Broker diligence

What Brokers Should Ask Before Marketing a Building With a Flat Roof

A flat roof can be a routine diligence item or the reason a commercial real estate deal slows down. This guide gives brokers, owners, buyers, lenders, and roofers a practical pre-listing roof file.

Key takeaways

- Brokers do not need to certify roof condition, but they should organize roof evidence before listing language creates buyer expectations.

- Roof age should be separated by section and backed by invoices, warranties, photos, permits, or clearly labeled seller reports.

- Leak logs, drainage, rooftop equipment, warranty transfer, PCA scope, and weather exposure are often more important than a broad "new roof" statement.

- A stronger pre-listing roof file helps sellers avoid overclaiming, helps buyers underwrite faster, and gives roofers a useful advisory role.

Brokers do not need to become roof experts, but they do need better roof questions

A commercial broker does not sell the roof in isolation. The broker sells the building, the income stream, the occupancy story, the replacement-property fit, the owner narrative, and the buyer's path to confidence. Yet the roof can quietly control all of those things. A flat roof can become the reason a buyer slows diligence, asks for a credit, changes debt assumptions, calls an insurance broker, delays closing, or walks away from a listing that otherwise looked clean.

Most roof problems are not discovered because a broker missed a dramatic defect. They are discovered because the listing process treated the roof as a single line item: "roof replaced in 2016," "roof in good condition," "roof under warranty," or "seller reports no issues." Those statements may be partly true, but they often hide the details that buyers, lenders, insurers, and roofers actually need. Was the whole roof replaced or one section? Was it a recover? Was a coating sold as a replacement? Are there tenant leak tickets? Did rooftop equipment change after the warranty was issued? Did severe weather occur after the last inspection? Can the buyer access the roof during diligence? Are there repair invoices, or just owner memory?

This guide is for brokers, listing teams, owners preparing to sell, commercial roofers working with broker partners, lenders reviewing collateral, and buyers who want a clearer diligence conversation. It is not legal advice, tax advice, insurance advice, engineering advice, warranty interpretation, or a substitute for roof inspection. The point is simpler: before a building with a flat roof is marketed, the roof file should be organized enough that the broker can avoid weak claims, answer predictable questions, and know when a qualified roof professional should be involved.

The broker's role is not to certify the roof. The broker's role is to prevent avoidable uncertainty from becoming a late-stage surprise.

"Flat roof" is broker language, not a complete roof description

Buyers often say "flat roof" because that is what the roof looks like from the ground or aerial imagery. In commercial property work, it is usually more accurate to say low-slope roof. Even low-slope roofs are supposed to move water. They rely on slope, drains, scuppers, gutters, tapered insulation, crickets, overflow paths, edge details, penetrations, maintenance, and membrane condition to keep water from becoming an operating problem.

That distinction matters because a broker's listing language can accidentally turn a vague roof description into an overconfident condition statement. "Flat roof replaced in 2018" sounds simple. A stronger statement would separate what is actually known: "Seller provided a 2018 invoice for replacement of the main low-slope roof area; older canopy and mechanical well areas should be verified during diligence." The second statement is less flashy, but it is safer and more useful.

Low-slope commercial roofs also differ by system. A property may have TPO, PVC, EPDM, modified bitumen, built-up roofing, metal roof areas, coatings, recover assemblies, or multiple systems installed at different times. A buyer cares less about the label alone and more about the combination of system, age, drainage, penetrations, maintenance, repairs, warranty status, weather exposure, and consequence if the roof fails.

For broker work, the useful move is to stop asking only "How old is the roof?" and start asking "Which roof areas exist, what records support each area, and what still needs verification?"

The roof file should exist before the offering package is finalized

A broker should not wait for a buyer's property condition assessment to create the first roof file. By then, the deal already has momentum. If roof uncertainty appears late, every party reacts under pressure. The seller may feel accused. The buyer may demand a credit. The lender may ask for a reserve. The insurance broker may ask for more detail. The commercial roofer may be called into a compressed timeline. The listing team may have to correct statements that were too broad.

The roof file does not need to be perfect before launch. It needs to be honest. It should separate strong evidence from weak evidence, current facts from older observations, and known issues from open questions.

Minimum pre-listing roof file:

- Roof section map or simple sketch, even if approximate.

- Installation date evidence by section.

- Replacement, recover, restoration, coating, and repair invoices.

- Warranties and transfer requirements.

- Roof inspection reports and roof photos.

- Property condition assessment roof excerpts, if available.

- Leak logs, tenant complaints, and water-intrusion work orders.

- Drain cleaning or maintenance records.

- Rooftop equipment work that affected penetrations, curbs, supports, or traffic paths.

- Known open bids, deferred repairs, or capital plans.

- Recent severe-weather exposure and any post-event inspection notes.

- Roof access rules for buyer diligence.

This file gives the broker a better listing conversation. It also gives the seller a chance to fix avoidable gaps before buyers turn them into leverage.

The first broker question should be roof age by section

The phrase "roof age" sounds singular. Many commercial buildings do not have one roof age. Additions, partial replacements, tenant improvements, mechanical changes, storm repairs, roof recover work, coating projects, and isolated capital improvements can create several roof histories on one property.

This is especially common on industrial, retail, office-flex, medical, self-storage, warehouse, and mixed-use properties. The main field may have one date, a loading dock canopy another, a small office portion another, and a mechanical screen or penthouse another. If the listing compresses that into one date, the buyer may later discover that the advertised age applies only to part of the roof.

Broker roof-age table:

| Broker question | Better evidence | Risk if skipped |

|---|---|---|

| What roof areas exist? | Roof plan, aerial markup, inspection photos | One roof age hides older sections |

| What was replaced? | Invoice, scope, permit, warranty | Coating or recover may be mistaken for replacement |

| Was the whole roof included? | Section-by-section scope | Buyer finds excluded areas during PCA |

| Who performed the work? | Contractor invoice and warranty record | Seller memory becomes the only source |

| What changed later? | HVAC, solar, tenant, telecom, or exhaust work orders | Later penetrations may affect condition and warranty |

The broker does not need to determine useful life. The broker should avoid implying useful life when the evidence only supports installation history. "Installed in 2018" is different from "has 15 years remaining." The second statement usually requires professional judgment, scope awareness, and condition evidence.

Replacement, recover, restoration, coating, and repair are not interchangeable

One of the most common listing problems is language drift. A seller may say the roof was "redone." A broker may write "newer roof." A buyer may hear "full replacement." A PCA may later identify a coating or recover instead. The facts might not be bad, but the mismatch can damage trust.

Before marketing the building, the broker should ask what kind of work was performed.

Useful distinctions:

- Full tear-off and replacement: old assembly removed and new roof system installed, subject to scope details.

- Recover: new roof layer installed over an existing system, often with different limitations and due diligence questions.

- Restoration or coating: useful work that may extend service life but should not be described as full replacement unless documents support that.

- Targeted repair: localized work around seams, flashing, drains, penetrations, edge, or damaged areas.

- Maintenance: drain cleaning, sealant work, patching, walk-pad work, or small service items.

Those categories change the listing conversation. A restored roof can be a positive feature if described accurately. A recover can be acceptable if documented and understood. A repaired roof can show maintenance discipline. The problem is not the work type; the problem is calling one thing another.

If a broker cannot verify the scope, the listing should avoid definitive claims. "Seller reports roof work in 2021; invoices requested" is weaker than a full record, but it is better than overclaiming. The broker can still market the property. The broker should not turn a vague work history into a certainty that later collapses.

The offering package should state roof evidence, not roof optimism

Marketing language is designed to create interest. Roof language should create confidence without promising more than the evidence supports. The offering package is often the first place roof expectations are set, and the strongest broker teams treat roof claims as diligence claims.

Safer listing language is specific, dated, and bounded.

Weak language:

- "Excellent roof."

- "No roof issues."

- "New roof."

- "Roof under warranty."

- "No leaks."

- "Storm damage ruled out."

Stronger language:

- "Seller provided a 2019 invoice for main roof replacement; buyer should verify remaining roof areas during diligence."

- "Warranty document provided; transfer terms and exclusions should be reviewed by buyer."

- "Seller provided repair invoices from 2023 and 2024 for drain and flashing work."

- "Tenant leak log provided through March 2026; no open leak tickets reported by seller."

- "Severe-weather history should be reviewed as exposure context, not as property-specific damage proof."

The stronger language may look less promotional, but it can help a deal. Buyers trust bounded evidence more than broad comfort language. Lenders and insurers also prefer specifics because they can map evidence to risk. Commercial roofers can respond more effectively when the roof file has dates, sections, and photos instead of a vague promise.

Leak history should be mapped before it is summarized

Many sellers say "we fixed the leaks." That may be true, but the broker needs enough detail to understand whether the leaks were isolated or patterned. Leak history is less useful when it is summarized only as a count. Three leaks across unrelated areas may be manageable. Three leaks below the same drain, parapet, rooftop unit, or expansion joint may suggest a persistent problem.

The listing team should request the leak log before launch, not after the buyer asks. If no formal leak log exists, the broker can ask for tenant complaint history, work orders, emails, service invoices, and property manager notes.

Leak mapping fields:

| Field | Why it matters |

|---|---|

| Date reported | Shows chronology and relation to weather |

| Suite or interior area | Links symptom to tenant consequence |

| Roof zone above | Helps avoid vague building-wide conclusions |

| Nearby drain, edge, curb, or penetration | Points inspection to likely detail areas |

| Repair scope | Shows whether work was temporary or corrective |

| Recurrence | Separates one-time repair from pattern |

| Interior damage | Helps buyer understand business interruption and tenant impact |

The broker should not diagnose the source of water. Interior water can come from plumbing, facade, condensation, mechanical systems, or roof defects. The broker should organize the evidence so a qualified inspector or roofer can ask better questions.

If the seller has no leak history, the listing can still proceed. But "no records provided" is not the same as "no leaks." The broker should keep that boundary clear.

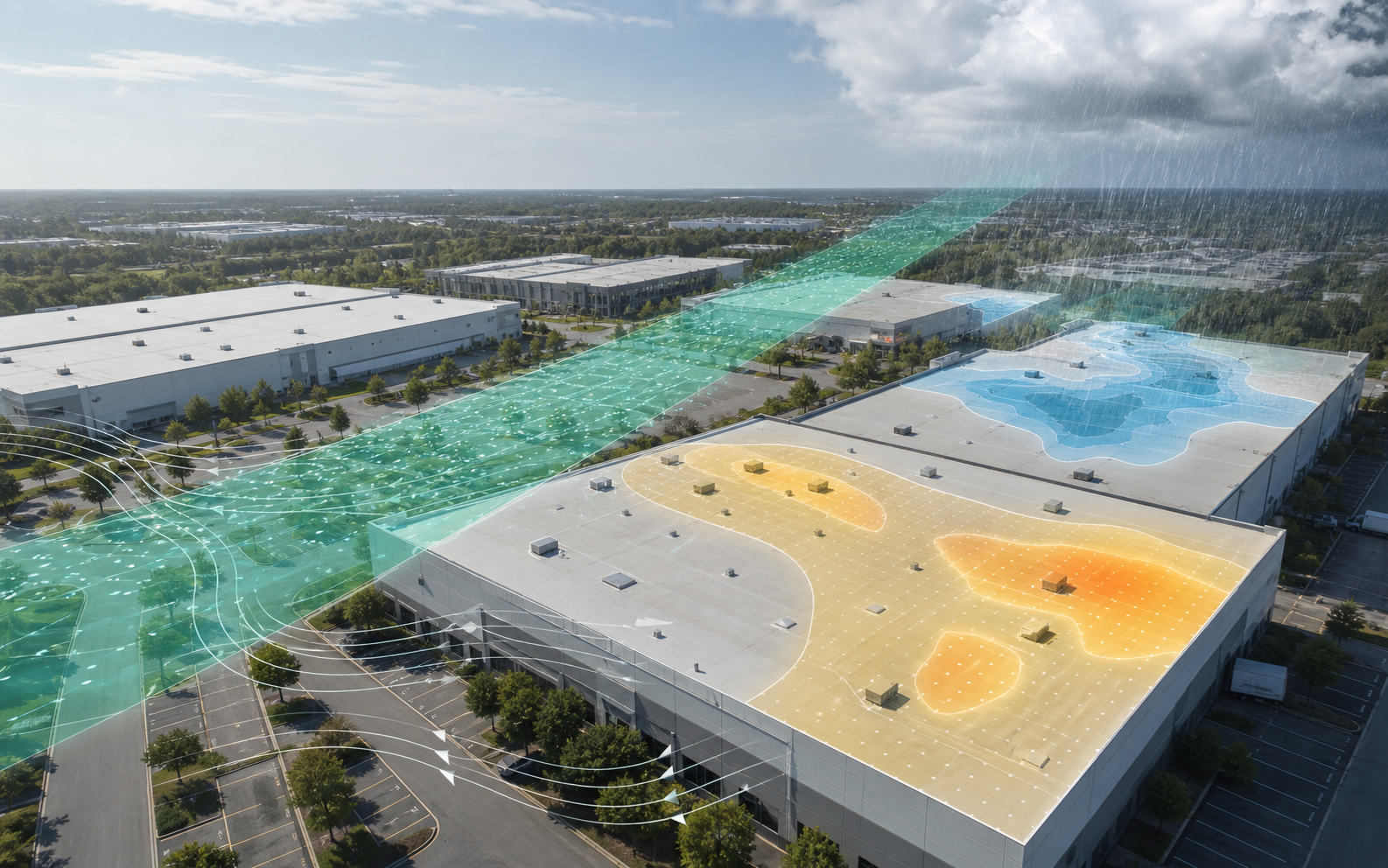

Drainage is often more important than the roof's age statement

Water movement is one of the first issues a buyer, roofer, or risk engineer should care about on a low-slope roof. A roof that does not drain well can become expensive even if it is not old. Ponding water, clogged drains, undersized drains, blocked scuppers, poor overflow paths, settled insulation, crushed areas, and debris can all change the practical risk.

Public building-envelope guidance commonly emphasizes collecting and disposing of rainwater, slope to drain, and moisture control. WBDG roof guidance discusses drains, valleys, gutters, downspouts, drainage paths, penetrations, and roof-system deterioration. EPA moisture guidance similarly frames low-slope roof design around collecting and disposing of rainwater. A broker does not need to cite those sources in a listing, but the broker should understand the practical implication: water behavior is a roof diligence issue, not a minor housekeeping note.

Pre-listing drainage questions:

- Are internal drains, scuppers, gutters, and downspouts visible and serviceable?

- Are drain baskets present and clear in recent photos?

- Are there known ponding areas after rain?

- Are there water stains below recurring roof areas?

- Are overflow drains or scuppers present where required?

- Are roof areas blocked by debris, tenant storage, grease, or equipment?

- Are maintenance records available for drain cleaning?

If a broker can obtain roof photos after rain, those photos can be useful. They should not be used to diagnose everything. They can show whether standing water is obvious and whether a roof professional should look more closely.

Rooftop equipment can change the roof story after installation

Commercial roofs are often working platforms. HVAC units, exhaust fans, kitchen vents, solar equipment, telecom equipment, conduit, refrigeration systems, skylights, hatches, anchors, and tenant improvements can add penetrations, curbs, supports, service traffic, discharge, vibration, and warranty questions.

A roof installed in 2018 may not be the same roof risk in 2026 if tenants added equipment, contractors cut new penetrations, service vendors walked the same paths repeatedly, or supports were placed without proper pads. This is why installation date alone is not enough.

Broker questions about rooftop equipment:

- What equipment is on the roof today?

- Which equipment was added after the last roof replacement, recover, or coating?

- Were penetrations installed by approved contractors?

- Were curbs, supports, walk pads, or pitch pockets modified?

- Are grease, chemical, condensate, or discharge exposures present?

- Are service paths protected?

- Do leak repairs cluster around equipment?

- Do warranties address later rooftop work?

The broker should be careful about "roof under warranty" when major equipment work happened after the warranty was issued. The warranty may still matter, but transfer rules, maintenance requirements, exclusions, and later penetrations should be reviewed.

For buyers, rooftop equipment can also change operating cost. A roof with many units may need a different maintenance plan than a simple roof of similar age. For commercial roofers, equipment density is a natural advisory opportunity because it shows where inspection and maintenance should focus.

Warranty documents should be treated as evidence, not blanket comfort

A roof warranty can help a listing. It can also create false comfort if the broker treats it as a simple promise that the buyer is protected. Warranties vary by issuer, scope, term, transfer conditions, exclusions, maintenance requirements, notice rules, and later-work rules. A warranty may cover materials differently from workmanship. It may require transfer within a certain time. It may exclude ponding, consequential damage, improper maintenance, unauthorized penetrations, acts of nature, or other conditions.

The broker should not interpret warranty coverage unless qualified to do so. The broker can organize warranty evidence.

Pre-listing warranty checklist:

- Get the full warranty document, not a summary.

- Confirm the covered address and roof area.

- Confirm issue date and expiration date.

- Identify whether the warranty is transferable.

- Ask whether transfer requires fee, form, inspection, or manufacturer approval.

- Ask whether later rooftop equipment work was approved.

- Ask for maintenance records required by the warranty.

- Ask whether warranty claims or notices were filed.

- Give buyers the document early enough for their own review.

Marketing phrase to avoid: "roof warranty transfers automatically." Unless the document clearly supports that and the broker is comfortable with the statement, it is better to say, "Warranty document available; buyer should review transfer requirements."

This is not timid. It is precise.

A PCA can help the broker, but it may not answer every roof question

Property condition assessments are common in commercial real estate transactions. ASTM E2018 is widely used as a guide for baseline property condition assessment work. Lenders, buyers, and investors may use PCA findings to understand immediate repairs, deferred maintenance, observed conditions, and capital planning. Fannie Mae multifamily guidance similarly emphasizes physical condition, deferred maintenance, remaining useful life, photos, repair needs, and replacement reserves.

A PCA can be valuable for a listing. It can also be too broad to answer every roof-specific question. The assessor may have limited roof access, limited records, weather constraints, safety constraints, or a scope that does not include moisture survey, core cuts, manufacturer warranty review, detailed roof consultant analysis, or full roof-zone mapping.

Broker PCA questions:

- Did the assessor access the roof directly?

- Were all roof areas observed?

- Are roof photos included?

- Does the report separate roof sections?

- Are access limitations stated?

- Does the report rely on seller-provided age?

- Are immediate repairs separated from long-term replacement reserves?

- Does the PCA address leak history?

- Were warranties, invoices, or repair records reviewed?

- Has severe weather occurred since the PCA date?

If the PCA roof section is thin, that does not mean the building is bad. It means the roof claim should remain bounded. A buyer may still need a roofer, roof consultant, moisture survey, or targeted inspection depending on roof consequence and deal size.

Weather history should raise inspection priority without becoming a damage claim

Weather is useful in roof diligence, but it is easy to misuse. NOAA/NCEI storm-event records and National Weather Service severe-weather definitions can help identify significant hail, wind, tornado, heavy rain, and other events in a region. Those records are exposure context. They do not prove that a specific roof was damaged.

This distinction matters for brokers. A listing team should not ignore relevant weather history, but it should also avoid turning weather exposure into a property-specific conclusion. The right question is not "Can we say the roof has storm damage?" The right question is "Does the weather timeline change what buyers should verify?"

Weather should trigger follow-up when it aligns with vulnerability:

- Older roof and significant hail or wind after the last inspection.

- Edge repairs or flashing concerns after high-wind exposure.

- Skylights, metal accessories, rooftop units, or solar equipment after hail exposure.

- Recurring leak tickets after heavy rain.

- No post-event inspection despite meaningful exposure.

- High tenant consequence below vulnerable roof zones.

Broker language should stay careful. "Weather exposure history available for buyer review" is different from "storm damage." If post-event inspections exist, include them. If they do not, say so internally and decide whether the seller should obtain a roof check before launch.

Cost and reserve conversations should happen before price becomes emotional

Roof cost uncertainty can become a price fight because it often appears late. The buyer sees a risk. The seller sees a re-trade. The broker is stuck between momentum and credibility. A better pre-listing roof file helps the seller decide whether to fix, disclose, reserve, price, or investigate before the listing is live.

The broker should ask the seller whether there are known roof bids, capital plans, insurance correspondence, maintenance contracts, or lender reserve requirements. If there are known costs, the broker can help the seller decide how they affect positioning. If there are uncertain costs, the broker can help decide whether a roof professional should provide current context.

Reserve thinking should separate:

| Category | Example | Broker use |

|---|---|---|

| Known repair | Drain flashing bid, open leak repair, warranty transfer fee | Seller can fix, credit, or disclose |

| Likely near-term work | Older section, recurring ponding, repeated patch zone | May justify pre-listing inspection |

| Uncertainty cost | No records, no roof access, unknown age | Affects buyer confidence and diligence timeline |

| Business consequence | Tenant interruption, refrigerated space, medical use, public building | Raises urgency and reserve sensitivity |

BLS construction and roofing price indexes can provide broad cost-trend context, but they are not a substitute for project bids. A broker should not use public indexes to price a specific roof job. The practical value is awareness that roof budgets can change and that old estimates may not support current deal decisions.

The seller should decide what to repair before the buyer asks

Some sellers should repair roof issues before launch. Others should disclose, price, or simply organize records. The right choice depends on defect severity, deal timeline, buyer pool, tenant consequence, and seller strategy.

Pre-listing repair may make sense when:

- A small repair removes a large buyer objection.

- A known leak is active.

- Drain cleaning or debris removal is overdue.

- Photos show obvious neglected maintenance.

- A warranty transfer or inspection requires corrective work.

- Tenant operations would make a roof issue unusually sensitive.

Pre-listing repair may not make sense when:

- The scope is uncertain and needs buyer-specific input.

- A buyer may prefer its own contractor or roof consultant.

- The seller cannot complete the work before launch.

- The repair could create overconfidence without addressing the underlying issue.

The broker should not push cosmetic roof work just to make a listing sound cleaner. The goal is not to hide risk. The goal is to remove avoidable friction and document what remains.

Roof access should be planned as part of diligence logistics

Some roof diligence problems are logistical. The buyer wants roof access. The seller has safety rules. The property manager needs notice. The roof hatch is locked. A ladder is needed. Weather interferes. The tenant controls access. The roof is not safe without escort. The diligence clock keeps moving.

A broker can reduce friction by planning roof access before the first serious buyer asks.

Access questions:

- How is the roof accessed?

- Who has keys or ladder access?

- Are there safety restrictions?

- Is escort required?

- Are tenant areas involved?

- Can buyer roofers or consultants access the roof?

- Is drone imagery allowed by property rules and local constraints?

- Are there weather limitations?

- Are photos available if physical access is delayed?

The broker should not promise access casually. If access is limited, the buyer should know early. Limited roof access may increase uncertainty, and that uncertainty can affect price, reserve, or closing conditions.

Weak records are not fatal, but they should be labeled

Many commercial buildings have weak roof records. Ownership changed. Property managers changed. Vendors changed. Files were lost. Work was done years ago. Smaller sellers may not have disciplined capital documentation. Weak records do not automatically mean the roof is bad.

Weak records do mean the listing team should avoid strong claims.

Record confidence bands:

| Confidence | Evidence state | Listing posture |

|---|---|---|

| High | Invoice, warranty, photos, section map, maintenance records | State facts with dates and scope limits |

| Medium | Some invoices, seller statement, partial photos, PCA excerpt | State what is available and what buyer should verify |

| Low | Seller memory, no invoices, no access, no photos | Avoid age/condition claims beyond seller report |

| Unknown | Conflicting statements or missing roof history | Treat as a diligence item, not a selling point |

The broker's credibility improves when uncertainty is labeled. A buyer may accept uncertainty if it is clear and priced. Buyers react badly when uncertainty appears after the listing suggested certainty.

Commercial roofers can be valuable broker partners if boundaries are clear

Commercial roofers are often brought into deals too late, after a buyer has already identified a concern. Brokers can create better outcomes by involving roofers earlier when the roof is material. The roofer can help document roof areas, identify visible maintenance needs, explain repair history, estimate inspection priorities, and give the seller a clearer view of roof readiness.

But boundaries matter. A roofer should not be asked to provide tax advice, legal advice, insurance coverage advice, engineering conclusions, warranty interpretation beyond its role, or inflated certainty. The roofer's value is practical roof knowledge and documentation.

Good broker-roofer collaboration:

- Pre-listing roof walk with photos and zone notes.

- Drain and debris observations.

- Review of repair invoice chronology.

- Identification of obvious access or safety issues.

- Separation of maintenance items from capital concerns.

- Plain-language explanation of what needs further inspection.

- Clear scope and limitations in any written notes.

Bad collaboration:

- Calling weather exposure proof of damage.

- Overstating remaining roof life.

- Treating a sales proposal as an independent condition assessment.

- Using fear language to force a transaction outcome.

- Replacing buyer diligence with seller-friendly conclusions.

The best roofer partner helps the broker and seller make the roof file more legible.

Lenders and insurers may ask roof questions differently than buyers

A buyer may ask whether the roof changes price. A lender may ask whether the roof changes collateral risk, reserves, repairs, or closing conditions. An insurer may ask about age, material, condition, maintenance, weather exposure, loss history, and building vulnerability. A broker does not need to answer all of those questions, but the broker should understand that roof diligence has multiple audiences.

The same roof file can serve all of them if it is organized well.

For lenders:

- Age by section.

- PCA roof section.

- Immediate repair items.

- Replacement reserve assumptions.

- Deferred maintenance evidence.

- Access limitations.

For insurance and risk review:

- Roof age and material.

- Recent inspections.

- Weather exposure and post-event response.

- Prior leaks or losses.

- Maintenance records.

- Rooftop equipment and edge conditions.

For buyers:

- What is known, what is uncertain, what costs are likely, and what access is available.

The broker's advantage is coordination. A strong roof file keeps the same facts from being recreated in different formats after every stakeholder asks.

The broker's pre-listing roof question set

Before marketing a commercial building with a flat roof, the broker should be able to answer or label the following:

- What roof areas exist?

- What is the evidence-supported age of each area?

- What work was replacement, recover, coating, restoration, repair, or maintenance?

- Are warranties available, and are transfer requirements known?

- Are roof photos current?

- Is there a leak log or tenant complaint history?

- Are repair invoices available?

- Are drains, scuppers, gutters, and overflow paths visible in photos?

- Are there known ponding areas?

- What rooftop equipment exists, and what changed after installation?

- Has severe weather occurred after the last roof inspection?

- Are post-event inspection records available?

- Did a PCA include direct roof access?

- Are immediate repairs or reserves identified?

- Can buyers access the roof during diligence?

- Are there safety, tenant, or scheduling limits?

- Are there open roof bids or capital plans?

- Which roof statements are strong enough for listing language?

- Which roof statements should be kept as seller reports rather than facts?

- Which open questions should be resolved before launch?

This is not a script to make every roof sound good. It is a discipline for making every roof sound accurate.

Listing language should separate facts, seller reports, and diligence invitations

The broker's wording can either reduce roof friction or create it. Roof language works best when each sentence tells the reader what kind of evidence supports it. A fact supported by a document should be stated differently from a seller memory. A visible observation should be stated differently from a professional opinion. A buyer diligence invitation should be stated differently from a marketing claim.

Useful categories:

| Category | Example | Better wording |

|---|---|---|

| Documented fact | Invoice for main roof work | "Seller provided a 2021 invoice for main roof work; scope available in diligence file." |

| Seller report | Owner says no active leaks | "Seller reports no active roof leaks as of listing date." |

| Visible observation | Photos show drains and rooftop units | "Recent roof photos are available for buyer review." |

| Professional opinion | Roofer or consultant notes condition | "Roof contractor notes dated April 2026 are available; buyer should review scope and limitations." |

| Open diligence item | Unknown age on rear section | "Rear roof section age has not been confirmed." |

This type of language may feel more cautious than normal marketing copy. It is often more effective because it preserves trust. A buyer can see that the broker is not hiding the roof, exaggerating it, or pretending every question is answered. The broker is showing the path to evidence.

The highest-risk words are usually broad adjectives: excellent, new, sound, problem-free, leak-free, warrantied, recently replaced, fully repaired. Those words may be defensible in some situations, but only when the supporting file is strong. If the support is weak, use narrower language. "Seller provided roof repair invoices from 2024" is safer than "roof fully repaired." "Warranty document available" is safer than "roof covered." "No open leak tickets reported" is safer than "no leaks."

This is not about making the listing dull. It is about preventing the roof from becoming a credibility problem after the buyer starts verifying claims.

Buyers will ask roof questions in different ways

The broker should expect buyers to approach the roof from different angles. A 1031 buyer may focus on closing certainty and reserve confidence. An owner-user may focus on business interruption. An industrial buyer may focus on tenant operations, rooftop equipment, and insurance. A value-add buyer may focus on capex timing. A lender-driven buyer may focus on PCA findings and replacement reserve requirements.

Common buyer questions:

- How old is the roof?

- Does the age apply to every roof area?

- Was it a replacement, recover, coating, restoration, or repair?

- Is the roof under warranty, and can the warranty transfer?

- Are there active leaks?

- What repairs were done in the last five years?

- Did the PCA include roof access?

- Are there photos from after the last major storm?

- Are there ponding or drainage concerns?

- Are there roof bids or known capital plans?

- Can our roofer access the roof during diligence?

The broker does not need to answer every question immediately. The broker should know where the answer lives, whether the answer is strong, and whether the seller needs to provide more evidence. "We have the invoice and warranty in the diligence folder" is a very different response from "The seller thinks it was done around 2018." Both may be acceptable if labeled correctly. The buyer's trust changes when the broker knows the difference.

For competitive listings, this preparation can matter before the best-and-final stage. A buyer that can underwrite roof uncertainty quickly may bid with more confidence. A buyer that discovers roof uncertainty late may add contingencies, reduce price, or demand extra time. The roof file is not just a property-management file. It can affect deal speed.

Some roof issues should pause launch or change timing

Not every roof issue should delay a listing, but some should make the broker and seller stop before publishing broad claims. The question is whether the issue is small, documented, and bounded, or whether it could materially change price, access, financing, insurance, or buyer trust.

Consider pausing launch or changing launch language when:

- There is an active leak and no repair plan.

- The seller plans to claim "new roof" but the records show partial work.

- The warranty is central to the story but transfer terms are unknown.

- A buyer cannot access the roof and no current photos exist.

- A recent severe-weather event occurred after the last roof inspection.

- The roof has recurring tenant complaints below the same area.

- A known roof bid is material to the asking price.

- The seller has conflicting statements about roof age.

- Rooftop equipment work may have changed the roof after installation.

- The lender or target buyer pool is likely to require a current roof review.

Pausing does not always mean delaying for months. It may mean getting current photos, asking for missing invoices, cleaning drains, obtaining a roofer's limited-scope note, clarifying warranty transfer, or rewriting the roof section of the offering package. Sometimes one day of document work can prevent three weeks of late diligence tension.

The broker should also know when not to pause. If the seller has weak records but the listing language is careful and buyers will have access, the property can still go to market. The key is not perfection. The key is not letting weak records masquerade as strong evidence.

The roof file should survive closing

Brokerage work often ends at closing, but the roof file should not disappear into a transaction archive. If the buyer closes, the roof documents should become part of the operating handoff. That matters for owners, property managers, lenders, insurers, roofers, and future resale.

Post-closing roof file:

- Final invoices and warranties.

- PCA roof section and photos.

- Seller repair history.

- Leak log baseline.

- Drain and maintenance records.

- Rooftop equipment notes.

- Warranty transfer evidence.

- Open repair commitments.

- Reserve assumptions.

- First-year inspection triggers.

This handoff is useful even when the broker is not responsible for post-closing operations. A buyer who receives a clean roof file can manage the asset faster. A seller who prepared the file can reduce disputes about what was provided. A future broker may inherit better records. A commercial roofer can maintain the roof with more context.

The strongest listing teams think of roof records as part of asset quality. Good records do not make a bad roof good, but they make a roof easier to understand, price, maintain, finance, insure, and eventually sell.

Bottom line

A flat roof can be a routine diligence item or the reason a commercial real estate deal becomes harder than it needed to be. The difference often comes down to preparation. Brokers do not need to inspect roofs, interpret warranties, estimate useful life, or prove weather damage. They do need to ask better questions before the listing goes live.

The strongest broker roof file separates roof areas, evidence-supported age, work type, warranties, leak history, drainage, rooftop equipment, weather exposure, PCA scope, access limits, known costs, and unresolved uncertainty. It helps the seller avoid overclaiming. It helps the buyer understand what is real. It helps lenders and insurers ask sharper questions. It gives commercial roofers a productive role before the emergency call.

The goal is not to make roof risk disappear. The goal is to make roof risk legible early enough that it can be priced, inspected, repaired, reserved, disclosed, or accepted without derailing the transaction.

That is what good brokerage discipline looks like when a commercial building has a flat roof.

Frequently asked questions

Should a broker say a commercial flat roof is in good condition?

Only when the evidence supports the statement and the limits are clear. Safer language identifies the document, date, roof area, seller report, inspection note, or open diligence item behind the roof claim.

What roof records should a seller gather before listing?

Ask for roof age evidence by section, replacement or repair invoices, warranties, transfer requirements, inspection photos, leak logs, tenant work orders, drain maintenance records, rooftop equipment changes, PCA roof excerpts, and known bids.

Can weather history be used in a broker listing package?

Weather history can be used as exposure context and an inspection trigger. It should not be presented as proof of property-specific roof damage without property-specific evidence.

Sources and limits

Research basis reviewed against ASTM PCA framing, Fannie Mae PCA reserve guidance, WBDG, EPA, NOAA/NCEI, NWS, IBHS, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, and useful life.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings, including low-slope roof drainage principles.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.