Capex planning

Commercial Roof Capex and Reserve Planning: Turning Roof Uncertainty Into a Buy, Hold, Lend, or Intervene Decision

A roof reserve is not just a replacement-year guess. It is an evidence file, an exposure history, a consequence model, and a timing decision that owners, buyers, brokers, and lenders can revisit as conditions change.

Key takeaways

- Roof capex planning should separate known defects, uncertain useful life, weather exposure, access limits, and consequence of interruption.

- A PCA is useful but can be too broad for roof-specific decisions unless records, access, photos, and roof consultant input are aligned.

- A reserve schedule should include inspection triggers, repair thresholds, replacement scenarios, and documentation requirements.

- Brokers and buyers can reduce late diligence surprises by requesting roof records before roof condition becomes a price fight.

Roof capex is a timing problem before it is a cost problem

Commercial roof cost is usually discussed as a number: replacement cost per square foot, remaining useful life, reserve amount, repair quote, insurance deductible, tenant improvement exposure, or acquisition adjustment. Those numbers matter. They are not the first problem. The first problem is timing under uncertainty.

A roof can be technically serviceable and still create a financing problem. It can be repairable and still create a tenant-interruption risk. It can have years of expected life and still trigger an insurance or lender concern because the file is thin. It can be near replacement and still be manageable if the owner has clean records, a reserve plan, and a credible intervention sequence. The capex question is not simply "what will the roof cost?" It is "when does this roof force a decision, who bears the consequence, and how much confidence do we have?"

That framing is useful for every commercial roof audience Asset Optimix wants to reach:

- Commercial roofers need to know which owners have a plausible reason to plan rather than wait for an emergency.

- Owners and heads of real estate need to decide whether to repair, restore, replace, monitor, or reserve.

- Brokers need to prevent roof uncertainty from becoming a late diligence discount.

- 1031 exchange buyers need to separate true roof risk from transaction anxiety inside compressed timelines.

- Lenders need reserve logic that reflects property condition and useful-life evidence.

- Insurers and insurtech teams need to distinguish maintained roof risk from unknown roof risk.

- Tenants and operators need to understand when roof condition threatens operations, inventory, or customer experience.

Commercial roofs are one of the most visible examples of physical underwriting because the same asset affects cash flow, insurance, debt, tenant operations, maintenance budgets, and sale price. A better roof reserve is not a spreadsheet cell. It is a decision structure.

The weakest roof reserve is replacement cost divided by remaining years

Many planning conversations start with a rough replacement number and an estimated remaining useful life. If the replacement is expected to cost $800,000 and the roof has eight years left, the reserve conversation may drift toward $100,000 per year. That arithmetic is simple. It can be dangerously thin.

The problem is that roofs do not consume value in a straight line. A roof can sit quietly for years and then require a large intervention after an event, tenant complaint, financing review, or failed repair. Another roof can receive targeted repairs and extend useful service because the vulnerable zones are understood. Replacement cost also changes with access, tear-off needs, wet insulation, deck condition, staging, code requirements, tenant operations, rooftop equipment, disposal, and market pricing.

A stronger reserve separates at least seven questions:

- What roof areas exist, and are they the same age?

- What is known about material, assembly, warranty, drainage, and repair history?

- What condition evidence exists from inspection, photos, leak logs, and invoices?

- What weather and climate exposure could accelerate intervention?

- What is the consequence of failure for tenants, operations, insurance, debt, and sale?

- What repair, restoration, and replacement scenarios are plausible?

- What evidence is missing, and how should missing evidence affect confidence?

Only after those questions are answered should a reserve become a number. The number can still be approximate, but it is no longer floating without context.

A roof reserve should have tiers, not one date

A commercial roof reserve becomes more useful when it is organized into tiers. The tiers do not need to be complicated.

| Tier | Meaning | Example action |

|---|---|---|

| Immediate maintenance | Small work needed to keep the roof functioning and documented | Clean drains, reseal isolated penetration, remove debris, repair walk pad gap |

| Near-term repair | Known condition likely to worsen if ignored | Address recurring leak area, repair flashing, correct localized ponding, fix damaged edge |

| Diagnostic review | Evidence suggests hidden or systemic issue | Moisture survey, core cut, roof consultant review, structural or engineering input |

| Capital reserve | Roof may remain serviceable but needs budget protection | Reserve for restoration, recover, tear-off, or phased replacement |

| Transaction protection | Roof risk may affect sale, refinance, insurance, or loan terms | Pre-market inspection, lender-ready roof file, buyer diligence packet |

This tiered view avoids two bad outcomes. The first is waiting too long because replacement seems expensive and far away. The second is pushing replacement too early because every roof concern is treated as total failure. The middle is where money is saved: targeted maintenance, well-timed inspection, disciplined repair, and honest reserve planning.

For commercial roofers, tiering creates a better advisory conversation. Instead of leading with a replacement pitch, the roofer can identify what should happen now, what should be watched, and when the owner should prepare for capital work. For owners and lenders, it creates a record of reasonableness. For brokers and buyers, it gives diligence a structure.

Property condition assessments are useful, but roof decisions often need more detail

Property condition assessments can be valuable in commercial real estate transactions and lending. They help identify apparent condition, deferred maintenance, immediate repairs, replacement reserve items, and useful-life concerns. Fannie Mae's multifamily guidance is useful because it emphasizes alignment among the physical inspection, PCA report, loan documents, captions, photos, component ratings, repair conclusions, and reserve needs. It also highlights how property needs and remaining useful life influence reserves.

The practical limitation is scope. A PCA is often broad by design. It may cover the whole property, not only the roof. Roof access may be limited. Weather may prevent close review. The roof may be observed from the ground, drone, hatch, or limited walk area. The report may include a useful-life estimate without a roof-consultant-level investigation. That does not make the PCA bad. It means the user should not treat it as the final roof answer when the roof is financially material.

Roof-specific decisions may need:

- Full roof area inventory by section.

- Membrane type and assembly notes.

- Drainage and ponding documentation.

- Flashing, edge, and penetration photos.

- Rooftop equipment and service-route map.

- Leak log and tenant complaint chronology.

- Repair invoice review.

- Weather exposure timeline.

- Warranty and transfer review.

- Moisture survey or core sampling where justified.

- Qualified roof consultant or engineering input for high-consequence cases.

The buyer, lender, insurer, or owner does not need all of that for every property. They need enough of it to support the decision in front of them. A 20,000-square-foot retail building with no recent leak history may need a different level of roof diligence than a 600,000-square-foot industrial facility with critical tenants, older roof sections, and recent severe weather exposure.

Roof records can protect value before a sale

Roof uncertainty creates negotiation leverage. If a buyer discovers late that roof age is unclear, repairs are undocumented, warranties are missing, or leak history is vague, the buyer will often price the uncertainty aggressively. Sometimes the discount is justified. Sometimes it is a response to poor documentation rather than poor roof condition.

Sellers and brokers can reduce this risk by treating the roof as a pre-market workstream. The strongest file includes:

- Roof replacement or installation records by section.

- Permit records where available.

- Warranties and transfer terms.

- Annual or semiannual inspection notes.

- Repair invoices with locations and scope.

- Leak logs mapped to suites, bays, rooms, or gridlines.

- Drain-cleaning and maintenance records.

- Rooftop equipment work affecting penetrations or curbs.

- Recent photos of roof field, edges, drains, parapets, and equipment.

- Weather events during ownership and whether post-event inspection occurred.

- Open roof issues and planned corrections.

This is not about making the roof look perfect. It is about making the roof legible. A buyer can tolerate known work better than unknown work. A lender can underwrite a documented reserve better than a surprise. A broker can tell a cleaner story when the roof file is ready before the first serious diligence call.

For 1031 exchange buyers, the same point applies from the other side. Time pressure can make weak records expensive. If the exchange timeline is tight, a roof file that would be merely inconvenient in a normal acquisition can become a go/no-go issue. Buyers should use roof-risk evidence to decide whether to inspect harder, seek escrow, reprice, require seller work, or accept the risk.

The reserve model should separate known cost from uncertainty cost

Owners often blend known and unknown roof risk into one budget. That hides the decision. A better reserve separates known cost from uncertainty cost.

Known cost includes work that has been identified with reasonable confidence:

- Clean and repair drains.

- Repair a specific flashing defect.

- Replace damaged walk pads.

- Repair punctures or open seams.

- Correct a localized ponding problem.

- Replace a damaged curb flashing.

- Complete a recommended inspection or moisture survey.

Uncertainty cost covers the possibility that missing information or weak evidence could change the scope:

- Unknown wet insulation quantity.

- Unknown deck condition.

- Unknown tear-off requirement.

- Unknown warranty transfer.

- Unknown number of roof sections.

- Unknown post-storm condition.

- Unknown effect of rooftop equipment work.

- Unknown tenant interruption cost.

This distinction helps decision-makers avoid false precision. A reserve can say, in effect: "The known maintenance need is modest, but the uncertainty reserve is larger because roof access was limited, age evidence conflicts, and multiple tenant leak tickets lack mapped locations." That is more useful than one blended number that nobody believes.

The uncertainty cost should fall as evidence improves. A post-inspection roof file, moisture scan, repair closeout, and updated photos can reduce uncertainty even if the roof still needs future work. Better evidence does not always reduce actual risk, but it reduces surprise risk.

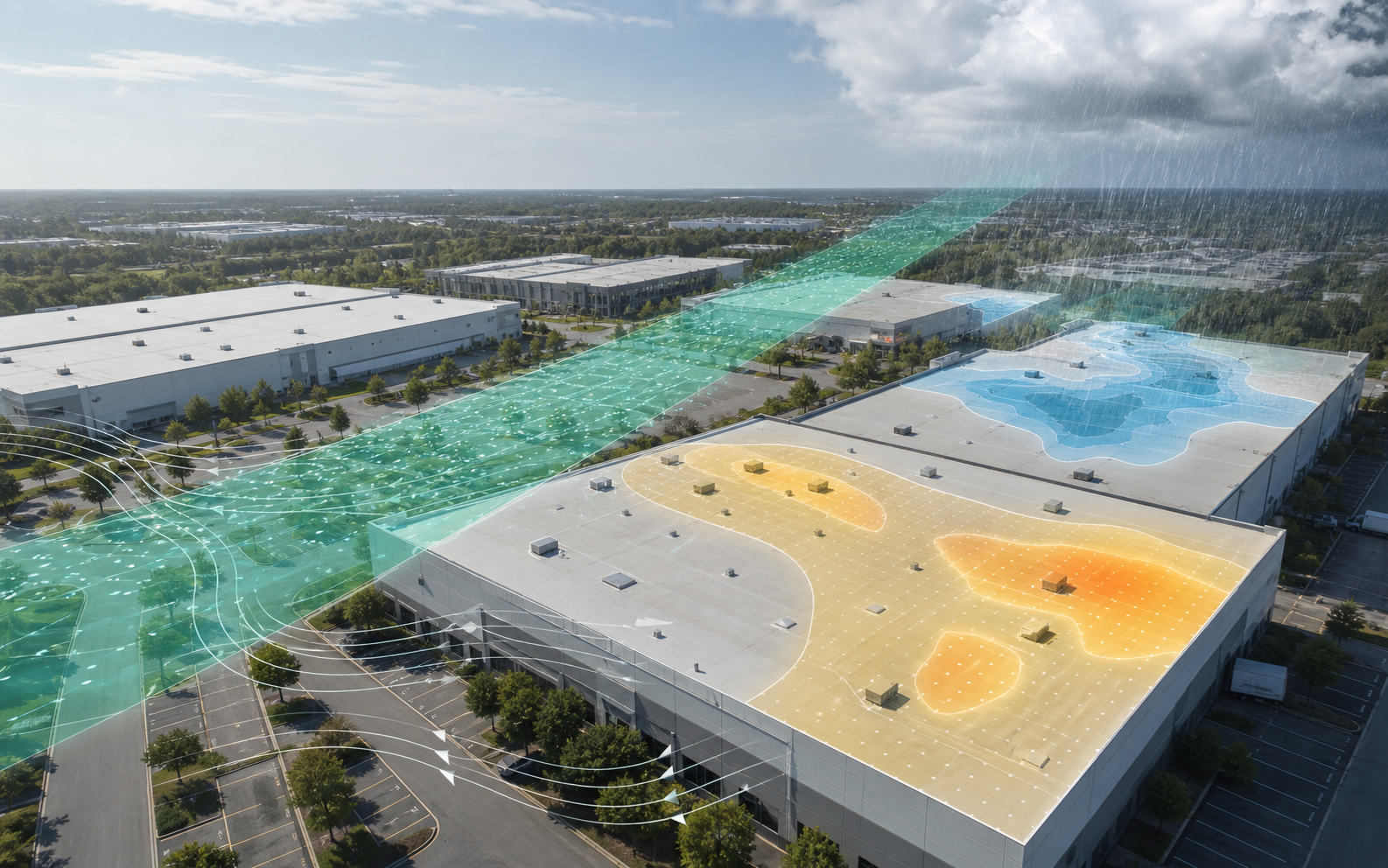

Weather exposure belongs in capex, not only insurance

Weather history is often treated as an insurance topic. It should also be treated as a capital-planning topic. Severe hail, wind, heat, heavy rain, and freeze-thaw exposure can change inspection timing and repair priorities even when no claim is filed. The NOAA/NCEI Storm Events Database and National Weather Service severe weather definitions provide useful public context for significant events. They do not prove parcel-level roof damage. They help decide whether a roof reserve should be revisited.

Weather-capex questions include:

- Did a severe hail or wind event occur near the building after the last roof inspection?

- Did leak tickets or repair calls increase after the event?

- Did the event affect roof accessories, rooftop equipment, skylights, or edge conditions?

- Is the roof older, heavily penetrated, poorly drained, or weakly documented?

- Does the building have tenants or operations that make roof interruption unusually expensive?

- Should the reserve schedule change because inspection confidence is now lower?

Weather exposure is especially important when it aligns with vulnerability. A newer roof with strong records and post-event inspection may not need a major reserve change. An older low-slope roof with unknown repairs, many rooftop units, ponding areas, and no post-event photos may deserve a larger uncertainty reserve even if no leak is visible yet.

The capital plan should not wait for a claim. It should respond to evidence.

Inflation and cost indexes are background, not bids

Roof planning happens in a moving cost environment. Public indexes such as the Bureau of Labor Statistics Producer Price Index can show broad price movement in construction and roofing contractor categories. They are useful background. They are not substitutes for bids.

Commercial roof pricing depends on variables that indexes cannot know:

- Region and labor market.

- Roof size and access.

- Tear-off, disposal, and staging.

- Occupied-building constraints.

- Deck repairs.

- Wet insulation quantity.

- Material choice and availability.

- Warranty requirements.

- Safety and logistics.

- Rooftop equipment complexity.

- Phasing and tenant restrictions.

- Code, wind, and energy requirements.

The right planning use of cost indexes is not to quote a roof from a public table. It is to remind the owner that an old reserve may be stale. If the last replacement budget was created three years ago, it should be refreshed. If the owner is buying a property, roof capex assumptions should be tested against current market quotes and alternate scenarios.

Good reserve language separates estimate class. A rough reserve is not a contractor proposal. A contractor proposal is not a final scope if hidden wet insulation or deck issues remain. A replacement budget without access assumptions is not final. This may sound conservative, but it prevents the capital plan from looking more precise than it is.

Roof capex is also an operating-expense conversation

The user described a key point: roofs are large capital assets, but many owners do not plan them with enough operating discipline. Maintenance spending, inspections, drain cleaning, leak response, and documentation often sit in operating budgets. Replacement sits in capex. The split can create bad incentives. If operating maintenance is deferred, capital replacement may arrive earlier and with less warning. If capital planning is ignored, operating repairs may become repetitive and wasteful.

The better view is lifecycle cost of ownership:

- Preventive maintenance reduces avoidable deterioration.

- Inspection creates decision-quality evidence.

- Timely repair prevents localized issues from spreading.

- Documentation reduces transaction and underwriting friction.

- Reserve planning prevents emergency financing.

- Replacement timing protects tenants and asset value.

This is not an argument to overspend on maintenance. It is an argument to connect maintenance to capital planning. A $5,000 maintenance action can be wasteful if it is the third temporary repair in the same failed zone. It can be valuable if it protects a serviceable roof and buys time for planned replacement. The difference is evidence.

For owners with multiple buildings, the portfolio view matters. The question is not only which roof is worst. It is which roof is most likely to create an expensive decision soon, and which intervention changes that trajectory. A smaller roof above a mission-critical tenant may outrank a larger roof above low-consequence space. A roof with a weak file may outrank a visibly older roof with strong maintenance history.

Lenders need reserve logic they can defend

Lenders do not need roof drama. They need enough evidence to decide whether the collateral has deferred maintenance, near-term capital needs, or operational risk that affects loan structure. A weak roof file can create conditions, escrows, reserves, or delays. A strong roof file may not eliminate roof concerns, but it makes them easier to size.

Useful lender-facing roof questions:

- What roof areas exist, and what are their approximate ages?

- What evidence supports those ages?

- What is the current condition and confidence level?

- Are there known leaks, active defects, or deferred maintenance?

- Are any components past useful life or near it?

- What is the recommended immediate repair amount?

- What replacement reserve is appropriate by year?

- Are there inspection, access, or documentation limits?

- Does weather exposure since the last inspection change confidence?

- Does tenant consequence require faster action?

The reserve answer should connect to the evidence. If a roof section is estimated at seven remaining years, the file should explain why. If a near-term repair is recommended, the file should show the source. If a roof is inaccessible, the confidence should fall. If photos contradict the PCA component rating, the contradiction should be resolved or flagged.

This is where physical underwriting overlaps with credit. Roof condition is not only maintenance. It affects collateral resilience, tenant income, operating cash flow, insurability, and exit value.

Brokers can make roof risk less adversarial

Brokers cannot make a roof newer. They can make the roof story cleaner. That matters because roof issues often become adversarial when the parties lack shared facts. A buyer sees an old roof. A seller says it has been maintained. A lender asks for reserve. An insurer asks for condition. A roofer says replacement is coming. Nobody has the same evidence.

A broker can reduce friction by asking for roof evidence before marketing:

- Installation records.

- Warranty information.

- Repair history.

- Inspection photos.

- Leak ticket summary.

- Maintenance schedule.

- Known open issues.

- Replacement or restoration bids if any.

- Roof consultant reports.

- Recent weather and post-event inspection notes.

Then the broker can present the roof as one of four stories:

- Strong roof file, low near-term concern.

- Known maintenance needs, manageable reserve.

- Material roof uncertainty, buyer should inspect early.

- Known capital event, price and timing should reflect it.

Those stories are more useful than generic phrases like "roof in good condition" or "newer roof." They also protect the broker's credibility. If the roof is a known issue, hiding it rarely helps. If the roof is not a major issue, proving that earlier can preserve value.

Commercial roofers can turn capex planning into better demand

A commercial roofer who only appears after leaks is competing in the most reactive part of the market. Capex planning creates a more advisory relationship. The roofer can help owners understand which buildings need inspection, which repairs are worth doing, which repairs are buying little time, and when capital work should be planned around tenants, weather windows, and budget cycles.

The strongest roofer-led capex conversations are specific:

- "This roof section is not an emergency, but recurring ponding near these drains should be corrected before it creates insulation or deck questions."

- "The roof can likely be managed this year, but the owner should carry a reserve because the records do not prove the age of the east section."

- "The recent wind event makes a perimeter inspection reasonable because the edge metal and prior repairs are the weak points."

- "Repeated leak calls below this equipment line suggest the next spend should not be another generic patch."

This language attracts more serious commercial buyers because it sounds like risk management, not pressure. It also aligns with how owners think about budgets. A planned roof project can be scheduled, financed, coordinated, and communicated. An emergency roof project disrupts everything.

A strong roof-risk platform should help roofers find and explain those planned opportunities.

A useful roof reserve changes when new evidence arrives

A reserve schedule should not be static. It should change when the roof file changes.

Update triggers include:

- New roof inspection.

- Severe hail or wind exposure.

- Repeated leak in same area.

- New tenant or operational consequence.

- Major rooftop equipment installation.

- Drainage failure or ponding change.

- Warranty expiration or transfer issue.

- Repair quote that changes scope assumptions.

- Moisture survey finding.

- Acquisition, refinance, renewal, or sale process.

Each trigger should answer one question: did the new evidence change timing, confidence, or consequence? If yes, the reserve should update. If no, the file should still record why.

This is where many commercial roof plans fail. The plan is created once, then left alone until the next emergency or transaction. Roofs are exposed assets. Their condition changes. The evidence should change with them.

A capex decision matrix for commercial roofs

The following matrix is a practical starting point:

| Condition | Evidence confidence | Consequence | Planning posture |

|---|---|---|---|

| Minor defects, strong records, low consequence | High | Low | Maintain and monitor |

| Minor defects, weak records, moderate consequence | Low | Moderate | Baseline inspection and uncertainty reserve |

| Recurring leaks in same area | Medium | Moderate to high | Targeted investigation and repair strategy review |

| Severe weather after last inspection | Medium | Depends on use | Post-event inspection trigger |

| Older roof, no age proof, buyer diligence pending | Low | High | Early roof specialist review and reserve discussion |

| Multiple zones, wet insulation suspicion, tenant interruption risk | Medium to high | High | Capital scenario planning and professional review |

| Known end-of-life roof with strong bids and schedule | High | High | Planned replacement or phased intervention |

This matrix does not decide for the owner. It keeps the conversation from drifting into slogans. The posture changes as evidence improves. A low-confidence roof can move to a more precise reserve after inspection. A high-confidence roof can move to urgent status if new damage appears. A low-consequence building can become high consequence when tenant use changes.

Acquisition diligence should make roof uncertainty explicit

Commercial real estate acquisitions often compress roof questions into a short diligence window. The buyer receives a PCA, seller documents, broker comments, roof photos, maybe a warranty, and sometimes a contractor opinion. If the buyer does not force roof uncertainty into the open, the issue can remain vague until it becomes a re-trade argument.

The diligence question should be split in two:

- What roof cost is already supported by evidence?

- What roof cost could emerge because evidence is missing?

Supported cost may include a repair proposal, maintenance recommendation, known warranty exclusion, planned replacement, or roof consultant finding. Missing-evidence cost may include unknown age, limited access, no post-storm inspection, unexplained leak history, undocumented equipment penetrations, or inaccessible roof sections. Buyers should treat those categories differently. A known repair is a scope question. Unknown wet insulation or unknown roof age is a risk-pricing question.

This distinction is especially valuable for 1031 exchange buyers. A buyer under time pressure may be tempted to accept weak roof information to keep the transaction moving. That may be the right business decision, but it should be explicit. If the buyer accepts uncertainty, the reserve should carry uncertainty. If the seller can reduce uncertainty with records or inspection access, the reserve can become more precise.

For brokers, this is a chance to protect deal momentum. A broker who knows the roof file is weak can ask for inspection access early. A broker who knows the roof file is strong can use that strength to reduce buyer concern. The roof does not have to be perfect; the story has to be defensible.

Tenant consequence can outrank roof age

Roof age is easy to compare across a portfolio. Tenant consequence is often more important. A ten-year-old roof over a sensitive operation can deserve more attention than a twenty-year-old roof over low-consequence storage if the failure impact is different.

Consequence factors include:

- Inventory value and water sensitivity.

- Electrical, medical, food, cold-storage, data, laboratory, or manufacturing use.

- Customer-facing operations.

- Lease obligations and service-level expectations.

- Public-sector continuity needs.

- Business-interruption exposure.

- Mold or indoor-air-quality sensitivity.

- Difficulty relocating operations.

- Access limitations for emergency repair.

This is why roof capex planning should not be owned only by maintenance. Real estate, finance, operations, risk, and tenant-facing teams may all need input. A roof reserve that ignores tenant consequence may look efficient until the wrong leak shuts down the wrong space.

Commercial roofers can use consequence to prioritize. Owners can use consequence to justify proactive inspection. Lenders and insurers can use consequence to ask better questions. Buyers can use consequence to decide whether roof uncertainty should affect price, escrow, or closing conditions.

Repair-versus-replacement math should include recurrence

Many owners ask whether to repair or replace. The better question is whether the next repair changes the recurrence pattern. A repair that addresses a true localized defect may be rational. A repair that repeats the same failure without addressing cause may be a signal that the roof has moved into capital territory.

Recurrence evidence includes:

- Multiple invoices for the same roof area.

- Repeated tenant complaints below the same zone.

- Similar repairs after each heavy rain.

- Patch expansion around an old repair.

- Persistent ponding despite repeated surface work.

- Equipment curb repairs after each service cycle.

- Repair spending that rises while confidence falls.

The recurrence pattern can change the reserve even before replacement is certain. It may justify diagnostic work, a restoration analysis, or a capital scenario. It may also show that the owner has been spending operating dollars without reducing risk.

The repair-versus-replacement conversation should include avoided consequence. If a replacement avoids repeated tenant disruption and emergency coordination, the value is not only longer roof life. It is operational control. If a repair buys two years of service with high confidence and low consequence, replacement may be premature. Evidence decides the difference.

Municipal and public portfolios need defensible prioritization

Municipalities, school districts, counties, agencies, and public-sector owners face a version of the same roof problem with added scrutiny. Public portfolios often contain many buildings, constrained budgets, procurement rules, public-service continuity needs, and aging assets. Roof decisions may be visible to boards, councils, taxpayers, auditors, or grant reviewers.

For public portfolios, a defensible roof reserve should show:

- Which buildings were reviewed.

- What evidence was available.

- Which roofs have active leaks or known defects.

- Which roofs have high public-service consequence.

- Which roofs have recent severe-weather exposure.

- Which roofs need inspection before budget commitment.

- Which interventions can be phased.

- Which projects should wait because evidence or consequence is lower.

This is not only a technical exercise. It is governance. A public owner may need to explain why one roof is funded before another. A ranking that combines condition, exposure, consequence, and confidence is easier to defend than a list sorted by age alone.

The same logic can extend from municipal roofs into paving, drainage, and exterior assets. Public infrastructure decisions need transparent prioritization under imperfect evidence. Roofs are a strong first category because failure is visible, expensive, and operationally disruptive.

Roof capex should be tied to partner economics

Commercial roofers, insurers, brokers, and lenders all care about roof capex, but they see different economics. A roofer sees inspection, maintenance, repair, restoration, and replacement demand. An insurer sees frequency, severity, loss control, and uncertainty. A broker sees deal friction and buyer confidence. A lender sees collateral resilience and reserve adequacy. An owner sees cash flow, tenant experience, and asset value.

Those economics can align when the roof file is specific. A roofer can win planned work instead of emergency work. An insurer can ask for targeted mitigation instead of broad caution. A broker can reduce late diligence volatility. A lender can size reserves with fewer surprises. An owner can spend at the right time rather than under pressure.

The conflict appears when roof evidence is vague. A generic "older roof" note may cause every party to protect itself. The buyer asks for a large credit. The lender adds a reserve. The insurer asks for more information. The owner feels the roof is being double-counted. The roofer is pulled into a reactive quote. Better evidence does not make the roof cheaper by magic, but it reduces defensive pricing.

This is why a roof-prediction company should care about partner workflows, not only model output. The roofer needs a reason to call. The owner needs a reason to listen. The insurer needs defensible segmentation. The broker needs a way to position uncertainty. The lender needs a reserve rationale. The best system gives each party the same evidence categories while allowing the action to differ.

The highest-value roofs are not always the worst roofs

For a channel partnership with commercial roofers, the most attractive buildings may not be the roofs in catastrophic condition. Catastrophic roofs are urgent, but they may already have active vendors, claims, emergency bids, tenant pressure, or owner frustration. The higher-value opportunity can be a roof that is not yet an emergency but has clear reasons to plan.

Examples:

- Older low-slope roof with weak records before insurance renewal.

- Retail roof with recurring drain issues but no capital plan.

- Industrial roof with dense rooftop equipment and repeated service traffic.

- Multi-building owner with inconsistent maintenance records across markets.

- Property coming to sale with a roof file that could be strengthened before diligence.

- Municipal portfolio where roof ranking needs to be defensible for budget approval.

- Lender or broker pipeline where roof uncertainty repeatedly slows transactions.

These are attractive because intervention can be advisory. The roofer can inspect, document, maintain, and plan before the building owner loses control of timing. The highest-value signal combines physical risk with business context.

That distinction matters for sales, underwriting, lending, brokerage, and ownership strategy, but the conversation should stay grounded in the roof problem. The audience needs to recognize its own expensive roof decision before it happens.

Reserve planning should make delay visible

Delay is not always wrong. A roof may be monitored for years when condition, consequence, and evidence support that choice. The problem is unpriced delay. If an owner decides to wait, the reserve plan should show what waiting assumes and what would break the assumption.

Delay assumptions can include:

- The roof remains leak-free through the next storm season.

- Known drainage issues are corrected before heavy rainfall.

- Repairs hold through the warranty or budget cycle.

- Tenant use does not become more sensitive to interruption.

- Replacement bids are refreshed before the next capital plan.

- Insurance or lender requirements do not change.

- No major rooftop equipment work adds penetrations.

When those assumptions are explicit, delay becomes a managed posture rather than passive avoidance. The owner can monitor the right signals. The roofer can explain why maintenance matters. The lender can see whether reserve timing is rational. The broker can explain why the roof is not being ignored.

This is also where cost of ownership improves. Planned delay with triggers can be financially sound. Unplanned delay usually transfers cost into emergency response, tenant disruption, rushed bids, and weaker negotiation.

What "reduce cost of ownership" really means

Reducing roof cost of ownership does not mean choosing the cheapest repair. It means reducing the total expected cost of uncertainty, interruption, emergency work, repeated repairs, and poorly timed capital. Sometimes the cheapest decision today is the most expensive decision over five years. Sometimes the expensive replacement recommendation is premature because targeted repair and monitoring would have been enough.

Cost of ownership includes:

- Preventive maintenance.

- Inspection and diagnostics.

- Repairs.

- Restoration or coating where appropriate.

- Replacement.

- Tenant disruption.

- Interior damage.

- Insurance friction.

- Financing friction.

- Transaction discounts.

- Staff time spent coordinating emergencies.

- Lost credibility with tenants or buyers.

The roof itself is only part of the cost. A leak above inventory or critical operations can create costs far beyond the roof repair. A roof uncertainty issue discovered late in a sale can cost more through re-trade than through actual near-term work. A weak reserve can create lender friction even if the roof is not failing.

The owner who plans earlier is not always spending more. Often they are buying options: time to bid, time to phase, time to coordinate tenants, time to choose scope, and time to avoid emergency pricing.

Bottom line

Commercial roof capex planning should not begin and end with a replacement year. It should connect roof records, condition, weather exposure, repair history, useful-life confidence, tenant consequence, and market cost assumptions. It should separate known cost from uncertainty cost. It should update when new evidence arrives. It should help roofers, owners, brokers, buyers, lenders, and insurers speak from the same file.

The best reserve is not the one that sounds most precise. It is the one that explains what is known, what could change, what would be expensive, and what action should happen before the roof becomes an emergency.

Frequently asked questions

Is a roof reserve just estimated replacement cost divided by remaining years?

That is too thin for commercial decision-making. A stronger reserve considers useful-life confidence, repair history, weather exposure, roof zones, tenant consequence, lender requirements, and inspection triggers.

When should a buyer ask for roof documents?

Before final price conviction. Ask early for roof age evidence, warranties, leak logs, repair invoices, inspection reports, drainage history, rooftop equipment work, and any recent weather-related documentation.

How does cost inflation affect roof planning?

Use public cost indexes as background, not bid substitutes. The practical move is to refresh estimates, separate material and labor assumptions, and keep alternates for repair, restoration, and replacement scenarios.

Sources and limits

Research basis reviewed against Fannie Mae PCA guidance, BLS PPI, WBDG, EPA, FEMA, NOAA/NCEI, NWS, and IBHS public guidance. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, and useful life.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings.