Physical underwriting

Roof Age Confidence Bands for Commercial Property Underwriting

Commercial roof age is not one number. This guide explains how owners, roofers, lenders, brokers, insurers, and buyers can separate documented age, inferred age, effective age, and remaining useful life.

Key takeaways

- Commercial roof age should be organized by roof section and work type, not collapsed into one building-level number.

- A roof can be old with high confidence, new with low confidence, or moderate risk with evidence gaps that change the next action.

- Chronological age, effective age, and remaining useful life are different fields and should not be used interchangeably.

- Confidence bands improve roofer advisory workflows, lender reserves, buyer diligence, insurance follow-up, and portfolio triage.

Roof age is useful only after confidence is attached

Commercial roof age sounds like a clean underwriting field. A broker asks for it. An owner answers from memory. A lender wants it in the property condition file. An insurer may ask for it during placement. A roofer may hear it on the first phone call. A buyer may use it to estimate replacement timing before a letter of intent. The number can feel objective because it is written as a year: installed in 2014, replaced in 2018, coated in 2021, repaired in 2023.

That simplicity is dangerous. A commercial roof is rarely one age. A building may have a main field membrane, an older canopy, a newer addition, recovered sections, coating work, tenant-driven penetrations, replaced flashing, abandoned curbs, and edge metal that does not match the field. Even when the installation year is correct, the age may not describe condition, remaining useful life, weather exposure, hidden moisture, drainage behavior, access limits, or the confidence behind the records.

The better underwriting question is not "How old is the roof?" It is "What roof areas exist, what age evidence supports each area, what condition evidence modifies the age, and how confident are we?"

That is the purpose of roof age confidence bands. They let owners, commercial roofers, insurers, brokers, 1031 exchange buyers, lenders, and asset managers use age without pretending that age is the whole roof. A confidence band separates known installation history from believed history, from inferred history, from unknown history. It keeps a clean roof file from being treated like a vague seller memory. It also keeps a vague seller memory from being priced as though it were a transferable warranty and a current inspection.

Asset Optimix uses this framing because roof prediction and physical underwriting are only useful when uncertainty is visible. Confidence is not decoration. It changes the next action.

Chronological age, effective age, and remaining useful life are different

Three phrases often get blended in roof conversations: chronological age, effective age, and remaining useful life. They should be separated.

Chronological age is the time since installation, replacement, recover, coating, restoration, or repair. It is a history field. If a roof section was installed in 2016, the chronological age is tied to that date. The date might be supported by an invoice, permit, warranty, contractor proposal, closeout package, inspection note, accounting record, or seller statement. The date is still only a date.

Effective age is a condition-adjusted idea. A ten-year-old roof with chronic ponding, repeated open seams, dense rooftop equipment, poor access control, and thin records may behave like an older roof for underwriting purposes. A fifteen-year-old roof with strong maintenance history, clear drainage, transferable warranty terms, and recent roof consultant photos may be easier to underwrite than a newer roof that nobody can explain. Effective age is not a casual label. It should be tied to observed condition and records.

Remaining useful life is a forward-looking estimate. It asks how long a component is expected to remain serviceable before replacement, major restoration, or major repair becomes likely. Property condition assessments and lending files often use remaining useful life when discussing reserves. That estimate is useful, but it should not be detached from scope, access, inspection date, and evidence quality.

A clean roof file keeps these separate:

| Field | What it says | What it does not say by itself |

|---|---|---|

| Chronological age | When a roof area or component was reportedly installed or improved | Current condition, hidden moisture, workmanship quality, or future performance |

| Effective age | How condition and use make the roof behave relative to its calendar age | Exact replacement year or warranty interpretation |

| Remaining useful life | Expected period before significant intervention | Certainty, cost, coverage, code compliance, or inspection replacement |

When these three fields are merged, decisions get sloppy. A buyer may assume a "2018 roof" means five more comfortable years when only one section was replaced. A lender may accept a remaining useful life estimate without noticing that roof access was limited. A broker may repeat a seller's roof age statement without distinguishing replacement from coating. A roofer may inherit unrealistic expectations before seeing the roof.

Confidence bands keep those errors from becoming the working assumption.

A confidence band is not a risk score

A roof age confidence band describes how strongly the file supports the age claim. It is not the same as a roof risk score.

A roof can be old and high confidence. It may have invoices, permits, warranties, annual inspection photos, drainage records, and repair history. The age is not flattering, but the file is clear. That roof may still need replacement planning, but it can be underwritten with fewer unknowns.

A roof can be new and low confidence. It may have a seller statement that says "new roof," but no section map, no scope, no warranty transfer information, no closeout photos, no detail on whether the work was a recover, no note on insulation, and no record of rooftop equipment changes after the work. The age sounds favorable, but the evidence is weak.

A roof can be moderate risk and low confidence. That is often the most frustrating category because the next action is not obvious from age alone. The building may need an inspection, seller record request, reserve adjustment, or lender discussion before price conviction.

For physical underwriting, confidence tells the user how much weight to put on the conclusion. It should answer:

- What evidence supports the age?

- Does the evidence map to the full roof or only a section?

- Is the evidence recent enough to matter?

- Does condition evidence agree with the age claim?

- What important facts remain unknown?

- What decision would change if the confidence improved?

That last question matters. Do not collect roof age evidence as paperwork theater. Collect it because it changes inspection priority, reserve timing, lending conditions, insurance questions, acquisition pricing, or roofer follow-up.

A practical four-band framework

Asset Optimix uses a practical four-band structure for roof age confidence. The bands are intentionally plain because the output needs to be understood by people who do not all share the same technical background.

| Band | Meaning | Typical evidence | Practical action |

|---|---|---|---|

| Documented | Age is supported by strong records tied to roof sections | Invoices, warranty, permit, closeout package, roof plan, dated inspection photos | Use as a working age field, then adjust for condition and exposure |

| Supported | Age is supported but some detail is missing | Seller records, accounting entries, contractor letter, partial invoices, PCA notes | Use with caveats and request missing detail when material |

| Inferred | Age is estimated from indirect evidence | Aerial history, ownership memory, patch chronology, material clues, appraisal notes | Treat as provisional and schedule validation if the roof matters |

| Unknown | Age cannot be responsibly assigned | Conflicting statements, no records, inaccessible roof, no section history | Lower confidence, request inspection or reserve for uncertainty |

The framework does not require perfect knowledge. It requires honest labeling. A roof section with an unknown age can still be leased, financed, insured, repaired, or acquired. The problem is not the unknown. The problem is acting as though the unknown is known.

For example, a buyer reviewing a distribution building may see one roof note: "Roof replaced approximately 2017." A better file might say:

- Main warehouse field: supported, seller invoice indicates 2017 recover, full scope pending.

- Office roof: unknown, no records located, visible from aerial as separate lower roof.

- Loading canopy: inferred, older modified bitumen visible in photos, no age evidence.

- Edge metal: supported, replaced in 2020 repair invoice, warranty limits not reviewed.

That file is not longer for its own sake. It prevents false precision. It also gives every stakeholder a better next question.

Roof age belongs at the section level

Many commercial buildings have multiple roof areas. A single roof age can hide the exact section that creates the next intervention.

A building may include:

- Original warehouse roof.

- Later office addition.

- Retail canopy.

- Mechanical penthouse.

- Lower loading dock roof.

- Stair or elevator overrun.

- Recovered section.

- Coated section.

- Storm-repaired section.

- Tenant improvement area with new curbs and penetrations.

Each area can have a different age, system, drainage pattern, consequence, and evidence level. If the file collapses all of that into one age, the underwriting result becomes misleading. A weighted average roof age can be especially deceptive. If 85 percent of the roof is documented as newer and 15 percent is unknown over a critical tenant space, the smaller unknown section may drive the reserve or inspection priority.

Section-level age also helps commercial roofers. A roofer speaking with an owner or broker can quickly separate education from immediate opportunity. The conversation becomes more precise:

- Which roof areas have clean installation records?

- Which areas have no age support?

- Which areas have recurring leak tickets?

- Which areas have concentrated rooftop equipment?

- Which areas have the highest tenant consequence?

- Which areas need inspection before a financing, sale, or renewal conversation?

For brokers and buyers, section-level age supports better diligence language. "Seller reports portions of the roof were replaced in 2019" is more honest than "new roof" when only one section is documented. For lenders and insurers, section-level evidence helps distinguish a manageable maintenance item from a building-level uncertainty.

Replacement, recover, restoration, coating, and repair are not the same age event

Roof age errors often start when different types of work are described with the same word. "New roof" is used casually in sales conversations, but the scope behind the phrase can vary widely.

A full replacement may remove old membrane and wet insulation, replace damaged deck where needed, install new insulation and cover board, and install a new membrane system. A recover may place a new roof system over an existing one under specific conditions. A restoration or coating may extend service life of an existing system when the underlying roof is a suitable candidate. A repair may address a leak, flashing, curb, drain, seam, puncture, or edge condition without changing the age of the roof system.

For confidence bands, the first question is not whether the work was valuable. Many recover, restoration, coating, and repair projects are valuable. The question is what age field the work supports.

| Work described | Age implication | Confidence concern |

|---|---|---|

| Full tear-off replacement | May support a new roof system age if records are complete | Need section map, scope, insulation/deck notes, warranty, completion date |

| Recover | Supports age of recover system, not necessarily hidden existing system | Need eligibility, existing roof condition, moisture findings, deck limits |

| Coating or restoration | Supports restoration date, not full replacement age | Need substrate condition, prep, warranty terms, maintenance duties |

| Localized repair | Supports repair chronology, not roof age reset | Need location, repeated pattern, cause, follow-up evidence |

| Edge or flashing replacement | Supports component age, not field membrane age | Need tie-in details and whether repeated failures continue |

This is where sloppy language becomes expensive. If a broker markets a building as having a new roof because a coating was installed, the buyer may underwrite incorrectly. If an insurer hears "2019 roof" but later sees a recover over an unknown assembly, the file may lose credibility. If a lender uses a remaining useful life estimate without knowing the scope behind the date, the reserve may be too low.

The stronger answer is simple: describe the work as the records describe it, then label the confidence.

Age evidence has a hierarchy

Not all roof age evidence carries the same weight. A well-organized file should distinguish primary evidence, supporting evidence, indirect evidence, and weak evidence.

Primary evidence includes documents created close to the work and tied to a roof area: executed contracts, invoices, permits, warranty documents, closeout packages, roof plans, submittals, inspection sign-offs, and dated progress photos. These are often the best foundation for a documented band.

Supporting evidence includes seller capital ledgers, property management records, contractor letters, PCA excerpts, insurance inspection notes, accounting records, and maintenance summaries. These can be useful, but they may not include enough scope detail to prove exactly what was installed.

Indirect evidence includes aerial imagery, material appearance, patch patterns, tenant complaints, appraisal notes, ownership memory, and repair vocabulary. Indirect evidence can help form an inferred band, especially when direct documents are missing, but it should not be overstated.

Weak evidence includes broad statements without date, scope, or source. "Roof is newer," "roof is fine," "roof was done before purchase," or "no known issues" may be a starting point for questions, not a confidence band by itself.

The file should also recognize contradictions. A warranty may say one date, an invoice may describe a different section, and a PCA may assign another apparent age. Contradictions do not automatically mean someone is wrong. They often mean the roof has more than one area or more than one type of work. The responsible move is to separate the sections and scope until the conflict is explained.

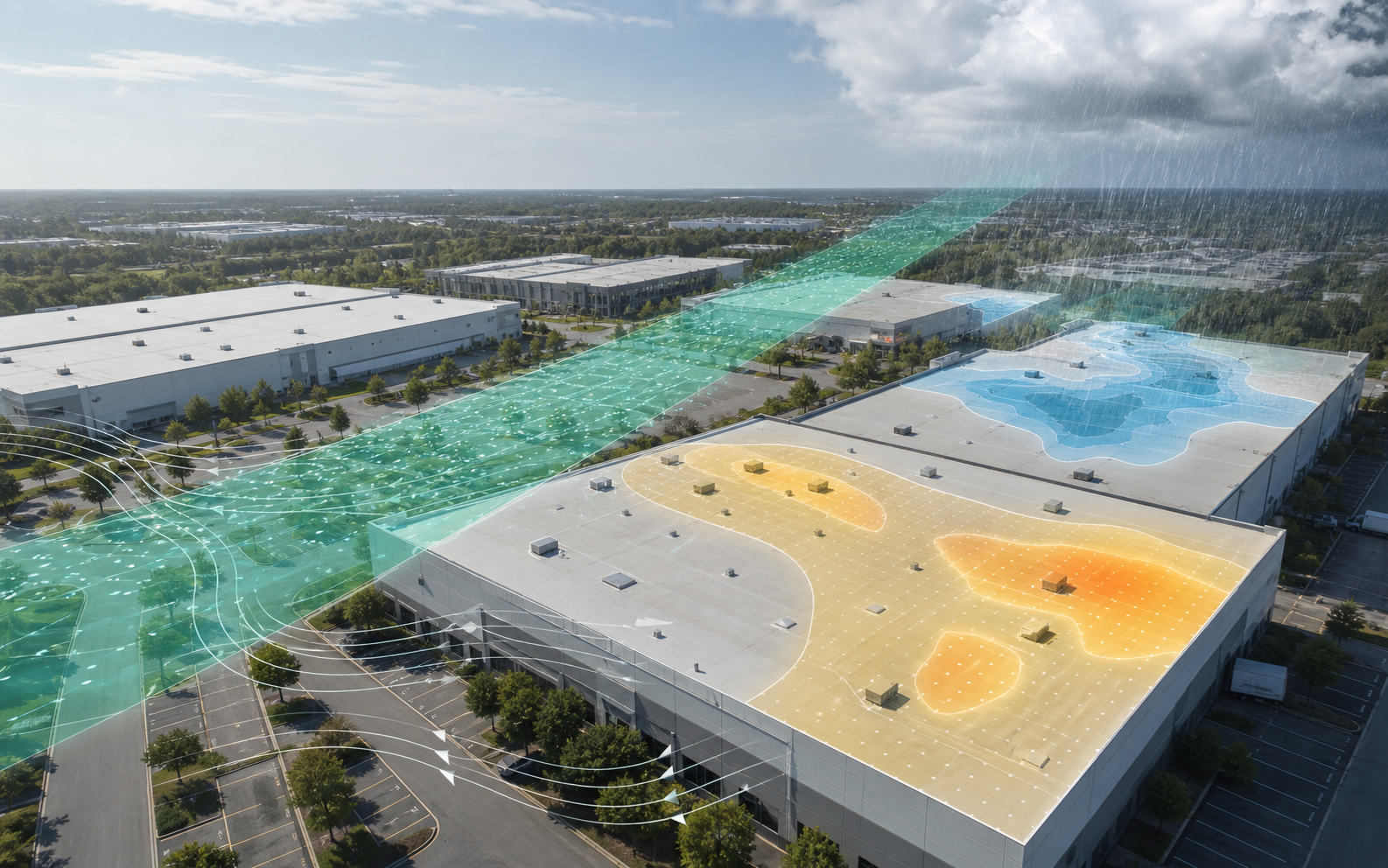

Condition can move the practical age up or down

A roof's chronological age is fixed, but the practical underwriting posture changes with condition. This is why age confidence should be paired with condition confidence.

Condition evidence may include:

- Current roof photos.

- Infrared or moisture scan findings.

- Drainage observations.

- Ponding areas.

- Open seams or laps.

- Membrane shrinkage or splits.

- Blisters, ridges, punctures, or exposed reinforcement.

- Edge metal and coping condition.

- Flashing and curb details.

- Rooftop equipment condition.

- Walk pad coverage.

- Leak logs.

- Repair invoices.

- Tenant work orders.

- Maintenance records.

An older roof with clean current photos and orderly maintenance may remain a planned capex item. A newer roof with unresolved drainage and repeated leak repairs may become an immediate diligence concern. The confidence band should not let the date silence the condition evidence.

For underwriting, the most useful paired output looks like this:

| Roof area | Age band | Age confidence | Condition confidence | Practical note |

|---|---|---|---|---|

| Main field | 2016 installation | Documented | Medium | Records strong, but current photos are nine months old |

| Office roof | Unknown | Unknown | Low | No records, limited access, leak history near west parapet |

| Loading canopy | 2008 estimate | Inferred | Medium | Aerial and repair history support older band, inspection needed |

This kind of table gives the next action. The office roof is not automatically the worst roof. It is the least understood roof, which may be enough to change the diligence plan.

Drainage can make a younger roof behave older

Drainage is one of the most important modifiers of roof age confidence. Low-slope roofs are designed to move water, but real buildings collect debris, settle, change use, add equipment, and develop maintenance gaps. A younger membrane does not eliminate drainage concern if the roof repeatedly holds water or if drain maintenance is weak.

Drainage evidence should include drains, scuppers, gutters, overflow provisions, slope changes, interior drain history, clogged strainer history, ponding locations, and any repairs tied to standing water. If a roof's age is documented but drainage evidence is poor, the practical confidence in useful life should drop.

This does not mean every ponding mark is catastrophic. It means the file should not use age as a shield against visible behavior. A roof that was installed five years ago and still ponds around multiple drains after routine rain may deserve earlier inspection than a twelve-year-old roof with clean drainage records and no recurring leak locations.

For roofers, drainage is a strong advisory opening because it connects maintenance, inspection, and owner education without overclaiming. For lenders and buyers, drainage can move a roof from a distant reserve line to a condition that needs confirmation before closing. For insurers, poor drainage can indicate a building where age alone understates vulnerability.

Weather exposure should adjust confidence, not pretend to prove condition

Weather history is a key part of physical underwriting, but it should be used carefully. A hail report, wind event, tropical rainfall period, freeze-thaw cycle, heat exposure, or severe thunderstorm nearby does not prove that a specific roof was damaged. It does, however, change what questions should be asked.

If a documented roof age predates a major weather exposure, the confidence in current condition may be lower unless there was a post-event inspection or maintenance record. If the roof was inspected after the event and the file includes photos and repair notes, confidence may remain higher. If the roof has unknown age and significant nearby weather exposure, the uncertainty compounds.

A useful age-confidence record separates:

- Age evidence: what supports the installation or work date.

- Exposure evidence: what weather occurred near the property.

- Condition evidence: what was observed on the roof.

- Response evidence: what inspection, repair, or maintenance followed.

That separation protects all parties. It keeps a roofer from implying damage based only on a weather record. It keeps an underwriter from ignoring a meaningful exposure. It keeps a buyer from treating the absence of a claim as proof of no roof issue. It keeps a broker's diligence package more defensible.

For deeper context on this distinction, the existing [roof weather risk and physical underwriting guide](/insights/roof-weather-risk-physical-underwriting/) explains why weather records are exposure context, not property-specific proof of damage.

Remaining useful life estimates need an evidence note

Remaining useful life is common in property condition assessments and lending files. It helps translate physical condition into capital planning. The problem is that remaining useful life can look more precise than the evidence behind it.

An estimate should always carry an evidence note:

- What roof areas were accessible?

- Was the roof observed directly or from limited vantage points?

- Were records reviewed?

- Were photos included?

- Were roof sections separated?

- Was the estimate tied to a system type?

- Was moisture testing performed or excluded?

- Was the estimate made before or after major weather exposure?

- Were tenant leaks or repairs considered?

- Does the estimate conflict with invoices, warranties, or owner records?

The note does not have to be long. It has to prevent misuse. "RUL 7 years" is thin. "RUL 7 years for main field based on June 2026 visual roof observation, seller invoice, and no reported active leaks; office addition excluded because access was not provided" is much more useful.

Fannie Mae multifamily property condition guidance is helpful beyond its direct lending setting because it emphasizes physical condition, deferred maintenance, useful life, photos, repair needs, and replacement reserves. Those categories map well to commercial roof underwriting. ASTM E2018 also gives transaction teams a recognized property condition assessment framework. Neither should be treated as a substitute for roof-specific judgment when the roof is financially material.

Useful life tables are starting points, not verdicts

Estimated useful life tables can anchor a conversation. They give lenders, assessors, owners, and consultants a common reference point for components. But a table is not a roof inspection. A roof's actual performance depends on design, installation, materials, drainage, climate, maintenance, traffic, rooftop equipment, repairs, and prior recover or restoration work.

The right use of an estimated useful life table is to frame a question:

- Is the roof within a normal planning window for its system?

- Are current condition observations better or worse than expected?

- Are records strong enough to support the age?

- Are there reasons to shorten the planning horizon?

- Are there reasons to maintain confidence in a longer planning horizon?

The wrong use is to treat a table as a replacement year calculator. If a table suggests a broad useful life range and the roof's age falls near the middle, the decision is not finished. The underwriter still needs evidence.

This is especially important when the roof system is only generally described. "Single-ply roof" is not the same as a detailed assembly record. "Built-up roof" does not explain drainage, insulation, recover history, or condition. "Metal roof" does not explain fasteners, coating, penetrations, seams, or corrosion. Useful life tables need roof-specific facts to become useful in decisions.

The lender view: age confidence affects reserves and conditions

Lenders care about roof age because the roof can affect collateral condition, cash flow, future capital needs, insurance placement, tenant operations, and default risk. A lender may not need perfect roof knowledge, but it needs enough confidence to decide whether reserves, repair conditions, holdbacks, or additional diligence are reasonable.

Age confidence changes the reserve conversation:

- Documented age and current condition can support a more targeted reserve.

- Supported age with missing scope may justify a reserve plus a document request.

- Inferred age may require inspection before closing or a conservative reserve.

- Unknown age with leak history may become a repair condition or pricing issue.

Hard-money and bridge lenders may feel this more sharply because speed is part of the product. A roof issue can be acceptable if it is known, scoped, and reserved. The same issue can become unacceptable if it appears late with no records and no inspection access.

For stabilized lending, the problem is often false comfort. A PCA may include a remaining useful life estimate, but if the roof was not fully accessible or if section history is missing, the lender should understand the caveat. A clear confidence band helps the lender avoid treating an estimate as a guarantee.

The buyer view: confidence changes price, timing, and negotiation

Buyers do not need every roof to be perfect. They need the roof to be underwritten honestly before the deal structure hardens.

Low confidence can affect:

- Purchase price.

- Seller credits.

- Inspection contingency.

- Lender reserve.

- Insurance timeline.

- Capital plan.

- Tenant improvement budget.

- Closing schedule.

- Post-close maintenance plan.

The most expensive roof surprise is often not the defect itself. It is the timing. If missing age evidence appears before pricing, it can be priced. If it appears after financing terms are set, it can create friction. If it appears near closing, it can threaten the transaction.

For 1031 exchange buyers, this matters even more because replacement-property timing can be tight. A low-confidence roof does not necessarily kill a deal, but it should change the diligence rhythm. The existing [1031 exchange roof records guide](/insights/commercial-roof-records-1031-exchange-acquisition/) explains why roof records should be organized early when timing pressure is high.

An age confidence band gives the buyer a more precise basis for action. Instead of asking "Is the roof old?" the buyer can ask "Which roof areas are unknown, which have current condition evidence, and what would it cost us to remain uncertain?"

The broker view: better roof language reduces late-stage friction

Brokers are not roof inspectors. They should not certify roof condition, interpret warranties, estimate remaining useful life, or guarantee that weather did not affect a roof. But brokers do influence the first roof narrative a buyer sees. That matters.

Weak broker language creates false expectations:

- "New roof" when only a portion was replaced.

- "Roof in good condition" without a dated source.

- "Roof under warranty" without transfer or exclusion details.

- "No roof issues" when tenant leak logs were not reviewed.

- "Roof replaced" when the work was coating or localized repair.

Stronger language connects the claim to the evidence:

- "Seller provided a 2019 invoice for replacement of the main warehouse roof field; office addition roof age not documented."

- "Seller provided coating warranty dated 2021; coating scope and transfer terms should be reviewed by buyer."

- "PCA observed roof in 2024 and estimated remaining useful life for accessible areas; buyer should confirm inaccessible sections."

- "Tenant leak history requested; no file received as of offering package date."

This does not weaken marketing. It prevents the offering package from overpromising. The [broker listing diligence guide](/insights/commercial-roof-broker-listing-diligence/) covers this in more detail for flat-roof listings.

The roofer view: age confidence creates advisory opportunities

Commercial roofers can use age confidence bands without turning every conversation into an emergency sales pitch. That is important for channel partnerships. The value is not only replacement demand. It is better timing, better owner education, and better trust.

A roofer can review a building's age confidence pattern and recommend:

- Baseline inspection for unknown sections.

- Maintenance plan for documented but aging sections.

- Drain cleaning and photo documentation where condition confidence is weak.

- Warranty transfer review before sale.

- Post-weather inspection after meaningful exposure.

- Repair versus restoration discussion where age and condition support it.

- Replacement planning where age, condition, and consequence align.

This creates a practical workflow. A roofer does not have to say "the roof is failing" to create value. The roofer can say "your roof file has a documented main section, an unknown office section, and no current photos after recent wind exposure; the next responsible step is inspection and documentation." That is a professional advisory position.

For Asset Optimix, this is central to the first route to market. Roof prediction should help commercial roofers identify where an owner, broker, buyer, or lender already has a decision problem. Age confidence bands make that decision problem easier to explain.

The insurer view: age confidence prevents overreliance on a single field

Insurance and insurtech teams often receive roof age as a structured field. That field is useful, but it is risky when it becomes the only roof signal. A single roof age number can hide missing records, different roof sections, recover work, dense equipment, poor drainage, or post-installation weather exposure.

For underwriting and loss-control workflows, a better roof file separates:

- Age confidence.

- Material or system confidence.

- Condition confidence.

- Maintenance confidence.

- Weather exposure.

- Consequence of failure.

- Inspection recency.

This distinction helps route attention. A roof with low age confidence may not be high risk, but it may deserve follow-up. A roof with high age confidence and poor condition may deserve a different action. A roof with high age confidence and strong condition evidence may not need the same intervention as a vague older roof over high-value tenant operations.

Confidence also improves communication with producers and insureds. Instead of saying "roof age unacceptable," the file can say "roof age is unknown for two sections, inspection photos are unavailable, and maintenance records were not provided." That turns a blunt rejection or surcharge discussion into a specific evidence request.

The asset manager view: portfolio decisions need comparability

Asset managers rarely have the luxury of studying one roof at a time. They need to compare buildings across a portfolio, market, tenant base, and capital plan. Roof age confidence bands help make that comparison fair.

A portfolio view might rank assets by:

- Lowest age confidence.

- Oldest documented roof areas.

- Largest unknown roof area.

- Highest tenant consequence.

- Weakest drainage evidence.

- Greatest weather exposure since last inspection.

- Most inconsistent records.

- Highest near-term reserve need.

This is better than sorting by age alone. A building with an older documented roof may be less urgent than a building with unknown roof age, limited access, repeated leak tickets, and a mission-critical tenant. A building with a newer roof may still deserve attention if the section with the most equipment is undocumented.

For municipalities and public portfolios, confidence bands can support defensible prioritization. A public owner may not be able to fund every roof immediately. A ranking that separates age, condition, consequence, and confidence is easier to explain than one that simply says "oldest first."

Confidence bands should be versioned over time

Roof confidence is not static. It should improve or decline as evidence changes.

Confidence can improve when:

- Invoices are located.

- Warranty documents are found.

- A roof plan is marked by section.

- Current photos are collected.

- A qualified inspection is completed.

- Drain maintenance records are organized.

- Tenant leak logs are reconciled.

- Weather exposure is reviewed against post-event inspections.

- Repair locations are mapped.

Confidence can decline when:

- Records conflict.

- A roof becomes inaccessible.

- New leaks appear.

- Repairs repeat in the same area.

- Major weather occurs without follow-up inspection.

- Rooftop equipment is added without roof documentation.

- A warranty transfer fails.

- Drainage behavior worsens.

- Photos become stale.

That means age confidence should have an as-of date. "Documented as of 2026-05-28" is different from a permanent label. A roof file that was strong three years ago may be stale if the building added equipment, experienced severe weather, or developed tenant complaints.

Versioning also helps prevent blame. When the confidence band changes, the file should explain why. That makes the roof record a living underwriting asset rather than a one-time diligence folder.

A simple scoring model can support consistent triage

Confidence bands can remain qualitative, but a simple scoring model can help portfolios and partner workflows. The key is to keep the score explainable.

One practical approach:

| Evidence category | Strong | Moderate | Weak |

|---|---|---|---|

| Installation scope | Contract, invoice, permit, section map | Seller records or partial documents | Owner memory only |

| Roof section mapping | Areas marked by plan or aerial | Some sections identified | One building-level age |

| Current condition | Recent roof photos or inspection | Older photos or limited observation | No condition evidence |

| Repair history | Mapped invoices and leak logs | Partial maintenance records | No records or vague statements |

| Weather response | Post-event inspection or notes | Exposure known, response unclear | Exposure unknown or not reviewed |

| Access quality | Full roof access | Limited roof access | No roof access |

The output can convert into a band, but the explanation matters more than the number. A numeric score without explanation becomes another black box. A band with evidence notes tells the user what to do.

For example:

| Building | Age confidence | Main driver | Next action |

|---|---|---|---|

| Retail center A | Supported | Invoices found, section map missing | Request roof plan and warranty transfer detail |

| Warehouse B | Unknown | No records, no access, leak history | Schedule roof inspection before reserve finalization |

| Office C | Documented | Full replacement package and current photos | Use age field, monitor drainage and maintenance |

| Industrial D | Inferred | Aerial and repair history only | Validate age before lender review |

This kind of output is usable in a roofer outreach list, lender diligence file, insurance follow-up queue, or asset management dashboard.

Age confidence should drive specific triggers

The value of a confidence band is the trigger it creates. Without triggers, confidence becomes another label.

Common triggers include:

- Unknown age over high-consequence tenant space: inspect before acquisition or renewal.

- Supported age but no section map: request records before marketing or financing.

- Documented age but current photos stale: update photo set before reserve decision.

- Inferred older age plus recent severe weather exposure: schedule post-event inspection.

- Recover date documented but underlying assembly unknown: review moisture, deck, and prior roof evidence before assuming useful life.

- Coating date documented but described as replacement: correct file language and review warranty terms.

- Repeated repairs in same area: move from age question to condition and cause question.

- Roof access denied: reduce confidence and record the limitation.

These triggers keep the workflow practical. They also help different stakeholders share one file. The broker sees what can be said. The buyer sees what to inspect. The lender sees what affects reserves. The roofer sees where to advise. The insurer sees what evidence is missing.

Do not let confidence become a substitute for professional judgment

Roof age confidence bands are decision aids, not professional conclusions. They should not be used to certify condition, state code compliance, interpret warranty terms, determine insurance coverage, promise useful life, or replace qualified inspection.

The limits should be explicit:

- Age confidence is about evidence quality, not roof quality by itself.

- Condition confidence depends on inspection scope and date.

- Weather exposure is context, not damage proof.

- Remaining useful life is an estimate, not a guarantee.

- Replacement cost requires current scope and market pricing.

- Warranty value depends on terms, transfer, exclusions, maintenance, and claim procedure.

- Hidden moisture and deck issues may not be visible without appropriate testing.

Clear limits make the output more useful, not less. Commercial decisions are full of uncertainty. The point is to name uncertainty early enough that the right person can address it.

What to request before assigning a band

Before assigning a roof age confidence band, ask for a small but disciplined set of records:

| Request | Why it matters |

|---|---|

| Roof plan or aerial section map | Prevents one age from covering multiple roof areas |

| Replacement or repair invoices | Shows dates, scope, contractor, and affected areas |

| Warranty documents | Helps distinguish system work from repair or coating claims |

| Permits or closeout package | Supports installation timeline and scope |

| PCA roof excerpts | Shows prior condition observations and useful life estimates |

| Current roof photos | Connects age to current condition |

| Leak logs and tenant work orders | Reveals repeated locations and consequence |

| Drain maintenance records | Shows whether age is being modified by water behavior |

| Rooftop equipment work orders | Identifies post-installation penetrations and traffic |

| Weather response records | Shows whether exposure was followed by inspection or repair |

The request is intentionally practical. A small owner may not have everything. A seller preparing a listing may need time to gather it. A roofer may help create the first clean photo set. The band should reflect what is available, not punish a file for being imperfect without explaining what is missing.

How Asset Optimix should present the output

A useful roof age output should avoid both false certainty and vague caution. It should be concise enough for a business user and specific enough for a technical follow-up.

A strong output might read:

"Main warehouse roof: supported age band, 2017 recover based on seller invoice and warranty reference; section map pending. Current condition confidence is medium because no roof photos after 2025 wind exposure were provided. Recommended next action: confirm recover scope, request section map, and schedule roof photo update before lender reserve finalization."

That sentence does several things:

- It names the roof area.

- It labels the age confidence.

- It identifies the evidence.

- It states the missing evidence.

- It separates age from condition.

- It connects the finding to a decision.

That is more useful than "roof age 9 years" or "medium risk." It gives the user a defensible next step.

For public-facing education, the same principle applies. The existing [commercial roof failure patterns guide](/insights/commercial-roof-failure-patterns/) explains that roof failure is a chain of signals. Age is one signal. Confidence tells the user how much to trust that signal.

Common mistakes to avoid

The most common roof age mistakes are simple:

- Treating one age as if it covers every roof area.

- Calling a coating or repair a replacement.

- Ignoring recover history.

- Treating remaining useful life as a guarantee.

- Using a PCA estimate without checking access limits.

- Assuming no leak complaints means no roof problem.

- Ignoring rooftop equipment changes after installation.

- Treating weather exposure as proof of damage.

- Averaging roof ages across sections.

- Failing to update confidence after new evidence arrives.

Each mistake can be prevented with a better record structure. The structure does not have to be complicated. It just has to separate roof area, work type, age evidence, condition evidence, exposure, consequence, confidence, and next action.

The commercial value is better timing

Roof age confidence bands are not just a cleaner data field. They improve timing.

For roofers, they identify where an owner needs education, inspection, maintenance, restoration, or replacement planning. For brokers, they reduce late diligence surprises. For buyers, they help price uncertainty before negotiations harden. For lenders, they support reserve and condition decisions. For insurers, they separate unknowns from known maintained risks. For owners, they turn a vague roof file into a capital planning tool.

The commercial roof is one of the largest physical assets on many buildings, but it is often described with a single age. That is not enough. A roof age without confidence can mislead every stakeholder in the transaction.

The stronger approach is section-level, evidence-based, and explicit about limits. State the chronological age when it is supported. Adjust the practical view with condition and exposure. Estimate remaining useful life only with context. Show confidence clearly. Then connect the confidence band to a next action.

That is how roof age becomes useful in commercial property underwriting.

Frequently asked questions

What is a commercial roof age confidence band?

It is a label for how strongly the file supports a roof age claim. A documented band may have invoices, permits, warranty records, section mapping, and photos. An inferred or unknown band needs caveats and usually triggers inspection or record requests.

Is roof age the same as remaining useful life?

No. Roof age is historical. Remaining useful life is a forward-looking estimate that depends on condition, records, access, system type, maintenance, weather exposure, and professional judgment.

Can a newer roof still have low underwriting confidence?

Yes. A newer roof with missing records, unclear scope, limited access, dense rooftop equipment, repeated leaks, or no post-weather inspection can have lower confidence than an older roof with strong documentation and current condition evidence.

Sources and limits

Research basis reviewed against ASTM PCA framing, Fannie Mae PCA and estimated useful life guidance, WBDG, EPA, NOAA/NCEI, NWS, IBHS, and BLS public sources. These sources support context, definitions, and public guidance. They do not turn a remote report into a roof-specific inspection, coverage opinion, engineering opinion, code opinion, warranty interpretation, or project bid.

- ASTM E2018 property condition assessment guideCommercial property condition assessment framing for transaction diligence, observed condition, and capital planning scope awareness.

- Fannie Mae Multifamily PCA underwriting guidanceUnderwriting inspection and replacement-reserve context for property condition, deferred maintenance, useful life, and repair needs.

- Fannie Mae estimated useful life tablesEstimated useful life table context for building components, including roof-system planning references.

- NOAA/NCEI Storm Events DatabaseOfficial storm-event records used for weather exposure context, not parcel-specific proof of damage.

- National Weather Service severe weather definitionsPublic definitions for severe thunderstorm, hail, and wind criteria.

- WBDG moisture management strategiesBuilding-enclosure moisture control context for design, construction, operation, and maintenance.

- WBDG roofing systems knowledge areaRoofing-system degradation, drainage, corrosion, penetration, and maintenance context.

- FEMA low-slope roof systems mitigation fact sheetPublic-facility low-slope roof mitigation framing for wind, wind-driven rain, and rainfall events.

- IBHS commercial property loss-prevention researchCommercial-building wind and roof vulnerability context, including roof membrane, edge flashing, rooftop equipment, and load-path focus areas.

- EPA moisture-control guidanceOperating and maintenance context for moisture-controlled buildings, including low-slope roof drainage principles.

- BLS Producer Price IndexPublic construction and roofing contractor price-index categories for cost-trend context, not project-specific bids.