected by walk pads?

- Are condensate or discharge lines managed correctly?

- Are grease or chemical exposures present?

- Do repair invoices cluster around equipment?

- Do tenant work orders point below equipment zones?

- Did warranties require approval for later penetrations?

This is a major issue for buyers moving into larger commercial assets through an exchange. The buyer may be comfortable with residential or smaller commercial maintenance, then acquire a building where the roof is also a mechanical platform. The financial risk is not only roof age; it is control over everyone who touches the roof.

For commercial roofers, equipment density is a strong advisory signal. A building with many rooftop units and weak records deserves a different maintenance conversation than a simple low-slope roof with limited equipment. For lenders and insurers, equipment density can help explain why two roofs of the same age should not be treated the same.

Leak logs should be mapped before they are summarized

Seller-provided leak history can be useful, but summaries hide patterns. "Three leaks repaired over the last two years" means little without location. Three unrelated minor leaks across a large building may be manageable. Three leaks below the same drain, parapet, or equipment curb may point to a persistent roof-zone problem.

The buyer should map leak logs to:

- Suite, bay, room, or gridline.

- Roof zone above the symptom.

- Drain, scupper, parapet, equipment, or penetration nearby.

- Date of complaint.

- Weather near the complaint date.

- Repair invoice and scope.

- Whether the complaint recurred.

- Whether interior damage was repaired.

The goal is not to prove the roof caused every water symptom. Interior water can come from plumbing, facade, condensation, mechanical systems, or roof defects. The goal is to see whether a roof-zone pattern exists.

Mapped leak history changes the acquisition conversation. A seller may say "all leaks were repaired." The buyer can ask, "Did they recur below the same roof zone?" A lender may ask whether immediate repairs are enough. A roofer may identify where inspection should start. An insurer may ask whether maintenance is documented. Everyone gets a sharper question.

Warranties are diligence leads, not comfort by themselves

A roof warranty can be valuable. It can also create false comfort. Buyers should read warranties as leads for further review, not as automatic protection. The warranty may have transfer requirements, exclusions, maintenance obligations, notice rules, approved-contractor requirements, limitations for later penetrations, exclusions for ponding, exclusions for acts of nature, or differences between material and workmanship coverage.

The acquisition team should ask:

- Is the warranty transferable?

- Has transfer notice or fee been handled?

- Which roof sections are covered?

- What is the warranty type and remaining term?

- Are later rooftop penetrations or equipment changes approved?

- Are inspection and maintenance obligations documented?

- Are leaks, repairs, or claims already reported?

- Are ponding, wind, hail, or consequential damages limited or excluded?

- Does the warranty match the seller's roof-age statement?

This is not a warranty interpretation. It is a diligence posture. Legal and roofing professionals should review the actual warranty. The buyer's job is to make sure the warranty is not treated as a vague substitute for condition evidence.

Brokers can reduce friction by collecting warranty documents before marketing. Owners can protect value by keeping warranty transfer and maintenance records organized. Roofers can help owners understand what maintenance documentation supports warranty credibility without giving legal advice.

The buyer should identify roof deal-breakers before the inspection comes back

Roof diligence is easier when the buyer knows what would actually change the deal. Without that discipline, every roof issue becomes emotional. A disciplined buyer identifies roof deal-breakers, price-adjustment triggers, reserve triggers, and monitoring items in advance.

Possible deal-breakers:

- Active roof failure over critical tenant operations with no feasible mitigation.

- Major unknown roof condition where access is denied.

- Material capital need that breaks financing or exchange economics.

- Insurance placement concern that cannot be resolved before closing.

- Seller refuses reasonable roof records or inspection access.

- Roof condition conflicts materially with seller representation.

Possible price or reserve triggers:

- Unknown age for a large roof section.

- PCA recommends near-term replacement.

- Recurring leak pattern in a mapped zone.

- Severe weather exposure after last inspection without verification.

- Warranty transfer uncertainty.

- Roof specialist identifies wet insulation or systemic drainage issues.

Possible monitoring items:

- Minor isolated defects with clear repair plan.

- Older roof with good records and low consequence.

- Weather exposure but no symptoms and post-event inspection.

- Maintenance items that seller can complete before closing.

This structure helps an exchange buyer move quickly without being reckless. It also helps brokers and sellers understand what kind of roof issue matters. Not every defect deserves a re-trade. Not every uncertainty should be ignored.

Lenders and insurers should see the same roof evidence the buyer sees

Roof surprises become worse when the lender or insurer sees different evidence than the buyer. A buyer may underwrite a manageable roof reserve, then the lender's review identifies deferred maintenance. Or the buyer may assume insurance will be routine, then underwriting asks for roof age, condition, or inspection documentation. These issues can threaten timing even when the roof itself is not catastrophic.

The buyer should prepare a roof evidence package that can support lender and insurance conversations:

- Roof section summary.

- Age evidence and confidence.

- PCA roof excerpts.

- Inspection photos.

- Repair history.

- Leak history summary with mapped locations.

- Warranty status.

- Known immediate repairs.

- Replacement reserve logic.

- Weather exposure since last inspection.

- Open uncertainties and planned follow-up.

This package is not a sales brochure. It should include limits. If roof age is unknown, say so. If weather exposure is unverified by inspection, say so. If access was limited, say so. Lenders and insurers can work with uncertainty more effectively when it is named early.

For hard-money and bridge lenders, speed makes this even more relevant. A roof issue can be acceptable if it is priced, reserved, and tied to a repair plan. The same issue can be unacceptable if it appears late with no scope, no access, and no confidence.

Brokers can reduce re-trade risk by pre-clearing roof questions

The broker's roof role is not to inspect the building. It is to reduce avoidable ambiguity. A broker who represents a seller should know whether the roof file is strong, thin, or problematic before serious buyers start diligence. A broker who represents a buyer should know which roof records to ask for before the buyer commits too much time to an exchange replacement candidate.

Pre-clearing roof questions can include:

- What roof year is being represented, and what proves it?

- Does that year apply to all roof sections?

- Are there known leaks or repeated repairs?

- Is there a warranty, and is it transferable?

- Has severe weather occurred since the last inspection?

- Are there roof replacement bids or reserve estimates?

- Will roof access be available early?

- Is rooftop equipment tenant-owned or landlord-owned?

- Are there tenant complaints involving water intrusion?

This protects deal credibility. If the roof is strong, the broker can support the story with evidence. If the roof is weak, the broker can encourage realistic pricing or pre-market repair. If the roof is unknown, the broker can prepare the seller for buyer inspection requests.

Exchange buyers are often decisive when evidence is clear. They become cautious when the roof story changes late.

Commercial roofers can become acquisition partners without becoming deal advisers

Commercial roofers should not act as tax advisers, lawyers, lenders, or brokers. They can still be valuable acquisition partners. Their role is to inspect, document, explain roof condition, separate maintenance from capital, and help the buyer understand realistic intervention timing.

The most useful roofer deliverables in acquisition diligence are practical:

- Roof area map with observed conditions.

- Photo set covering field, drains, edges, equipment, penetrations, repairs, and access paths.

- Immediate repair list.

- Maintenance items.

- Recurring-risk observations.

- Replacement or restoration scenarios if warranted.

- Source limits and inaccessible areas.

- Questions that require consultant, engineer, warranty, or manufacturer input.

The roofer should avoid overclaiming. A roofer can say a roof area deserves further review because ponding, age, and repeated repair evidence line up. A roofer should not promise tax, insurance, warranty, or financing outcomes. The buyer needs roof facts, not cross-disciplinary certainty.

For Asset Optimix's channel strategy, this is a strong wedge. Roofers who can help owners and buyers think before emergency replacement are more valuable than roofers who appear only after water hits the floor.

A practical scoring model for 1031 roof diligence

A buyer can use a simple scoring structure during replacement-property review:

| Category | Low concern | Medium concern | High concern |

|---|---|---|---|

| Age evidence | Dated invoice/warranty by section | Seller statement with partial support | Unknown or conflicting |

| Condition evidence | Recent inspection with photos | PCA only or older inspection | No roof access or thin photos |

| Leak history | None or isolated and closed | Some recurrence, limited mapping | Repeated unmapped or active leaks |

| Weather exposure | No material events since inspection | Events with some follow-up | Severe events with no verification |

| Drainage | Clear maintenance evidence | Minor ponding or cleaning gaps | Persistent ponding or blocked drains |

| Equipment | Limited, controlled access | Moderate equipment with records | Dense equipment, weak penetration records |

| Consequence | Low tenant sensitivity | Moderate operating impact | Critical tenant, inventory, or public use |

| Reserve confidence | Supported and current | Rough but explainable | Stale, missing, or contradicted |

The score should not replace judgment. It should force the buyer to see which concern is driving the decision. A roof may be high concern because evidence is weak, not because condition is known to be poor. That distinction can lead to an inspection request instead of a price cut. Another roof may have strong evidence of real capital need, which should lead to reserve or price action.

What the buyer should know before identifying the property

For exchange-driven acquisitions, roof diligence should begin before formal identification when possible. The buyer may not be ready to commit, but the roof file can already inform whether the property belongs on the shortlist.

Before identification, the buyer should know:

- Whether roof access will be available.

- Whether roof age is documented by section.

- Whether there is a recent PCA or roof inspection.

- Whether leaks or repairs are known.

- Whether the roof is a near-term lender or insurance issue.

- Whether the property has high-consequence tenants.

- Whether severe weather occurred after the last roof review.

- Whether seller records are strong enough to support the asking story.

This does not mean roof diligence controls the whole exchange. It means a major capital component should not be discovered after the buyer's options have narrowed. Roof uncertainty is easier to manage before the buyer is boxed in.

Insurance placement can turn roof uncertainty into timing risk

Insurance often enters the acquisition process as a closing requirement rather than a strategic diligence workstream. That is a mistake for roof-heavy commercial assets. Roof condition, roof age, prior losses, maintenance evidence, and weather exposure can all influence the questions an insurer or broker asks before binding coverage. A buyer who waits until late in the exchange timeline to organize roof evidence may discover that insurance questions now compete with lender conditions and closing logistics.

The buyer does not need to predict the insurer's decision. The buyer does need to anticipate the evidence likely to be requested:

- Roof age by section.

- Most recent roof inspection or PCA roof observations.

- Photos of roof field, drains, edges, rooftop equipment, and repairs.

- Known leaks and repair history.

- Warranty and maintenance records.

- Severe weather exposure and post-event follow-up.

- Planned repairs or reserves.

- Tenant or occupancy details that increase consequence.

This evidence can help the buyer's insurance broker explain the risk earlier. It can also prevent a weak roof file from being mistaken for a bad roof. A maintained roof with older age may be more acceptable when the file shows inspection history, repair closeout, and a reserve plan. A newer roof with unknown sections, no photos, and repeated leaks may create more questions than its age suggests.

For insurtech and carrier teams, this is one reason commercial roof prediction is valuable. The most useful signal is not a claim that a roof is good or bad. It is a structured view of age confidence, vulnerability, weather exposure, maintenance evidence, and consequence. That view helps route risk-control attention before the policy conversation becomes urgent.

Material and contractor availability belong in the reserve conversation

Commercial roof capex is affected by more than condition. Material availability, contractor capacity, weather windows, tenant operations, equipment logistics, and regional labor conditions can change the practical cost of delay. A buyer who treats roof reserve as a static replacement estimate may miss the operational reality of executing the work.

The acquisition team should ask whether the roof plan depends on assumptions that could change:

- Is the roof system common in the local market?

- Are qualified contractors available in the needed season?

- Would work require tenant coordination, night work, phased access, or shutdown windows?

- Are rooftop equipment relocations or supports part of the scope?

- Is a tear-off likely, or could wet insulation/deck issues change disposal and staging?

- Would energy, wind, or code requirements affect replacement choices?

- Are there long-lead materials or warranty requirements?

These questions matter even when the buyer is not replacing the roof immediately. If the reserve assumes work can be done next year at a rough number, but the building has difficult access, high tenant sensitivity, and complex equipment, the reserve may be too thin. If the roof can be maintained for several years with straightforward local contractor support, the reserve posture may be more manageable.

Public cost indexes, including BLS producer price data, can give background on cost movement, but they cannot price a specific roof. The acquisition file should distinguish between cost-trend context and project-specific bids. A stale bid is not the same as a current scope. A generic reserve is not the same as a contractor proposal. A contractor proposal is not the same as a final price if hidden wet insulation or deck repairs remain unknown.

Portfolio buyers should compare roof risk across replacement candidates

Some 1031 buyers are not evaluating one building in isolation. They may be comparing several replacement candidates across markets. Roof diligence becomes more powerful when it is standardized across candidates. Otherwise, the buyer may over-focus on the property with the loudest roof issue and underweight a quieter property with weaker evidence.

A simple comparison table can help:

| Candidate | Roof evidence confidence | Near-term roof action | Weather/condition concern | Tenant consequence | Reserve posture |

|---|---|---|---|---|---|

| Building A | High | Maintenance only | Low | Moderate | Normal reserve |

| Building B | Medium | Specialist inspection | Wind exposure after last PCA | High | Uncertainty reserve |

| Building C | Low | Access required before close | Unknown age and repeated leaks | Moderate | Price/condition trigger |

The buyer should compare roof risk in the same language across properties. A building with visible defects but strong records may be easier to underwrite than a building with clean marketing language and no roof file. A building with a known $150,000 repair may be preferable to a building with unknown roof age, no access, and high tenant consequence. The question is not which roof has the least scary sentence. The question is which roof has the clearest path to a defendable decision.

This comparison also helps brokers and lenders. A buyer can explain why one replacement candidate is more attractive even if its roof is older. The reason may be better records, lower tenant consequence, stronger inspection access, or more realistic reserves. That is better than treating roof diligence as a binary pass/fail item.

The closeout file after acquisition matters too

Roof diligence should not end at closing. If the buyer acquires the property, the roof file should become an operating file on day one. Too often, diligence documents sit in a transaction folder while property management starts over with incomplete information. That wastes the value of the diligence process.

The post-closing roof file should include:

- Final roof records received from seller.

- PCA and supplemental roof review.

- Repair commitments and deadlines.

- Warranty transfer confirmation.

- Inspection photos.

- Leak log baseline.

- Roof access and vendor rules.

- Drain-cleaning schedule.

- Rooftop equipment ownership and maintenance responsibilities.

- Reserve assumptions and triggers.

- Open questions for first-year ownership.

This closeout file helps the new owner avoid repeating diligence work. It also gives commercial roofers a better starting point for maintenance. It gives insurance and lender stakeholders clearer follow-through. It helps asset managers track whether the acquisition reserve was accurate or needs revision.

For buyers using an exchange to enter a new market or asset class, this matters even more. The buyer may not know local weather patterns, contractor capacity, tenant roof access habits, or roof material history. A strong closeout file turns acquisition diligence into operating discipline.

Bottom line

A 1031 exchange buyer has to move quickly without letting speed turn into blind acceptance of physical risk. The commercial roof is one of the easiest places for hidden uncertainty to become visible late. That uncertainty can affect price, reserves, lending, insurance, tenant operations, and closing confidence.

The solution is not to demand perfect roof knowledge. The solution is to organize roof evidence early: age by section, PCA scope, inspection access, leak mapping, weather exposure, rooftop equipment, warranty status, repair history, consequence, and reserve confidence. The buyer should separate known cost from uncertainty cost and decide which missing facts require inspection before the exchange timeline tightens.

For brokers, a better roof file reduces re-trade risk. For lenders and insurers, it makes physical underwriting clearer. For commercial roofers, it creates an advisory role before emergency work. For owners and buyers, it turns a vague roof worry into a set of decisions.

Roof diligence is not the 1031 exchange. It is one of the physical realities that can decide whether the replacement property is actually as strong as the exchange strategy requires.

Frequently asked questions

Is roof diligence different for a 1031 exchange buyer?

The roof evidence itself is similar, but timing pressure changes the risk. Missing records, limited access, or late inspection findings can become more expensive when the buyer has exchange deadlines and fewer replacement-property options.

Can a PCA answer every roof question in an acquisition?

No. A PCA can be very useful, but roof-specific decisions may still need roof access, repair records, warranty review, mapped leak history, photos, or a qualified roof specialist depending on risk and consequence.

Sources and limits

Research basis reviewed against IRS like-kind exchange guidance, ASTM PCA framing, Fannie Mae PCA reserve guidance, NOAA/NCEI, NWS, WBDG, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- IRS like-kind exchangesOfficial IRS framing for like-kind exchange context; this article does not provide tax or legal advice.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, and useful life.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.